Medicare Advantage and Medicare Supplement Insurance (also known as Medigap) are two ways to fill Medicare coverage gaps and control costs. However, they differ in how they work and what they cover. Medicare Advantage is an alternative to Original Medicare, offered by private insurance companies, and usually includes Medicare Part A, B, and D coverage. It often has lower monthly premiums and may be a better option if you can't afford a Medigap plan. On the other hand, Medicare Supplement Insurance is additional insurance purchased from private carriers to fill the gaps in Original Medicare coverage. It provides more flexibility, allowing you to see any doctor that accepts Medicare, but you'll have to pay a supplemental insurance premium on top of your regular Medicare premiums.

| Characteristics | Values |

|---|---|

| Medicare Advantage | An alternative to Original Medicare, offered by private insurance companies |

| Medicare Supplement Insurance (Medigap) | Extra insurance to help pay your share of costs in Original Medicare |

| Medicare Advantage coverage | Combines Medicare Part A and B for comprehensive coverage, all in one plan. It often includes Part D prescription drug coverage, too. |

| Medigap coverage | Helps pay the out-of-pocket expenses not covered by Original Medicare (Part A and B). It is not part of the government's Medicare program but provides coverage in addition to it. |

| Flexibility | Medigap gives you the freedom to see any doctor that accepts Medicare. Medicare Advantage plans often have lower monthly premiums, but you'll usually have to go to providers in your plan's network. |

| Cost | Medicare Advantage premiums, deductibles and other costs can vary by plan and change each year. You must pay the Part B premium ($185 in 2025) and keep paying it to stay in your plan. |

| Medigap costs | You must have Part A and Part B to buy a Medigap policy. Medigap policies are standardized, and in most states, named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, no matter which insurance company sells it. Price is the only difference between policies with the same letter sold by different companies. |

| Switching plans | You can't switch from Medigap to Medicare Advantage at any time. You'll have to wait for the Medicare Open Enrollment Period, which runs from Oct 15 to Dec 7 each year. |

Explore related products

What You'll Learn

- Medicare Advantage combines Part A and B, with some plans covering Part D

- Medicare Supplement Insurance (Medigap) helps pay for costs not covered by Original Medicare

- Medigap policies are automatically renewed annually, even with health problems

- Medicare Advantage is an alternative to Original Medicare, offered by private insurers

- Medicare Supplement Insurance plans set a maximum out-of-pocket limit

![]()

Medicare Advantage combines Part A and B, with some plans covering Part D

Medicare Advantage, also known as Part C, is an alternative to Original Medicare. It combines Part A (Hospital Insurance) and Part B (Medical Insurance) into a single plan. This means that, with Medicare Advantage, you can receive all your healthcare coverage in one place.

Medicare Advantage is offered by private insurance companies that have contracted with the federal government. It is important to note that you must be enrolled in both Part A and Part B to be eligible for Medicare Advantage. Additionally, you will still need to pay your Part B premium, which is $185 per month in 2025, along with a monthly Medicare Advantage premium.

Medicare Advantage plans often include extra benefits that are not available with Original Medicare. Many plans include Part D prescription drug coverage, and some may also offer routine dental, vision, and hearing services. These additional benefits can provide comprehensive healthcare coverage for individuals seeking an all-in-one solution.

