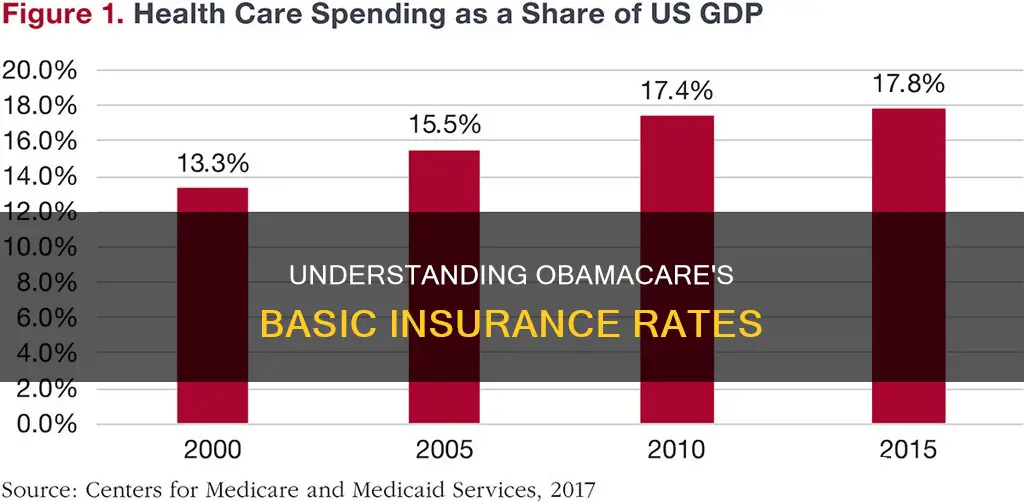

Obamacare, officially known as the Affordable Care Act (ACA), was enacted in 2010 to create a health insurance marketplace. The ACA expanded Medicaid eligibility, making it possible for millions of Americans to get health insurance coverage. The cost of Obamacare plans is influenced by factors such as age, state, company, and income. For instance, the average monthly cost of an Obamacare plan for a 30-year-old is $483, while for a 40-year-old, it is $544, and for a 50-year-old, it is $760. The type of plan also influences the cost, with bronze and silver plans having cheaper premiums but more out-of-pocket expenses, while gold and platinum plans have higher premiums but lower out-of-pocket costs. Additionally, over 90% of people who buy an Obamacare plan receive premium tax credits, which lower the cost of coverage.

| Characteristics | Values |

|---|---|

| Average Monthly Cost | $621 |

| Average Monthly Cost for a 30-year-old | $483 |

| Average Monthly Cost for a 40-year-old | $544 to $621 |

| Average Monthly Cost for a 50-year-old | $760 |

| Cost Influencing Factors | Age, Plan Type, Company, State, etc. |

| Tier System | Bronze, Silver, Gold, Platinum |

| Premium Tax Credits | Available for people with a household income of up to 400% of the federal poverty level |

| Cost-Sharing Subsidies | Available for Silver plans |

| Cheapest State for Obamacare | New Hampshire |

| Most Expensive State for Obamacare | Vermont |

Explore related products

What You'll Learn

- Obamacare, officially the Affordable Care Act (ACA), offers a health insurance marketplace

- ACA plans are divided into four metal tiers: bronze, silver, gold, and platinum

- ACA premiums are adjusted for age, family size, and income

- ACA plans can be costly, but premium tax credits and subsidies are available

- Catastrophic health insurance is an ACA option for those under 30 or facing economic issues

![]()

Obamacare, officially the Affordable Care Act (ACA), offers a health insurance marketplace

The ACA's health insurance marketplace provides a platform for individuals to explore available plans in their area and select a plan that best suits their needs. The marketplace offers a range of plans with different coverage levels, often referred to as metal tiers: Bronze, Silver, Gold, and Platinum. These tiers differ in their premium costs and out-of-pocket expenses. For instance, Bronze and Silver plans generally have lower premiums but higher out-of-pocket costs, while Gold and Platinum plans have higher premiums but lower out-of-pocket expenses.

