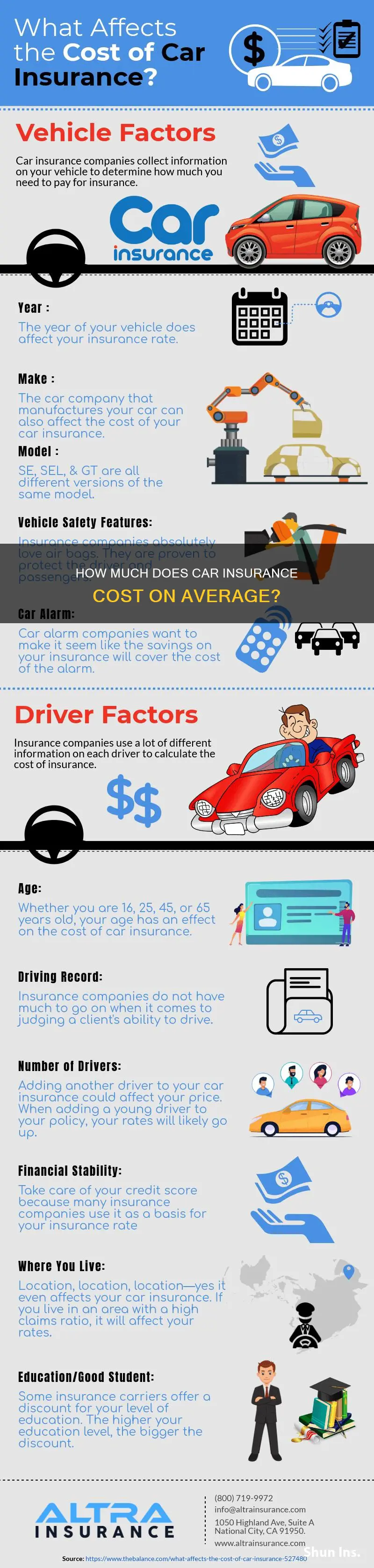

The average cost of car insurance is influenced by a multitude of factors, including age, gender, location, driving record, credit history, vehicle type, and more. In May 2025, the average cost of a full coverage policy was $2,692 per year, while a minimum coverage policy averaged $808 per year. The national average cost for car insurance is $2,149 per year, according to Forbes' analysis. However, rates vary significantly by state, with Idaho averaging $123 per month for full coverage and Florida averaging $343 per month. Additionally, individual premiums can differ based on factors such as age, with teens being among the most expensive to insure. Improving one's credit score, maintaining a clean driving record, and taking advantage of discounts are all strategies to lower insurance costs.

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

Full coverage vs. minimum coverage

The average cost of car insurance in the US is $2,068 per year, according to one source. However, another source states that the national average is $2,680 per year for full coverage and $802 per year for minimum coverage. The cost of auto insurance depends on various factors, including age, driving history, location, coverage type, and vehicle make and model.

When it comes to full coverage vs. minimum coverage, there are several key differences to consider. Firstly, it's important to understand the difference between liability-only insurance and full coverage. Liability-only insurance covers injury and damage caused to another person's property or vehicle. In contrast, full coverage includes liability insurance and adds protection for damage to your vehicle from collisions and non-collision incidents like storms and fires. It also often includes rental reimbursement and emergency roadside coverage.

The cost of full coverage insurance is significantly higher, averaging 234% more than minimum coverage. For example, the average cost of full coverage car insurance is $2,290 per year, while minimum coverage costs an average of $623 per year, according to NerdWallet's June 2025 rate analysis. However, the extra expense may be worth it for the added protection. If you cause an accident, liability insurance may not provide sufficient financial coverage, leaving you with substantial out-of-pocket expenses.

Your decision between full coverage and minimum coverage depends on several factors. Firstly, consider your state's requirements. Each state has different mandates for the types and amounts of coverage needed to drive legally. Additionally, if your vehicle is leased, financed, or not yet paid off, your lender may require you to carry full coverage insurance. Your overall financial situation and comfort level with financial risk will also influence your choice. If the cost of repairing or replacing your vehicle out of pocket is a concern, full coverage may be the better option. On the other hand, if you own your car outright and feel comfortable with the risks, minimum coverage may suffice.

