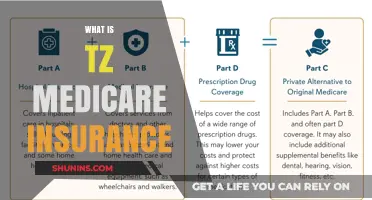

Medicare is a health coverage option for individuals, and there are two main ways to get it: Original Medicare and Medicare Advantage. Original Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance), covering inpatient hospital care, doctors' services, and tests. Medicare Advantage combines Part A, Part B, and often Part D (drug coverage) into one plan, with extra benefits like vision, hearing, and dental services. It is provided by private companies that follow Medicare-set rules. When an individual has Medicare and other health insurance, one is the primary payer and the other is the secondary payer. The primary payer pays up to its limit, then sends the remaining balance to the secondary payer. Medicare doesn't offer couple or family plans, and individuals must sign up for Part A and Part B separately.

| Characteristics | Values |

|---|---|

| Medicare Coverage | Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) |

| Medicare Advantage | Bundles Part A, Part B, and usually Part D (drug coverage) into one plan |

| Medicare Drug Coverage | Optional and available to everyone with Medicare |

| Medicare Cost | Medicare pays part of the cost and you pay your share |

| Medicare for Non-US Residents | Medicare won't pay for Part A and Part B claims for those not lawfully present in the US |

| Medicare and Medicaid | Medicaid covers nursing home care and personal care services, which Medicare does not |

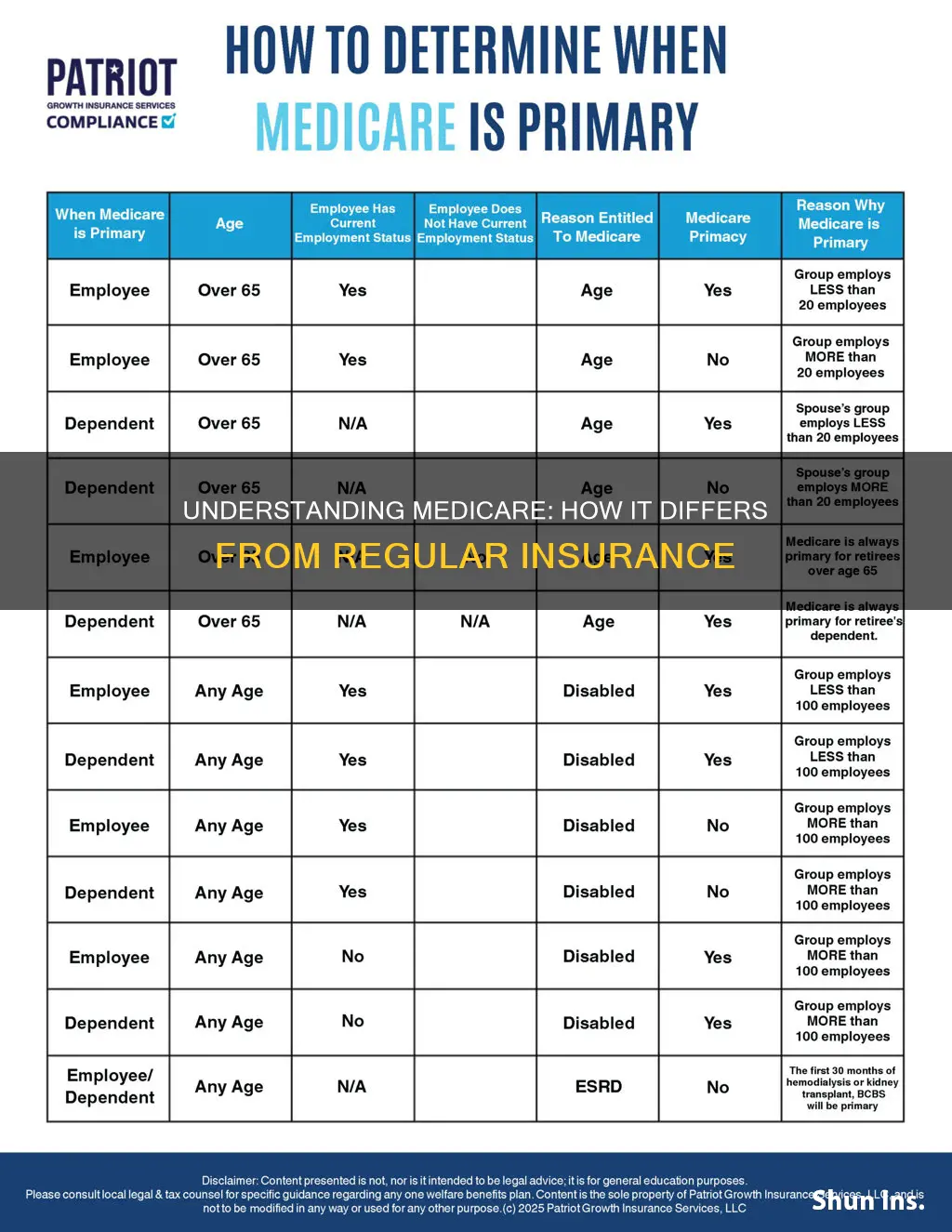

| Medicare and Other Insurance | If you have other insurance, which pays first depends on factors like your employment status, type of insurance, and health situation |

| Medicare and Couples/Families | Medicare does not offer plans for couples or families |