The cost of Obamacare plans varies depending on several factors, including age, state, company, and income. Age plays a significant role in determining monthly rates, with older individuals typically paying higher premiums. Additionally, the state in which one resides influences the cost of Obamacare due to differences in the cost of medical care and state and local laws. The company providing the insurance also impacts the rate, as each company sets its own rates for the same plan tier. Furthermore, income is a critical factor, as those with lower incomes may qualify for premium tax credits and subsidies, reducing their overall costs.

It is important to note that Obamacare plans can be expensive, especially for those who do not qualify for subsidies or tax credits. The average cost of an Obamacare plan for a 30-year-old is $483 per month, while it increases to $544 for a 40-year-old and $760 for a 50-year-old. However, the majority of people who purchase Obamacare plans receive discounts, and over four out of ten customers pay less than $10 per month.

Obamacare has had a significant impact on the individual health insurance market, leading to reduced insurer choice and competition, as well as higher premiums for many Americans. Despite this, the ACA has expanded access to health insurance for millions, particularly through the expansion of Medicaid eligibility.

Navigating Insurance Repairs: A Guide to Auto Collision Restoration

You may want to see also

Explore related products

![]()

ACA plans are divided into four metal tiers: bronze, silver, gold, and platinum

Obamacare, officially known as the Affordable Care Act (ACA), created a health insurance marketplace that lets users compare available plans in their area. ACA plans are divided into four metal tiers: bronze, silver, gold, and platinum. These tiers are based on the share of costs for covered services that the insurer and the insured will pay.

Bronze plans have the lowest monthly premiums but the highest costs when you need care. If you are generally healthy and don't need a lot of medical care, a bronze plan may be a good choice. You will be responsible for paying for most routine care yourself, but you will be covered in case of an unexpected health crisis.

Silver plans are considered the "benchmark" plan because of their moderate monthly premiums and moderate costs when you need care. You must choose a silver plan to qualify for cost-sharing reductions, also known as "extra savings" on out-of-pocket expenses such as deductibles, copayments, and coinsurance.

Gold plans have high monthly premiums but low costs when you need care.

Platinum plans have the highest monthly premiums and the lowest costs when you need health services. If you have major health problems and know you will need a lot of medical care, a platinum plan might be right for you. Although you will pay a higher monthly bill, your out-of-pocket costs will be lower.

Maximizing National Insurance: Filling Gaps, Securing Benefits

You may want to see also

Explore related products

$93.99 $132

![]()

ACA premiums are adjusted for age, family size, and income

The Affordable Care Act (ACA), also known as Obamacare, offers health insurance plans that are divided into four metal tiers: bronze, silver, gold, and platinum. The premiums for these plans are adjusted for age, family size, and income.

Age is a significant factor in determining the cost of Obamacare plans. The average monthly rate for a 30-year-old is $483, while it increases to $544 for a 40-year-old and $760 for a 50-year-old. The age of family members applying for coverage also influences the cost of the benchmark plan for a household.

Family size is another critical factor in calculating ACA premiums. The federal poverty level, which determines eligibility for Medicaid and premium subsidies, varies depending on family size. For instance, the poverty level for a single adult is $15,060, while it is $31,200 for a family of four.

Income plays a pivotal role in determining ACA premiums and eligibility for subsidies. Households with incomes under 400% of the federal poverty level qualify for savings on the marketplace. The size of the subsidy is based on the household's income relative to the prior year's poverty level. Premium tax credits are available for households with incomes at or below the federal poverty level, which is $14,580 for an individual and increases with family size.

In addition to age, family size, and income, other factors influencing Obamacare costs include the chosen plan tier, state of residence, and the company providing the insurance. The cost of medical care in each state and state regulations can impact Obamacare rates, with Vermont being the most expensive state for Obamacare in 2025. Furthermore, health insurance companies have the flexibility to set their own rates, leading to variations in the cost of the same plan tier across different companies.