There are ways to reduce your car insurance costs, regardless of whether you choose full or minimum coverage. Many insurance providers offer discounts for safe driving, good grades, low mileage, paperless billing, and automatic payments. Additionally, you may be able to get a discounted premium by bundling your car insurance with other policies, such as home or renters insurance, from the same insurer. Improving your credit score can also help lower your insurance rate in most states.

Arsenal Credit Union: Is Your Money Federally Insured?

You may want to see also

Explore related products

![]()

Discounts for paying in full

The average cost of car insurance varies depending on several factors, including age, driving history, location, coverage, and vehicle make and model. According to a rate study, the average annual cost of car insurance is $2,068. However, the cost of full coverage is higher, averaging $2,290 per year, while minimum coverage costs around $623 annually.

When it comes to discounts for paying auto insurance in full, several insurance providers offer incentives for policyholders who opt for this payment method. Here are some key points to consider:

- Discounts for Annual or Semiannual Payments: Some insurance companies provide discounts for customers who pay their premiums in full as a single annual or semiannual lump sum. This option can result in significant savings compared to paying monthly or quarterly installments. The discount range offered by top companies is typically between 6% and 14% for annual payments.

- Avoid Monthly Finance Fees: In addition to the discount, paying in full can help you avoid monthly finance or service fees charged by some insurance companies when payments are spread out. These fees can add up over time, so paying in full can result in even more savings.

- Paperless Policy Discounts: Many insurance providers offer discounts for policyholders who opt for paperless billing and receive their bills and policy documents electronically. This not only saves the company printing and mailing costs but also contributes to environmental sustainability.

- Automatic Payments Plan: While not a direct discount, it's worth noting that most insurance companies charge service fees for processing payments on an insurance policy. By opting to pay in full each renewal period, you can avoid these service fees altogether.

- Telematics Discounts: Although not directly related to paying in full, telematics programs offer another opportunity for savings. These programs use GPS technology to track driving habits like speeding, harsh braking, and phone use. Many insurers provide discounts to drivers who share their telematics data and demonstrate safe driving behaviors.

It's always a good idea to review your policy and discuss available discounts with your insurance agent. By taking advantage of these payment-related discounts, you can significantly reduce your auto insurance costs.

How Police Verify Your Car Insurance

You may want to see also

Explore related products

![]()

Impact of credit score

The average cost of car insurance is influenced by a multitude of factors, including age, driving history, location, coverage type, and vehicle type. According to a rate study, the average annual cost of car insurance is $2,068. However, this amount can vary significantly depending on individual circumstances.

Credit scores have a notable impact on automobile insurance rates. While insurers do not directly consider credit scores when determining premiums, they do factor in credit history in most states. They use a credit-based insurance score, which considers similar factors to a regular credit score but weighs them differently. This includes outstanding debt, credit history length, credit mix, and payment history.

Individuals with poor credit scores are often viewed as higher-risk customers by insurers. Actuarial data suggests that drivers with poor credit are more likely to file claims, leading to higher insurance rates. Conversely, those with good credit may benefit from lower premiums, assuming other factors are favourable. The impact of credit scores on insurance rates can vary across states, with some states prohibiting the use of credit information altogether.

Improving one's credit score can help lower insurance rates. This can be achieved by making consistent, timely payments, reducing debt, and maintaining a positive credit history. Additionally, shopping around for insurance quotes and taking advantage of discounts can help mitigate the impact of a poor credit score on insurance premiums.

In summary, while credit scores are not the sole determinant of automobile insurance rates, they play a significant role in assessing an individual's risk profile. By managing their credit responsibly and exploring alternative options, individuals can optimise their insurance costs.

Verify Insurance Certificates: Quick and Easy Steps

You may want to see also

Explore related products

![]()

Age and cost

Age is a significant factor in determining the cost of automobile insurance. Insurers use age as an indicator of how risky an individual is to insure, and younger drivers are often charged heftier prices due to their lack of experience. According to data from June 2025, the average annual cost of car insurance for full coverage was $2,680 for 40-year-old drivers. However, this figure varies significantly for younger drivers, with 18-year-olds facing the highest premiums among the age groups analysed. Male drivers under 18 pay almost 50% more than their female counterparts, and 16-year-olds of any gender pay an average of 80% more than older drivers.