Explore related products

What You'll Learn

- Medicare doesn't offer family plans, unlike regular insurance

- Medicare Part A and B are mandatory for buying supplemental Medigap policies

- Medicare Advantage bundles Parts A, B, and D, with extra benefits like vision and dental

- Medicare doesn't cover long-term care, routine physicals, or dentures

- Medicare and other insurance have a primary and secondary payer system

![]()

Medicare doesn't offer family plans, unlike regular insurance

Medicare is a government-provided health insurance programme that differs from private insurance in several ways, including the absence of family plans. While regular insurance often provides the option to cover your spouse or family under the same policy, Medicare does not offer this benefit.

With Medicare, individuals are limited to enrolling in plans that cover only themselves. This means that spouses or partners must enrol separately and choose their own Medicare coverage options. This can result in a couple or family having different types of coverage, depending on their individual needs and preferences.

Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance), is one of the primary options available. It covers most of the approved health care services and supplies but not all. For additional benefits, individuals can opt for Medicare Advantage, which bundles Part A, Part B, and often Part D (drug coverage) into a single plan. However, unlike regular insurance, Medicare Advantage does not typically allow enrollees to join a separate drug plan.

The lack of family plans in Medicare can impact the cost and convenience of healthcare for families. Each family member must enrol and pay for their own coverage, potentially resulting in higher overall expenses. Additionally, managing multiple plans can be more complex than a single family plan offered by regular insurance providers.

It is important to note that Medicare works differently with other types of insurance. If an individual has Medicare and other health insurance, the coordination of benefits determines which insurance pays first. The primary payer covers up to its limits and then sends the remaining balance to the secondary payer. This process can impact the overall cost and coverage for individuals with multiple insurance plans, including those with family members on separate insurance policies.

Get Medical Insurance After Deadline: What Are Your Options?

You may want to see also

Explore related products

![]()

Medicare Part A and B are mandatory for buying supplemental Medigap policies

Medicare is a federal health insurance program primarily for people aged 65 and over, but it also applies to younger people with disabilities or those with End-Stage Renal Disease (ESRD). Original Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance). If you choose Original Medicare, you can also decide if you want drug coverage (Part D) and supplemental coverage, like Medigap.

Medicare Supplement Insurance, or Medigap, is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare. Medigap policies are standardized, meaning that policies with the same letter offer the same basic benefits, regardless of the insurance company. It's important to note that Medigap is only available to those with Original Medicare, and you must have both Part A and Part B to be eligible for Medigap. This means signing up for both parts of Original Medicare before purchasing a Medigap policy. Additionally, Medigap policies only cover one person, so spouses would each need their own policy.

When you have Medicare and other health insurance, such as from an employer or retiree coverage, each type of coverage is called a "payer." The "primary payer" pays up to its coverage limit and then sends the remaining balance to the "secondary payer." If there are still costs remaining after the secondary payer pays, the patient may be responsible for covering those costs.

It is important to understand the differences between regular insurance and Medicare when considering supplemental Medigap policies. Medigap is specifically designed to supplement Original Medicare and cannot be used in conjunction with a Medicare Advantage Plan. Medicare Advantage Plans are an alternative to Original Medicare, and they typically bundle Part A, Part B, and sometimes Part D into a single plan offered by Medicare-approved private companies. These plans may offer additional benefits that Original Medicare does not cover, such as vision, hearing, and dental services.

In summary, Medicare Part A and Part B are mandatory for buying supplemental Medigap policies. This is because Medigap is designed to supplement the coverage provided by Original Medicare, and it requires both parts to be in place before it can be purchased.

Veteran Status on Medical Insurance Cards: What You Need to Know

You may want to see also

Explore related products

![]()

Medicare Advantage bundles Parts A, B, and D, with extra benefits like vision and dental

Regular insurance differs from Medicare in several ways. Firstly, Medicare is not offered as a plan for couples or families, whereas private insurance often includes family plans. Secondly, Medicare works in conjunction with other insurance policies, whereas regular insurance typically does not. When an individual has Medicare and another form of insurance, Medicare is considered the "primary payer", covering costs up to its limit, with the other insurance acting as the "secondary payer" for any remaining balance.

