The Bank Insurance Fund (BIF) was a unit of the Federal Deposit Insurance Corporation (FDIC) that provided insurance protection for banks that were not classified as savings and loan associations. The BIF was created in response to the savings and loan crisis of the late 1980s. The FDIC was established in 1933 to provide insurance for all banks and protect your money in the event of a bank failure. The BIF merged with the Savings Association Insurance Fund in 2006 to become the Deposit Insurance Fund (DIF), which insures deposits in commercial banks and savings banks. The DIF is funded by insured banks through quarterly assessments and interest income on its securities.

| Characteristics | Values |

|---|---|

| What is it? | A unit of the Federal Deposit Insurance Corporation (FDIC) |

| When was it created? | 1933 |

| What was the purpose? | To provide insurance protection for banks that were not classified as savings and loan associations |

| What was the maximum insured amount? | $100,000 per account |

| Who did it cover? | All depositors with accounts in FDIC-insured banks |

| What types of accounts were insured? | Traditional deposit accounts like certificates of deposit (CDs) |

| How was it funded? | Funded through quarterly assessments on insured banks and interest income on its securities |

| What happened to the fund? | In 2006, it merged with the Savings Association Insurance Fund to become the Deposit Insurance Fund (DIF) |

| What is the current status of the DIF? | As of Q3 2024, the DIF stood at $129.2 billion with a 1.21% reserve ratio |

Explore related products

What You'll Learn

- The Bank Insurance Fund (BIF) was a unit of the Federal Deposit Insurance Corporation (FDIC)

- BIF provided insurance protection for banks not classified as savings and loan associations

- BIF was created in response to the savings and loan crisis of the late 1980s

- BIF merged with the Savings Association Insurance Fund in 2006 to become the Deposit Insurance Fund (DIF)

- DIF is funded through assessments on insured banks and interest income on its securities

![]()

The Bank Insurance Fund (BIF) was a unit of the Federal Deposit Insurance Corporation (FDIC)

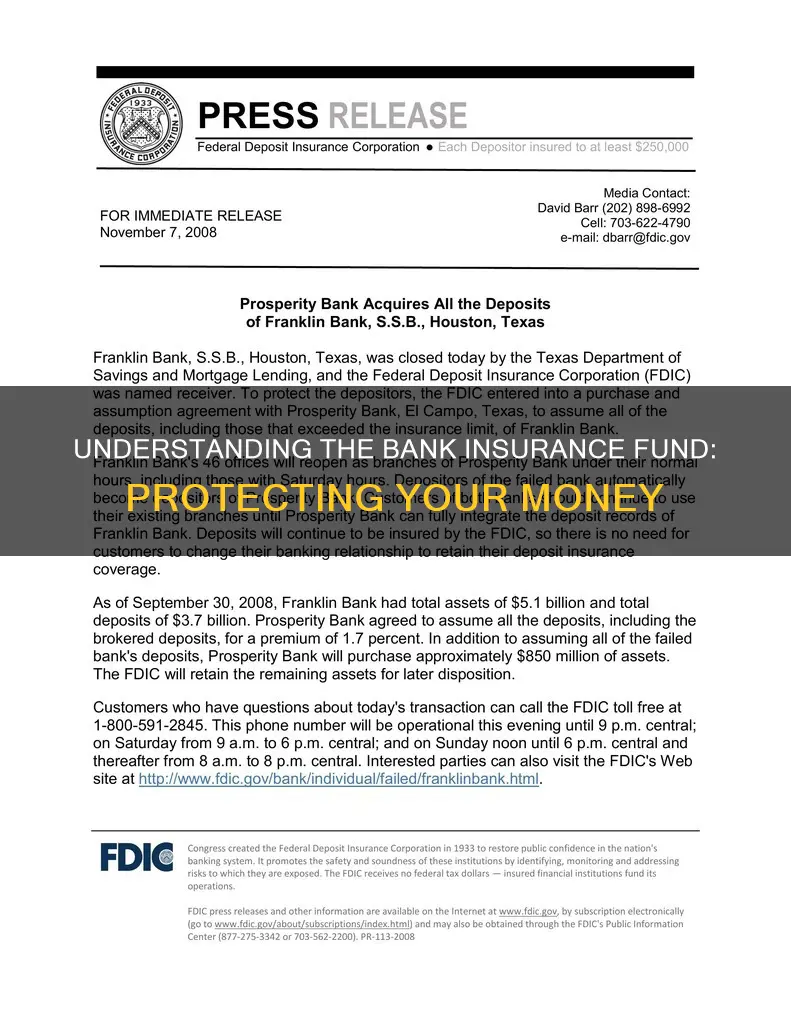

The FDIC was established in 1933 under the Federal Deposit Insurance Act to provide insurance for all banks. The BIF was one of two FDIC reserve funds that existed between 1989 and 2006, the other being the Savings Association Insurance Fund (SAIF). The BIF insured deposits in commercial banks and savings banks up to a maximum of $100,000 per account. It is important to note that the BIF received no taxpayer money; instead, insured banks paid for deposit insurance through premium assessments on their domestic deposits.