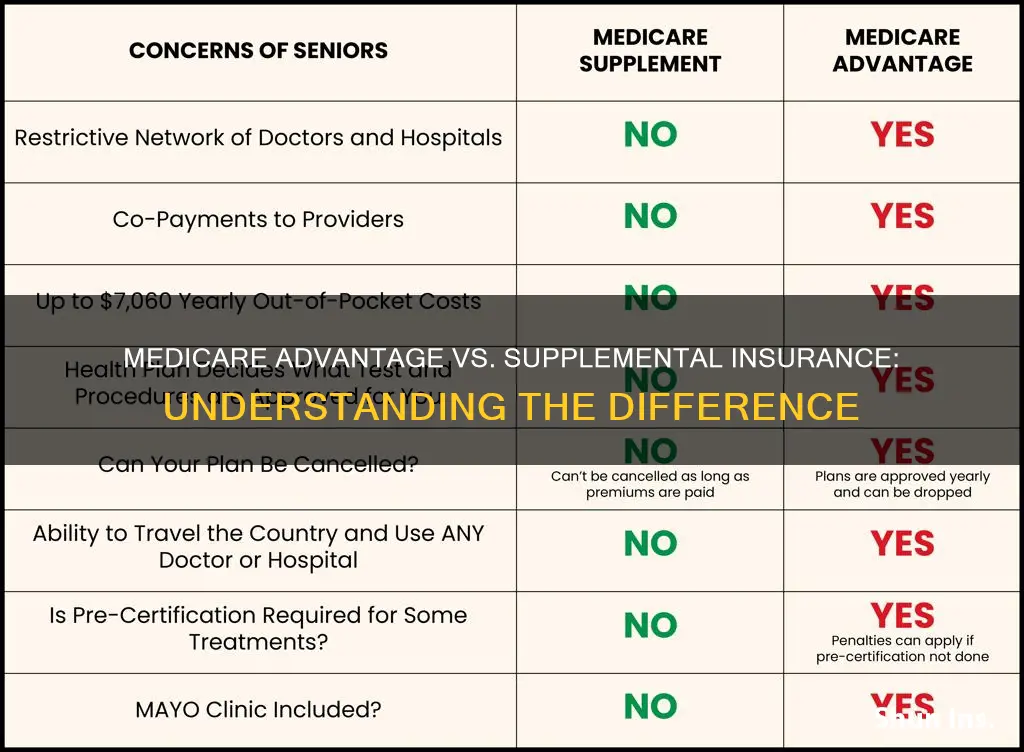

It is worth mentioning that Medicare Advantage plans may have provider restrictions. You will likely need to use doctors and hospitals within your plan's network, and accessing out-of-network care can be more expensive.

Medicare Advantage offers flexibility in terms of coverage options. While some plans may have lower monthly premiums, the out-of-pocket limit can vary. Once you reach this limit, your plan will typically cover 100% of your healthcare services for the remainder of the year.

In summary, Medicare Advantage combines Part A and Part B, providing a comprehensive single-plan solution. With the inclusion of Part D in many cases, along with potential extra benefits, Medicare Advantage offers a convenient way to manage your healthcare needs.

Utilizing Medicaid Benefits with Additional Insurance Coverage

You may want to see also

Explore related products

![]()

Medicare Supplement Insurance (Medigap) helps pay for costs not covered by Original Medicare

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can buy from a private company to help pay for costs not covered by Original Medicare (Parts A and B). Medigap policies help cover some out-of-pocket expenses that Original Medicare doesn't pay for, such as deductibles, copays, and coinsurance. For example, if you have a Medigap policy and receive care, Medicare will pay its share of the Medicare-approved amount for covered health care costs. Your Medigap policy will then pay your doctor whatever amount you owe under your policy, and you are responsible for any remaining costs.

Medigap policies are typically purchased in addition to Original Medicare coverage. You must be enrolled in Original Medicare (Part A and Part B) to purchase Medigap. It is important to note that Medigap is not part of the government's Medicare program, and you cannot have both Medigap and a Medicare Advantage Plan at the same time.

Medigap provides flexibility in choosing your healthcare providers, as it allows you to see any doctor that accepts Medicare. In contrast, Medicare Advantage plans often have lower monthly premiums but may require you to use providers within your plan's network.

Medigap policies do not cover all types of expenses. Generally, Medigap does not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Additionally, if you are under 65, you may face challenges in purchasing a Medigap policy or may have to pay higher premiums.

Medigap policies are standardized, and each policy offers the same benefits regardless of the insurance company selling it. The price is the main differentiating factor between Medigap policies offered by different companies. These policies are automatically renewed every year, even if your health status changes. However, your Medigap insurance company can drop you under certain circumstances.

Taiwan's Medical Insurance: A Comprehensive Coverage?

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UY218_.jpg)

![]()

Medigap policies are automatically renewed annually, even with health problems

Medigap, also known as Medicare Supplement Insurance, is a supplemental insurance that can be purchased to help pay for costs not covered by Original Medicare (Parts A and B). It is important to note that Medigap is not a replacement for Original Medicare but rather additional coverage. This means that you must have both Part A and Part B to be eligible to purchase a Medigap policy.

Medigap policies are standardized and automatically renewed annually, even if you experience health problems. Your Medigap insurance company can only drop you under specific circumstances. This provides peace of mind, knowing that your coverage will continue without interruption as long as you pay your Medigap premiums.

When you buy a Medigap policy, you agree to have the insurance company receive your Part B claim information directly from Medicare. Subsequently, your Medigap policy will pay your doctor any amount owed under your policy, and you will be responsible for any remaining costs.