Medicare Advantage, also known as Part C, is an alternative to Original Medicare (Parts A and B) that bundles hospital insurance (Part A), medical insurance (Part B), and prescription drug coverage (Part D) into a single plan. Medicare Advantage plans are offered by Medicare-approved private companies that must adhere to Medicare's rules. These plans often include extra benefits that Original Medicare does not cover, such as vision, hearing, and dental services.

Medicare Advantage plans vary, and each plan can have different rules for how you access services, such as requiring referrals to see a specialist. Costs for monthly premiums and services vary depending on the specific plan chosen. It is important to note that most Medicare Advantage plans do not allow enrollees to join a separate Medicare drug plan. Additionally, Medicare Advantage plans must cover all emergency and urgent care, as well as almost all medically necessary services that Original Medicare covers.

When considering Medicare Advantage, it is essential to consult with your employer, union, or benefits administrator, as enrolling in a Medicare Advantage plan might result in the loss of your existing employer or union coverage. It is also worth noting that insurance companies can decide to join or leave Medicare annually, which may require you to switch plans or return to Original Medicare.

How Medicare and Medicaid Changes Affect Private Insurance

You may want to see also

Explore related products

$15.75

![]()

Medicare doesn't cover long-term care, routine physicals, or dentures

Medicare is a government-provided health insurance plan that covers most, but not all, of the costs for approved health care services and supplies. It is different from private insurance in that it does not offer plans for couples or families. Individuals must sign up for Medicare Parts independently. Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) are included in Original Medicare.

Original Medicare does not cover long-term care, routine physicals, or dentures. Long-term care refers to extended care services, typically for the elderly or those with chronic illnesses, which help with daily activities like eating, bathing, and dressing. Routine physicals, also known as annual check-ups or wellness exams, are preventative care visits that typically include measurements of vital signs, discussions about health concerns, and screenings for conditions like cancer or diabetes. Dentures, on the other hand, are prosthetic devices used to replace missing teeth and restore an individual's ability to eat and speak properly.

While Original Medicare does not cover these services, there are alternative options to consider. For long-term care, individuals may need to pay out of pocket or look into Medicare Advantage Plans (Part C), which may offer more comprehensive coverage for such services. Routine physicals may be covered by some Medicare Advantage Plans, and certain Medicare Advantage Plans may also provide dental benefits that include coverage for dentures.

It is important to note that Medicare Advantage Plans are offered by Medicare-approved private companies and may have different rules and costs associated with them. These plans must cover all emergency and urgent care, as well as almost all medically necessary services that Original Medicare covers. However, they may have additional benefits, such as vision, hearing, and dental services, which Original Medicare typically does not include.

Understanding Hardship Exemptions for Medical Insurance Coverage

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare and other insurance have a primary and secondary payer system

Medicare is US government-provided insurance for individuals over 65, whereas regular insurance is provided by private companies and can cover couples and families. Medicare offers Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance), and Medicare Advantage (Part C), which bundles Part A, Part B, and usually Part D (drug coverage) into one plan.

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limit of its coverage and then sends the remaining balance to the "secondary payer". If the "secondary payer" does not cover the remaining balance, the individual may be responsible for the remaining costs. This order of payment is called "coordination of benefits".

The primary payer is the insurance that has the primary responsibility for paying a claim. The secondary payer only pays if there are costs that the primary insurance did not cover. Medicare is the primary payer in certain instances, such as for individuals over 65 with an employer retirement plan, and the secondary payer in other instances, such as when an individual has a workers' compensation claim.

If the insurance company does not pay the claim promptly, your doctor or other providers may bill Medicare. In this case, Medicare may make a conditional payment to pay the bill and then recover any payments the primary payer should have made. A conditional payment is a payment Medicare makes for services that another payer may be responsible for. Medicare makes this payment so that the beneficiary does not have to use their own money to pay the bill. However, the beneficiary must repay Medicare once a settlement, judgement, award, or other payment is made.

Understanding Medical Insurance Acceptance Complexities

You may want to see also

Frequently asked questions

Medicare is provided by the US government and is specifically for individuals over 65, whereas regular insurance can be provided by private companies and can cover couples and families. Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance). Medicare Advantage bundles Part A, Part B, and usually Part D (drug coverage) into one plan.

Original Medicare covers inpatient hospital care, doctors' services and tests, and preventive services. Medicare Advantage may offer additional benefits like vision, hearing, and dental services.

There are two main ways to get your Medicare coverage: Original Medicare and Medicare Advantage. You can choose which way you want to get your health coverage each year.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)