Medicare supplement insurance, also known as Medigap, is extra insurance that individuals can purchase from private health insurance companies to help pay for costs that Original Medicare (Part A and Part B) does not cover. Medigap plans are available in 10 letter designations (A through D, F, G, and K through N), with each plan offering a different set of benefits. The most popular Medigap plan is Plan F, which covers Medicare Part A hospital deductible and co-payments, Part B deductible, and some emergency care outside the US. However, Plan F is only available to those who became eligible for Medicare before January 1, 2020. For new enrollees, Plan G is considered the best option due to its comprehensive coverage, which is similar to Plan F but excludes the Medicare Part B deductible. When choosing a Medigap plan, individuals should consider their health status, travel plans, budget, and the availability of plans in their state.

| Characteristics | Values |

|---|---|

| Name of the most popular Medicare supplement insurance | Plan F |

| Reason for popularity | Offers the most coverage of any Medicare Supplement option, covers the Medicare Part A hospital deductible and co-payments, the Part B deductible, and some emergency care outside the U.S. |

| Other popular plans | Plan G, Plan C, Plan K, Plan L, Plan N |

| Best overall plan | AARP/UnitedHealthcare Medicare Supplement Insurance |

| Best for low prices | Wellabe Medicare Supplement Insurance |

| Best for additional coverage options | Anthem Medicare Supplement Insurance |

| Best for high-deductible Medigap Plan G | Mutual of Omaha Medicare Supplement Insurance |

| Average cost of Medigap plans in 2025 | $148 per month |

| Average cost of Medigap Plan G in 2025 | $159 per month for a 65-year-old woman who doesn't smoke |

Explore related products

![]()

Plan F

Medicare supplement insurance, also known as Medigap, is private supplemental health insurance that helps cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance. Medigap plans are administered by private insurance companies and come in 10 letter designations (A through D, F, G, and K through N). Each plan with the same letter offers identical coverage, but prices can vary based on the insurance provider.

It's important to note that Plan F has a high-deductible option, where individuals must pay for Medicare-covered costs (coinsurance, copayments, and deductibles) up to a certain amount before the plan coverage kicks in. This option typically results in lower premiums but could lead to higher out-of-pocket expenses if extensive benefits are utilized.

When considering Plan F or any other Medigap plan, it's essential to evaluate your personal circumstances, anticipated medical needs, and financial situation. The best time to purchase a Medigap policy is during your open enrollment period, as pre-existing conditions may impact eligibility or pricing outside of this period.

Switching Insurance: Medical to Regular Health Coverage

You may want to see also

Explore related products

![]()

Plan G

Medicare supplement insurance, also known as Medigap, helps cover the costs that original Medicare plans don't. Medigap plans are administered by private insurance companies and come in 10 letter designations (A through D, F, G, and K through N). All plans with the same letter offer the same coverage, but prices vary based on the insurance provider.

The best Medigap company offering Plan G is AARP/UnitedHealthcare, which has cheap rates and good service. The average cost of Plan G in 2025 is $159 per month for a 65-year-old non-smoking woman.

Self-Employed and Medical Insurance: How Much Does It Cost?

You may want to see also

Explore related products

![]()

Plan N

Medicare Supplement insurance plans, more commonly known as Medigap, are administered by private insurance companies. There are 10 Medigap plans, designated with letters from A to N, with each plan offering a different set of benefits. Plan N is the third most popular Medigap plan, covering about 10% of all Medigap members.

While the core benefits of Plan N remain the same across insurance companies, the premium may vary depending on factors such as age, location, gender, and overall health. For instance, Cigna offers premium discounts of up to 25% for qualified applicants in certain states. It's important to note that Plan N, like other Medigap plans, is not connected with or endorsed by the U.S. government or the federal Medicare program.

