Medicare coinsurance is a cost-sharing device that comes into effect after deductibles have been met, requiring beneficiaries to cover a portion of their healthcare costs. The co-insurance percentage for Medicare is typically 20% of the Medicare-approved amount for most services, with Medicare covering the remaining 80%. This percentage can vary depending on the plan chosen, with some plans offering more coverage and reducing the coinsurance responsibility. Coinsurance is different from copayments, where beneficiaries pay a set fee for a service, such as $15 for a primary care visit.

| Characteristics | Values |

|---|---|

| Definition | Coinsurance is a cost-sharing device that comes into effect after deductibles have been met, requiring you to cover a portion of your healthcare costs. |

| Difference from other Medicare costs | The main difference between Medicare coinsurance and other Medicare costs has to do with the timing and intention. Premiums are regular monthly payments, and deductibles are fixed amounts beneficiaries pay before Medicare kicks in. |

| Coinsurance vs copayments | Coinsurance is a percentage of the Medicare-approved amount for a service, whereas copayments are a set fee for a service. |

| Coinsurance calculation | Coinsurance = (Medicare-approved amount for the service) x (percentage you’re responsible for). |

| Coinsurance percentage | The coinsurance percentage varies depending on the plan chosen. For most services covered by Medicare Part B, the coinsurance is 20% of the Medicare-approved amount. Medicare Part A does not use percentage-based coinsurance. |

| Out-of-pocket limit | The out-of-pocket limit for in-network care in 2025 is $9,350, plus the cost of prescriptions. |

| Medicare Advantage plans | Medicare Advantage plans (Part C) typically have cost-sharing in the form of fixed copayments rather than coinsurance. |

Explore related products

What You'll Learn

![]()

Medicare Part B coinsurance

Original Medicare (Parts A and B) covers most of your medical costs, but not all. With coinsurance, you pay a fixed percentage of the cost of every medical service you receive, and your insurance company pays the remaining percentage. This is different from a copay or copayment, where you pay a set fee for a service.

Medicare Part B (Medical Insurance) helps cover two types of services: medically necessary services and preventive services. Medically necessary services are services or supplies that meet accepted standards of medical practice to diagnose or treat your medical condition. Preventive services are healthcare to prevent illness (like the flu) or detect it at an early stage when treatment is likely to work best. You pay nothing for most preventive services if you get them from a healthcare provider who accepts assignments.

