When it comes to life insurance, there are a number of options to choose from. The best life insurance policy for you will depend on your specific situation, needs and goals. Term life insurance is the most straightforward and cost-effective type of policy, and the best life insurance companies offer a range of policies, including term and permanent coverage.

| Characteristics | Values |

|---|---|

| Cost-effective | Term life insurance |

| Straightforward | Term life insurance |

| Range of policies | Term and permanent coverage |

Explore related products

What You'll Learn

![]()

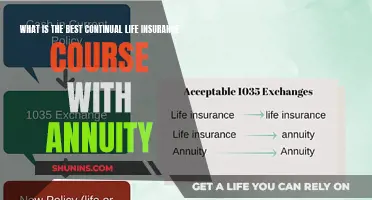

Term and permanent life insurance policies

When it comes to life insurance, there are two main types of policies: term and permanent. Term life insurance is the most straightforward type of policy to understand. You simply select your desired coverage amount and duration, and the premium will remain the same for the entire term. This makes term policies predictable and easy to manage. However, the coverage will expire at the end of the term. Term life insurance is also the most cost-effective type of life insurance in the marketplace.

On the other hand, permanent life insurance offers coverage for your entire life, rather than a fixed term. This type of policy is more complex and can take several forms, including whole life, universal life, indexed universal life, and variable universal life. Permanent life insurance policies often have additional features, such as the ability to accumulate cash value over time, which can be borrowed against or withdrawn.

The best type of life insurance policy for you will depend on your specific situation, needs, and goals. Term life insurance may be a good option if you're looking for straightforward, affordable coverage for a fixed period. In contrast, permanent life insurance could be more suitable if you want lifelong coverage and are interested in the additional features and benefits that this type of policy can offer.

Some of the best life insurance companies, according to recent analyses, include MassMutual, Pacific Life, and Protective. These companies offer a range of term and permanent life insurance policies, allowing you to choose the one that best suits your needs. You can also get free quotes and compare life insurance policies to find the right one for you.

Life Insurance Payouts: Are They Taxable in France?

You may want to see also

Explore related products

![]()

Financial strength of life insurance companies

When choosing a life insurance policy, it is important to consider the financial strength of the company offering it. The best life insurance companies stand out for their financial strength and coverage options.

Term life insurance is the most cost-effective type of life insurance in the marketplace. Most term policies have premiums that remain the same for the entire term duration, making them predictable and easy to manage. Term insurance is also the most straightforward type of life insurance policy to understand. When setting up a term policy, you select your desired coverage amount and duration.

The best life insurance companies offer a range of policies, including term and permanent coverage. For example, Pacific Life offers both term and permanent life insurance policies, as well as a wide variety of universal, indexed universal, and variable universal life insurance policies.

It is important to consider your specific situation, needs, and goals when choosing a life insurance policy. By reading guides and using tools, you can gain a clear understanding of your options and secure a policy that is best suited for you.

VA Life Insurance: Cash Value and Benefits Explained

You may want to see also

Explore related products

![]()

Coverage options

When it comes to coverage options, there are a few different types of life insurance policies to choose from. Term life insurance is the most straightforward and cost-effective type of policy. With term life insurance, you select the coverage amount and duration, and the premium remains the same for the entire term. This makes term life insurance transparent, predictable, and easy to manage.

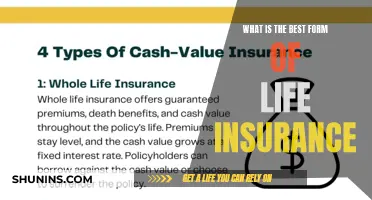

Another option is permanent life insurance, which includes whole life insurance and universal life insurance. While permanent life insurance policies are more expensive than term life insurance policies, they offer longer-term coverage and can be a good option for those who want lifelong protection. Universal life insurance, in particular, offers flexibility in terms of coverage and premiums.

When deciding on a life insurance policy, it's important to consider your specific situation, needs, and goals. The best life insurance companies offer a range of coverage options, including term and permanent policies, so you can choose the one that best suits your needs. Some companies also offer life insurance policies without a medical exam, which can be convenient for those who want to avoid the hassle of undergoing a medical evaluation.

Government Life Insurance: Are Refunds Possible?

You may want to see also

Explore related products

![]()

Average cost of life insurance

The best life insurance policy for you will depend on your specific situation, needs, and goals. Term insurance is the most straightforward type of life insurance policy to understand. When setting up a term policy, you select your desired coverage amount and duration. The duration of your coverage will determine when your coverage expires. Term life is also the most cost-effective type of life insurance in the marketplace. Most term policies have premiums that will remain the same for the entire term duration. This transparent setup makes term policies predictable and easy to manage.

The average cost of life insurance is $26 a month, according to Covr Financial Technologies. This is based on a healthy 40-year-old buying a 20-year, $500,000 term life insurance policy. However, the average cost of life insurance per month can vary depending on the type of plan you own. For example, a 20-year, $250,000 term life insurance policy for a healthy 30-year-old costs under $200 per year on average, while a 10-year, $250,000 term life insurance policy for a healthy 20 to 40-year-old is typically between $24 and $29 per month. The average cost of a 20-year term life insurance policy with a $500,000 payout is $30 for 30-year-old males and $23 for 30-year-old females. Whole life insurance is typically more expensive, with the same policy costing approximately $450 monthly.

Understanding Life Insurance Benefits and Their Basis

You may want to see also

Explore related products

![]()

Medical exams

When it comes to choosing the best life insurance policy, there are a few key factors to consider. The best life insurance companies offer a range of policies, including term and permanent coverage. Term life insurance is the most cost-effective and straightforward type of life insurance, making it a popular choice for many. However, it's important to remember that your specific situation, needs, and goals should dictate the type of policy you choose.

The results of the medical exam can impact the cost of your life insurance policy. If you are in good health, you may qualify for a lower premium. On the other hand, if you have pre-existing health conditions or risk factors, your premium may be higher. It's important to be honest and accurate during the medical exam process, as providing false information can lead to issues with your policy down the line.

While the thought of a medical exam may be daunting for some, it's important to remember that it is a standard part of the life insurance application process. By being prepared and knowing what to expect, you can approach the exam with confidence. Additionally, some companies may offer simplified issue policies that require a shorter medical questionnaire instead of a full exam, which can be a good alternative for those who are hesitant about undergoing a comprehensive medical evaluation.

Overall, while medical exams play a role in the life insurance application process, they are just one factor among many that insurance companies consider when determining your eligibility and premium. By understanding the purpose and process of these exams, you can make informed decisions about your life insurance choices and find a policy that best suits your needs and provides peace of mind for you and your loved ones.

Life Insurance and Divorce: Who Gets the Payout?

You may want to see also

Frequently asked questions

The best life insurance policy for you will depend on your specific situation, needs, and goals. Term insurance is the most straightforward type of life insurance policy to understand. When setting up a term policy, you select your desired coverage amount and duration. The duration of your coverage will determine when your coverage expires. Term life is also the most cost-effective type of life insurance in the marketplace.

Term life insurance is the most cost-effective type of life insurance in the marketplace. Most term policies have premiums that will remain the same for the entire term duration. This transparent setup makes term policies predictable and easy to manage.

MassMutual is the best life insurance company of 2025, based on an analysis by U.S. News. Pacific Life and Protective are also highly rated.

The average cost of life insurance is $26 a month, according to Covr Financial Technologies. This figure is based on a healthy 40-year-old buying a 20-year, $500,000 term life insurance policy.