Get Medical Insurance in Madison, Wisconsin: A Guide

You may want to see also

Explore related products

![]()

Medigap vs Medicare Advantage

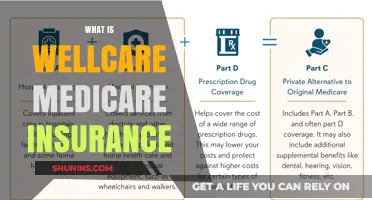

Medicare Supplement Insurance, also known as Medigap, is private supplemental health insurance that fills the gaps in Original Medicare. Medigap plans are administered by private insurance companies and come in 10 letter designations (A through D, F, G, and K through N). Each plan with the same letter offers identical coverage, but prices can vary based on the insurance company. Medigap policies can be purchased at any time if you have Medicare Part A and Part B, but insurers in most states can reject you or charge more if you have pre-existing conditions unless you buy during certain periods, such as within six months of enrolling in Medicare Part B if you're 65 or older.

Medigap provides flexibility, allowing you to see any doctor that accepts Medicare, and it comes with unlimited choices for care. However, it may not always be the most cost-effective option. For instance, Plan F, which is the most comprehensive Medigap plan, often costs more overall than Plan G, which has similar coverage except for the Medicare Part B deductible. Moreover, Medigap plans sold after 2005 do not include prescription drug coverage, so you may need to purchase a separate plan for that.

On the other hand, Medicare Advantage, also known as Medicare Part C, is an all-in-one alternative to Original Medicare, bundling Medicare Part A, Part B, and often Part D (prescription drug coverage). It is offered by private health insurers and typically operates within a network of doctors and hospitals. Medicare Advantage plans often have lower monthly premiums, but you usually have to use in-network providers, and going out of network can be more expensive. Additionally, Medicare Advantage may offer extra benefits such as dental, vision, and hearing coverage.

When deciding between Medigap and Medicare Advantage, consider your priorities regarding flexibility in provider choice, monthly premiums, out-of-pocket costs, and the range of benefits offered.

Labiaplasty: Is It Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

Medigap enrollment by state

Medigap, or Medicare Supplement Insurance, helps beneficiaries manage the costs of original Medicare. Medigap covers the co-payments, deductibles and coinsurance that original Medicare doesn't. This is especially important for the 22% of older adults who face medical debt.

Medigap is private insurance, and its plans are labelled A through N, with each letter denoting a different level of coverage. The plans are administered by private insurance companies, and prices vary based on the company.

Medigap enrollment varies by state. In 2023, 9% of traditional Medicare beneficiaries in Hawaii had Medigap, while 67% in Iowa did. In 2016, the range was similar, with 3% in Hawaii and 51% in Kansas. In 2015, 25% of people in traditional Medicare had Medigap. States with higher Medigap enrollment tend to be in the Midwest and plains states.

In 2023, Plan G was the most popular Medigap policy, with 39% of all policyholders, or 5.3 million people. Plan G is the most comprehensive policy available to new policyholders, covering the Part A deductible and all cost-sharing for Part A and B services, but not the Part B deductible. The average monthly premium for Medigap Plan G in 2023 was $164, but this varied from $140 in D.C., Hawaii and New Mexico to $236 in New York.

In 2025, the average monthly cost of Medigap Plan G for a 65-year-old non-smoking woman was $159. Plan F, which was previously the most popular plan, is no longer available to new beneficiaries.

Understanding Emergency Medical Insurance Coverage

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps pay for costs that Original Medicare (Part A and Part B) do not cover.

Some popular Medicare Supplement Insurance plans include Plan F, Plan G, and Plan N. Plan F offers the most coverage but is only available to those who became eligible for Medicare before January 1, 2020. Plan G has the same coverage as Plan F but does not pay the Medicare Part B deductible. Plan N is the third most popular plan type and covers about 10% of all Medigap members.

When choosing a Medicare Supplement Insurance plan, consider your personal preferences, expected medical needs, and budget. Also, review the benefits offered by each plan, such as coverage for chronic conditions, foreign travel, or emergency services.

You can enroll in a Medicare Supplement Insurance plan during the Medigap open enrollment period, which is a six-month period starting the first month you have Medicare Part B and are 65 or older. You can use Medicare's plan finder tool or contact State Health Insurance Assistance Programs (SHIPs) to find the best plan for you.

Recommended companies for Medicare Supplement Insurance include AARP/UnitedHealthcare, Wellabe, Anthem, and Mutual of Omaha. These companies offer competitive rates, low complaint rates, and additional benefits such as wellness extras or discounts.