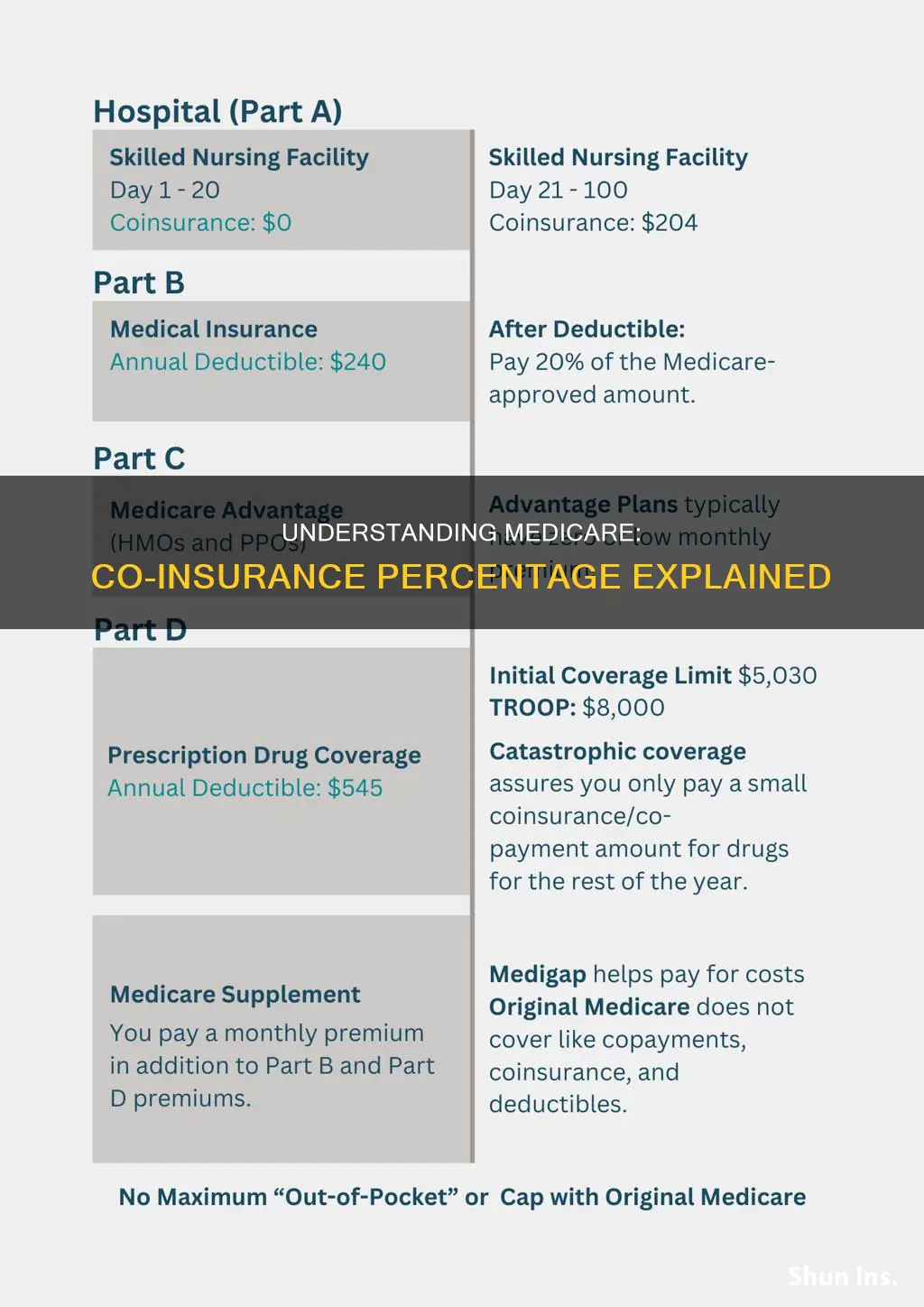

With Medicare Part B, after you meet your deductible, you typically pay 20% coinsurance of the Medicare-approved amount for most outpatient services and durable medical equipment. For example, if you're enrolled in Original Medicare and you visit your doctor for a $500 outpatient treatment, your doctor will bill Medicare for $500. In 2024, Part B carries an annual deductible of $240, so you’re responsible for paying this amount toward Part B-covered services for the year. After paying the Part B deductible, the remaining $260 of your bill is covered in part by Medicare and in part through coinsurance. Your share is 20% coinsurance of $52, and Medicare Part B’s share is 80%, or $188. On the next $500 bill for the same treatment from the same doctor, you’ll have already paid your Part B deductible, so Medicare will pay 80% ($400), and you will pay 20% ($100).

Coinsurance costs can be covered by purchasing a Medicare supplement (Medigap) plan. All Medicare Advantage plans have an out-of-pocket maximum, a set amount that you will pay out of pocket. Once you spend this amount, the insurance company will cover any other costs for the year at 100%.

Medical Leave and Job Security: Can You Be Fired?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Coinsurance vs copayments

Coinsurance and copayments (or copays) are both out-of-pocket expenses that are associated with an insurance plan. However, they are not the same thing. A copayment is a fixed cost or flat fee that a patient pays for a specific service covered by their insurance. It is a set dollar amount that is paid each time a service is received, such as a doctor's visit or filling a prescription. Copayments are usually paid at the time of service and do not apply to the deductible. The amount of a copayment is predetermined and can be found on an insurance ID card.

Coinsurance, on the other hand, is a percentage of the cost of a service that the patient pays. It is calculated as a percentage of an eligible health expense and varies depending on the type, size, and scope of services. Coinsurance comes into effect after deductibles have been met, requiring the patient to cover a portion of their healthcare costs. For example, an 80/20 health insurance plan means that the insurance will cover 80% of the cost, and the patient is responsible for the remaining 20%. The percentage can vary depending on the plan and care type, with policyholders typically paying between 10% and 40% of their medical costs.

Some plans may use both copayments and deductibles/coinsurance, depending on the type of covered service. Patients requiring frequent care may opt for a plan with lower copayments and coinsurance, while those who infrequently use medical services may choose a plan with higher copayments and coinsurance. Additionally, higher insurance premiums are associated with lower out-of-pocket expenses, including deductibles, copayments, and coinsurance.

In the context of Medicare, coinsurance refers to the portion of healthcare expenses that beneficiaries are responsible for paying after they have met their annual deductible. It is typically calculated as a percentage of the total cost of a covered service or medical supply, with Medicare covering the remaining percentage. For most services covered by Medicare Part B, the coinsurance is 20% of the Medicare-approved amount.

Switching Insurance: Moving from Medicaid to Blue Cross

You may want to see also

Explore related products

![]()

Coinsurance and deductibles

Coinsurance

Coinsurance is a cost-sharing mechanism in Medicare. It represents the portion of healthcare expenses that beneficiaries are responsible for paying after they have met their annual deductible. In simple terms, it is the percentage of the Medicare-approved cost of a covered health care service that you are expected to pay. This percentage can vary depending on the plan chosen and the specific service received. For example, for most services covered by Medicare Part B, the coinsurance is typically 20%, meaning the patient pays 20% while Medicare pays the remaining 80%.