The existence of two separate funds led banks to shift business between the BIF and SAIF depending on the benefits each could provide. At one point in the 1990s, SAIF premiums were five times higher than BIF premiums, leading several banks to attempt to qualify for the BIF. Some banks even merged with institutions qualified for the BIF to avoid the higher premiums of the SAIF.

In 2006, the BIF merged with the SAIF to become the Deposit Insurance Fund (DIF). The primary purpose of the DIF is to insure deposits and protect the depositors of insured banks. The DIF is funded mainly through quarterly assessments on insured banks, and it also receives interest income on its securities. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 revised the FDIC's fund management authority by setting requirements for the Designated Reserve Ratio (DRR) and redefining the assessment base used to calculate banks' quarterly assessments.

Understanding Bank Account Insurance Limits

You may want to see also

Explore related products

![]()

BIF provided insurance protection for banks not classified as savings and loan associations

The Bank Insurance Fund (BIF) was a unit of the Federal Deposit Insurance Corporation (FDIC) that provided insurance protection for banks that were not classified as savings and loan associations. The BIF was created in response to the savings and loan crisis of the late 1980s, which saw the failure of another federal insurer, the FSLIC. From 1934 to 1989, the deposit insurance premium for banks was 12 cents per $100 of domestic deposits.

The BIF insured deposits in commercial banks and savings banks up to a maximum of $100,000 per account. Insured banks paid for deposit insurance through premium assessments on their domestic deposits. Foreign deposits, or deposits at branch offices outside the United States or its territories, were not insured and thus not subject to deposit insurance premiums. The BIF did not receive taxpayer money.

In 2005, the Federal Deposit Insurance Act abolished the BIF and the Savings Association Insurance Fund (SAIF), creating a single Deposit Insurance Fund (DIF). The DIF is funded primarily through quarterly assessments on insured banks and interest income on its securities. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 set requirements for the Designated Reserve Ratio (DRR) and redefined the assessment base, which is used to calculate banks' quarterly assessments. The FDIC has used this to develop a long-term management plan for the DIF, designed to reduce pro-cyclicality and maintain a positive fund balance even during a banking crisis.

Explore Banking and Insurance: Career Opportunities

You may want to see also

Explore related products

$19.99 $20.99

![]()

BIF was created in response to the savings and loan crisis of the late 1980s

The Bank Insurance Fund (BIF) was a unit of the Federal Deposit Insurance Corporation (FDIC) that provided insurance protection for banks that were not classified as savings and loan associations. The BIF was created in response to the savings and loan crisis of the late 1980s.

The savings and loan crisis was a period of financial turmoil for savings and loan associations in the United States, which led to the closure of many of these institutions. The crisis was caused by a combination of economic, regulatory, and market factors. During this time, many savings and loan associations failed due to a variety of issues, including poor financial management, fraud, and a declining economy. This crisis had a significant impact on the banking industry and led to a loss of public confidence in financial institutions.

In response to the crisis, the Federal Deposit Insurance Corporation (FDIC) created the Bank Insurance Fund (BIF) to provide insurance protection for banks that were not classified as savings and loan associations. The BIF was established to help restore public confidence in the banking system and to protect depositors in the event of bank failures. The BIF provided coverage for depository institutions, insuring deposits in commercial banks and savings banks up to a maximum of $100,000 per account. This insurance protection was designed to reassure depositors that their money was safe and protected, even if their bank failed.

The BIF played an important role in maintaining the stability of the banking system and protecting depositors' funds. It was funded through premium assessments on insured banks, with no taxpayer money involved. The premiums were based on the bank's balance of insured deposits and the degree of risk that the bank posed to the FDIC. This risk-based pricing system allowed the BIF to maintain a stable source of funding while also providing an incentive for banks to manage their risk effectively.