Medicaid and Auto Insurance: Understanding the Relationship

You may want to see also

Explore related products

![]()

ACA plans can be costly, but premium tax credits and subsidies are available

Obamacare, officially known as the Affordable Care Act (ACA), created the health insurance marketplace, which allows individuals to compare available health insurance plans in their area. While the ACA has made it easier for Americans to obtain health insurance coverage, ACA plans can be expensive. The average Obamacare plan costs $483 monthly for a 30-year-old, $544 for a 40-old, and $760 for a 50-year-old. The cost of Obamacare plans depends on various factors, including age, the level of coverage, state, and the company. For instance, New Hampshire is the cheapest state for Obamacare, while Vermont is the most expensive.

However, premium tax credits and subsidies are available to make ACA plans more affordable. As of 2025, over 9 in 10 people who purchase an Obamacare plan receive premium tax credits, which lower the cost of coverage. More than four out of 10 customers pay less than $10 per month. Individuals qualify for premium tax credits if their household income is at the federal poverty level or up to 400% of that level. For individuals with income up to 150% of the federal poverty level, there is no required contribution, while those with income at 400% or above must contribute 8.5% of their household income. If eligible, individuals can save over $500 monthly on average on an ACA health insurance marketplace plan.

In addition to premium tax credits, the ACA also offers cost-sharing reductions (CSR) as financial assistance. CSRs reduce enrollees' deductibles and other out-of-pocket expenses when they seek medical care. The ACA's reforms have made it possible for people of all ages, health statuses, and incomes to purchase comprehensive coverage. For example, more than 19 million people receive advanced premium tax credits for ACA plans, and enrollment in ACA marketplace plans has increased from 12 million in 2021 to 24.2 million in 2025.

It is important to note that the availability of premium tax credits and subsidies may change over time. For instance, the American Rescue Plan Act of 2020 increased the ACA marketplace premium tax credits to ensure affordable health insurance during the COVID-19 pandemic. These enhanced tax credits were later extended through 2025 by the Inflation Reduction Act. However, these lower premium costs are set to end after 2025 unless Congress takes further action.

Unlocking Auto Insurance Discounts: Strategies for Smart Savings

You may want to see also

Explore related products

![]()

Catastrophic health insurance is an ACA option for those under 30 or facing economic issues

Obamacare, officially known as the Affordable Care Act (ACA), created a health insurance marketplace that allows Americans to compare and choose from a variety of plans in their area. The ACA plans can be expensive for those who do not qualify for subsidies or premium tax credits. The cost of Obamacare plans varies depending on factors such as age, state, company, and type of plan. The average cost of an Obamacare plan for a 30-year-old is $483 per month, $544 for a 40-year-old, and $760 for a 50-year-old.

Catastrophic health insurance is a low-cost option available under the ACA for individuals under 30 or those facing economic hardships, such as homelessness, bankruptcy, or significant medical debt. While it offers similar essential health benefits to an ACA plan, it has much higher deductibles and out-of-pocket costs. Catastrophic plans do not have coinsurance, which means that after reaching the plan's deductible, the health plan covers all in-network services for the rest of the year. These plans have lower premiums than Bronze plans and do not qualify for advanced premium tax credits or subsidies.

To qualify for a catastrophic health plan, applicants under 30 are automatically eligible, while those 30 and older must obtain a hardship or affordability exemption. An affordability exemption is granted if the lowest-priced health coverage available, such as through an employer or the ACA marketplace, exceeds 8.09% of the individual's household income. A hardship exemption is granted in cases of economic hardship, such as homelessness, bankruptcy, eviction, or significant medical debt.

The average monthly cost of a catastrophic health plan for a 30-year-old is $282. Catastrophic plans can be a good choice for those seeking affordable health insurance due to their low premiums and comprehensive coverage. However, it is important to consider the high deductibles and out-of-pocket costs associated with these plans.

Essential Auto Insurance Coverage: The Bare Minimum You Need

You may want to see also

Frequently asked questions

Obamacare is another name for the Affordable Care Act (ACA), which is a law that helps make it easier to get health insurance coverage.

Several factors influence the cost of Obamacare, including age, the level of coverage, state, and the company providing the insurance. The cost of medical care in each state can also change how much a health insurance policy costs.

The average cost of an Obamacare plan varies depending on the age of the insured. For a 30-year-old, the average cost is $483 per month, for a 40-year-old it is $544, and for a 50-year-old, it is $760 per month. The national average premium increased by 129% from 2013 to 2019.