Deductibles

A deductible refers to the amount you need to spend for eligible healthcare expenses before your insurance coverage kicks in. In other words, it is the amount you pay out of pocket before your insurance company starts contributing to the cost of your healthcare services. For example, if you have a $2,000 deductible, you will need to pay the first $2,000 of covered services yourself. Once you have met this deductible, coinsurance comes into effect, and you will share the costs with your insurance provider.

Choosing a Plan

When selecting a Medicare plan, it's essential to understand the specifics of how the plan works, including the percentage of coinsurance you will be responsible for, the services that are subject to coinsurance, and the out-of-pocket spending limit. Some plans may offer more coverage, reducing your coinsurance responsibility. Additionally, Medigap plans can help pay some or all of the coinsurance for Medicare Part B and cover various out-of-pocket costs under Medicare Part A.

Tanner Hospital's Accepted Medical Insurance Plans: What You Need to Know

You may want to see also

Explore related products

![]()

Coinsurance and premiums

Coinsurance refers to the percentage of the Medicare-approved cost of healthcare services that a beneficiary is expected to pay after meeting their plan deductible. It is a cost-sharing device that comes into effect after deductibles have been met, requiring beneficiaries to cover a portion of their healthcare costs. This percentage can vary depending on the plan chosen, with some plans offering more coverage and reducing the coinsurance responsibility.

For instance, in 2025, the standard Part B monthly premium is $185, and the Part B deductible is $257 per year. After meeting the deductible, the Part B coinsurance, or the beneficiary's share, is 20% of the cost for each Medicare-approved service or item. This means that for most services covered by Medicare Part B, the beneficiary pays 20% while Medicare pays 80%.

Medicare Part A does not use percentage-based coinsurance. However, Medicare Advantage plans (Part C) share costs with plan members, but it is usually in the form of a fixed copayment rather than coinsurance. In 2025, the average Medicare Advantage/Part C premiums are projected to range between $0 and $240, with the average plan costing $17 per month.

It is important to note that coinsurance is different from copayments or copays, where beneficiaries pay a set fee for a service, such as $15 for a primary care visit. Coinsurance, on the other hand, is a percentage of the Medicare-approved amount for a service and is often used for Medicare Part B services, including doctor visits and outpatient care.

The Lodge at Loveland, Ohio: Accepting Medicaid Insurance?

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)

![]()

Coinsurance and out-of-pocket costs

Coinsurance is a cost-sharing device that comes into effect after deductibles have been met. It is the portion of healthcare expenses that beneficiaries are responsible for paying after they have met their annual deductible. It is calculated as a percentage of the total cost of a covered service or medical supply, with Medicare covering the remaining amount. Coinsurance is often used for Medicare Part B services, like doctor visits and outpatient care.

The percentage of coinsurance varies depending on the plan. For most services covered by Medicare Part B, the coinsurance is 20% of the Medicare-approved amount, meaning the patient pays 20% and Medicare pays 80%. However, Part A does not use percentage-based coinsurance.

Medigap (Supplemental Insurance) plans can help cover the coinsurance that beneficiaries would otherwise have to pay for Medicare Part B. These plans are sold by private carriers and can also help with out-of-pocket costs under Medicare Part A. The price of a Medigap plan determines how much the beneficiary will pay in out-of-pocket costs.

Medicare Advantage (Part C) plans also have cost-sharing in the form of a fixed copayment for doctor's visits, rather than the 20% coinsurance of Part B. In 2025, the average Medicare Advantage/Part C premiums are projected to range between $0 and $240, with the estimated average plan costing $17 per month.

Out-of-pocket costs refer to the expenses that beneficiaries must pay for covered health care services before their Medicare plan starts to pay. There is no yearly limit on what beneficiaries pay out-of-pocket unless they have supplemental coverage, like a Medigap policy, or they join a Medicare Advantage Plan. Out-of-pocket costs can include monthly premiums, yearly deductibles, copays, and coinsurance.

In 2025, the out-of-pocket maximum for Medicare Part D (Prescription Drug Coverage) is $2,000. This means that if a beneficiary takes high-cost medications covered by Part D, they could see major savings. Additionally, there are programs available to help with out-of-pocket costs, such as State Pharmaceutical Assistance Programs (SPAPs) and Pharmaceutical Assistance Programs (PAPs).

How Independent Medicare Insurance Companies Make Money

You may want to see also

Frequently asked questions

Coinsurance is a cost-sharing device that comes into effect after deductibles have been met, requiring you to cover a portion of your healthcare costs.

The co-insurance percentage is calculated as a percentage of the total cost of a covered service or medical supply, with Medicare covering the remaining percentage.

For most services covered by Medicare Part B, the co-insurance percentage is 20% of the Medicare-approved amount, meaning the patient pays 20% and Medicare pays 80%.

Part A does not use percentage-based coinsurance.

Coinsurance and copayments are both ways beneficiaries share the cost of healthcare. Coinsurance is a percentage of the Medicare-approved amount for a service, whereas copayments are a set fee for a service, such as $15 for a primary care visit.