The impact of age on insurance costs is most pronounced for young drivers, with rates typically decreasing as individuals get older. Drivers aged 16 to 24 tend to face the highest premiums, with rates gradually decreasing for older age groups. By the time individuals reach their 30s, gender becomes less of a factor, and men and women pay comparable rates. However, it is important to note that age is not the only factor influencing insurance rates.

An individual's driving record, credit history, location, and type of coverage purchased also play a role in determining insurance costs. For example, at-fault accidents and DUI convictions can lead to significant increases in insurance rates. Additionally, drivers with poor credit may pay higher rates, as they are perceived as more likely to file claims. On the other hand, safe driving, good grades, and low mileage can often lead to discounts and lower premiums.

While age is a critical factor in determining insurance rates, it is not the only consideration. By bundling policies, reducing mileage, raising deductibles, and taking advantage of discounts, individuals can find ways to lower their insurance costs, regardless of their age. Additionally, usage-based insurance programs can help younger drivers with limited driving histories obtain lower premiums by monitoring their driving behaviour and offering discounts for safe practices.

Insurance Checker: What Is It and How Does It Work?

You may want to see also

Explore related products

![]()

Location and cost

The cost of automobile insurance varies significantly depending on location. Car insurance rates are set by ZIP code, so moving to a different area, even if it is just a few blocks away, can cause your rates to change. Some ZIP codes have higher crime and accident rates than others, which makes auto insurance more expensive.

In the United States, the national average cost of car insurance is $2,149 per year for full coverage, according to Forbes Advisor. However, individual premiums vary based on factors such as age, gender, marital status, driving record, credit history, and the make and model of the car. The national average cost for a minimum coverage policy is $808 per year, or $631 according to another source. USAA has the cheapest average annual rate for car insurance at $1,335, but their policies are only available to military community members and their families. The second-cheapest average rate is offered by Erie at $1,532 per year.

The average cost of car insurance also varies from state to state, with some states having significantly higher rates than others. For example, the average cost of car insurance after a DUI for a full coverage policy is $2,184 per year in Idaho, but it is $7,471 per year in Michigan. Similarly, the average cost of a six-month liability-only policy is $79.83 per month in some states, $105.36 in others, and $157.27 in yet others.

Within states, individual factors such as age, driving history, and credit score can also impact insurance rates. Drivers with poor credit pay around 75% more for full coverage car insurance compared to those with good credit. Insurance companies justify higher prices for those with poor credit by pointing to data linking poor credit to more frequent insurance claims. However, some states, including California, Hawaii, and Massachusetts, do not allow insurers to use credit when determining car insurance rates.

FDIC Insurance: What's Covered and What's Not

You may want to see also

Frequently asked questions

The average annual cost of car insurance in the US ranges from $1,335 to $2,692, depending on the source and the type of coverage. For instance, the national average cost for full coverage car insurance is $2,149 per year, according to Forbes Advisor's 2025 analysis. In contrast, the average cost of minimum coverage car insurance is $631 per year.

Several factors influence the cost of car insurance, including age, location, driving record, vehicle usage, accidents, vehicle type, and credit history. For example, younger drivers are generally considered to be riskier and are charged higher premiums. Similarly, drivers with a history of accidents or traffic violations will likely pay more for insurance.

There are several ways to reduce the cost of car insurance:

- Improve your credit score: A higher credit score can lead to lower insurance premiums.

- Shop around: Compare quotes from multiple insurance companies to find the best rates.

- Bundle policies: You may get a discount by purchasing multiple types of insurance, such as home and auto insurance, from the same company.

- Pay in full: Many insurance providers offer discounts for paying the full premium upfront instead of in monthly installments.

- Reduce mileage: Driving fewer miles can lead to lower premiums, as it reduces the risk of accidents.

- Safe driving: Maintaining a clean driving record without accidents or violations can help you qualify for lower rates.