It is worth mentioning that Medigap policies do not cover all types of expenses. For example, they typically do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Additionally, if you are under 65, purchasing a Medigap policy may be more challenging or costly.

When considering Medigap, it is essential to understand that you cannot simultaneously have it and be enrolled in a Medicare Advantage Plan. Medicare Advantage, also known as Part C, is an alternative to Original Medicare offered by private insurance companies. It combines Parts A and B into a single plan, often including Part D prescription drug coverage.

In conclusion, Medigap policies offer valuable supplemental coverage to Original Medicare and provide the assurance of automatic annual renewal, even with health issues. This feature ensures continuous protection for individuals who need it, making it a reliable option for those seeking additional coverage beyond what Original Medicare provides.

Sex Change Surgery: What Does Medical Insurance Cover?

You may want to see also

Explore related products

![]()

Medicare Advantage is an alternative to Original Medicare, offered by private insurers

Medicare Advantage, also known as Part C, is an alternative to Original Medicare. It is offered by private insurance companies that have contracted with the federal government. Medicare Advantage combines Medicare Part A (hospital insurance) and Part B (medical insurance) into a single plan, and often includes Part D prescription drug coverage.

Medicare Advantage plans may also offer extra benefits that aren't available with Original Medicare, such as routine dental, vision, and hearing services. These plans operate within networks of doctors and hospitals, and to receive the lowest-priced care, you must use in-network providers and facilities. If you can access out-of-network care, it is usually more expensive.

Medicare Advantage offers extra benefits and often has lower monthly premiums than Medicare Supplement Insurance. However, you will usually have to go to providers in your plan's network. In contrast, Medicare Supplement Insurance, also known as Medigap, gives you the freedom to see any doctor that accepts Medicare.

Medigap is supplemental coverage that helps pay for out-of-pocket expenses not covered by Original Medicare. It is not part of the government's Medicare program but is sold by private companies to fill "gaps" in Original Medicare. Medigap policies are standardised and automatically renewed every year, even if your health status changes.

You must have both Part A and Part B to be eligible for either Medicare Advantage or Medicare Supplement Insurance. You cannot have both at the same time, and if you switch between the two, you may lose your "guaranteed-issue" rights for Medigap.

Medical Insurance: Non-Compliance Penalties and Fines

You may want to see also

Explore related products

$94.34 $125

![]()

Medicare Supplement Insurance plans set a maximum out-of-pocket limit

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can buy from a private company to help pay your share of costs in Original Medicare. It is not part of the government's Medicare program but provides coverage in addition to it. Medigap policies help cover some costs that Original Medicare doesn't pay, such as deductibles, copays, and coinsurance. They also provide coverage for out-of-pocket expenses that Original Medicare doesn't cover.

Medigap policies are standardized, and in most states, they are named by letters like Plan G or Plan K. The benefits in each lettered plan are the same, no matter which insurance company sells it. The price is the only difference between policies with the same letter sold by different companies. Medigap policies do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Medigap insurance companies will pay your doctor directly for the Medicare-approved amount for covered health care costs. You are only responsible for any costs that are left. Medigap policies are automatically renewed every year, and you will keep your policy as long as you pay your premiums.

Medicare Supplement Insurance, or Medigap, offers flexibility as it allows you to see any doctor that accepts Medicare. In contrast, Medicare Advantage plans often have lower monthly premiums but may require you to use providers within your plan's network. With Medigap, you have the freedom to choose your healthcare providers without being restricted to a specific network. This flexibility can be crucial in ensuring you receive the care you need from your preferred healthcare professionals.

Medical Marijuana Insurance Coverage: What's the Deal?

You may want to see also

Frequently asked questions

Medicare Advantage is an alternative to Original Medicare and combines Medicare Part A and Part B into one plan. It is offered by private insurance companies and often includes Medicare Part D prescription drug coverage.

Medicare Supplemental Insurance, also known as Medigap, is extra insurance that helps pay for costs not covered by Original Medicare. It is sold by private companies to fill gaps in Original Medicare and gives you the freedom to see any doctor that accepts Medicare.

Medicare Advantage is an all-in-one policy that replaces Original Medicare, while Medicare Supplemental Insurance is extra insurance that can be purchased to cover costs that Original Medicare doesn't pay. Medicare Advantage plans often have lower monthly premiums, but you must use providers in your plan's network. With Medicare Supplemental Insurance, you can see any doctor that accepts Medicare, but you must be enrolled in Original Medicare to purchase it.