In 2006, the BIF merged with the Savings Association Insurance Fund (SAIF) to become the Deposit Insurance Fund (DIF). This merger reflected the FDIC's assumption of responsibility for insuring savings and loan associations, consolidating the two separate funds that served similar purposes. The DIF continues to provide insurance protection for depositors, with an increased coverage limit of $250,000 per account. The FDIC has also implemented comprehensive management plans to maintain a positive fund balance and steady assessment rates, even during economic downturns and banking crises.

Key Bank and Federal Deposit Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

BIF merged with the Savings Association Insurance Fund in 2006 to become the Deposit Insurance Fund (DIF)

The Bank Insurance Fund (BIF) was a unit of the Federal Deposit Insurance Corporation (FDIC) that provided insurance protection for banks that were not classified as savings and loan associations. The BIF was created in 1989 in response to the savings and loan crisis of the late 1980s.

Between 1989 and 2006, there were two separate FDIC reserve funds: the BIF and the Savings Association Insurance Fund (SAIF). This division reflected the FDIC's assumption of responsibility for insuring savings and loan associations after another federal insurer, the FSLIC, was unable to recover from the savings and loan crisis. However, the existence of two separate funds for the same purpose led banks to shift business from one to the other, depending on the benefits each could provide.

In 2005, the Federal Deposit Insurance Act was passed, abolishing the BIF and the SAIF and creating a single Deposit Insurance Fund (DIF). The FDIC merged the two funds on March 31, 2006, with an effective date of no later than July 1, 2006. As a result of the merger, the BIF and SAIF were abolished, and the DIF was formed.

The primary purpose of the DIF is to insure deposits and protect the depositors of insured banks. The DIF is funded mainly through quarterly assessments on insured banks, but it also receives interest income on its securities. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Dodd-Frank Act) revised the FDIC's fund management authority by setting requirements for the Designated Reserve Ratio (DRR) and redefining the assessment base, which is used to calculate banks' quarterly assessments. The DIF's balance totaled $110.3 billion in the fourth quarter of 2019 and stood at $129.2 billion in Q3 2024, or a 1.21% reserve ratio.

Private Medicine: Public Insurance, Mutual Benefits

You may want to see also

Explore related products

![]()

DIF is funded through assessments on insured banks and interest income on its securities

The Deposit Insurance Fund (DIF) is the result of a merger between the Bank Insurance Fund (BIF) and the Savings Association Insurance Fund (SAIF) in 2006. The BIF was a unit of the Federal Deposit Insurance Corporation (FDIC) that provided insurance protection for banks that were not classified as savings and loan associations. The FDIC is a corporation that was created in 1933 to provide insurance for all banks. The FDIC does not receive any federal funding and is funded by the insured banks themselves.

The DIF is funded through assessments on insured banks and interest income on its securities. The FDIC assesses premiums on each member bank and accumulates them in the DIF, which it uses to pay its operating costs and the depositors of failed banks. The amount of each bank's premiums is based on its balance of insured deposits and the degree of risk that it poses to the FDIC. The FDIC charges higher premiums to banks that pose a higher risk. The DIF is also funded through interest income on its securities, as it is fully invested in Treasury securities.

The primary purpose of the DIF is to insure the deposits and protect the depositors of insured banks. The FDIC provides deposit insurance to protect individuals' money in the event of a bank failure. All amounts that a particular depositor has in accounts in any particular ownership category at a particular bank are added together and insured up to $250,000. The FDIC also offers open bank assistance (OBA), where it arranges for the purchase or recapitalization of an institution before it actually fails, and uninsured depositors are usually protected in these transactions.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 revised the FDIC's fund management authority by setting requirements for the Designated Reserve Ratio (DRR) and redefining the assessment base, which is used to calculate banks' quarterly assessments. The FDIC developed a comprehensive, long-term management plan for the DIF to reduce pro-cyclicality and achieve moderate and steady assessment rates. The DIF's balance totaled $110.3 billion in the fourth quarter of 2019 and stood at $129.2 billion in Q3 2024.

UHC: Private or Public Insurance?

You may want to see also

Frequently asked questions

The Bank Insurance Fund was a unit of the Federal Deposit Insurance Corporation (FDIC) that provided insurance protection for banks that were not classified as savings and loan associations. The BIF was created in response to the savings and loan crisis of the late 1980s.

In 2006, the BIF merged with the Savings Association Insurance Fund (SAIF) to become the Deposit Insurance Fund (DIF) due to banks shifting business between the two funds depending on the benefits each could provide. The DIF is funded by insured banks through quarterly assessments and interest income on its securities.

The Federal Deposit Insurance Corporation was created in 1933 under the Federal Deposit Insurance Act to provide insurance for all banks. The FDIC provides deposit insurance to protect your money in the event of a bank failure.