Supplemental medical insurance premiums are generally tax-deductible, but only as a qualified medical expense. In the United States, the Internal Revenue Service (IRS) outlines that medical premiums can be tax-deductible in certain situations, depending on a few factors. Firstly, you can only deduct premiums as medical expenses if you itemize deductions on your tax return, and not if you take the standard deduction. Secondly, tax deductibility depends on how you pay your premiums. If your insurance is through your employer, you can only deduct the out-of-pocket portion of your employer-sponsored health insurance premium if you take the itemized deduction. If you pay for health insurance coverage after taxes are taken out of your paycheck, you might qualify for the medical expense deduction.

Characteristics and Values

| Characteristics | Values |

|---|---|

| Tax exclusion for employer-sponsored health insurance | Lowers the after-tax cost of health insurance |

| Premiums paid by employers | Exempt from federal income and payroll taxes |

| Premiums paid by employees | Typically excluded from taxable income |

| Replacing ESI exclusion with a tax credit | Equalizes tax benefits across taxpayers in different tax brackets |

| Retired public safety officers | Cannot include premiums for long-term care insurance paid with tax-free distributions from a qualified retirement plan |

| Medical expenses | Include dental expenses, cost of meals at a hospital, transportation expenses, insurance premiums to cover medical care or qualified long-term care, and certain costs related to nutrition, wellness, and general health |

| Itemized deduction for medical and dental expenses | Can be claimed on Schedule A (Form 1040) only for expenses more than 7.5% of adjusted gross income (AGI) |

| Self-employed individuals with a net profit for the year | May be eligible for the self-employed health insurance deduction |

| Premium tax credit | Can be used to lower monthly insurance payments |

| Health insurance premiums | May be tax-deductible depending on how much was spent on medical care and how insurance was obtained |

Explore related products

What You'll Learn

![]()

Self-employed health insurance tax deductions

If you're self-employed, you may be able to deduct premiums that you pay for medical, dental, and qualifying long-term care insurance coverage for yourself, your spouse, and your dependents. This is known as the self-employed health insurance deduction. It is important to note that you can only claim this deduction for months when neither you nor your spouse were eligible to participate in an employer-subsidized health plan. For example, if you were single and ineligible for any employer-provided health plan during the last six months of the year, you can claim the deduction for those months.

To be eligible for the self-employed health insurance deduction, you must have a qualifying insurance plan and be an eligible self-employed individual. Eligible health insurance includes medical insurance, qualifying long-term care coverage, and all Medicare premiums (Parts A, B, C, and D). If you have a net profit for the year, you may be able to claim this deduction as an adjustment to income on your tax return. This means that you benefit whether or not you itemize your deductions, and it lowers your adjusted gross income (AGI).

If you are a business partner or LLC member treated as a partner for tax purposes, you can deduct the health insurance premiums you pay directly. If the partnership or LLC pays the premiums, you can still claim the deduction for premiums paid for your coverage by following special rules. On the other hand, if your self-employment activity is a sole proprietorship that generated a tax loss for the year, you cannot claim the deduction because the business did not generate any positive earned income.

It's important to note that the self-employed health insurance deduction is different from the itemized deduction for medical and dental expenses that you claim on Schedule A (Form 1040). The self-employed health insurance deduction is entered on Part II of Schedule 1 as an adjustment to income and transferred to page 1 of Form 1040. The itemized deduction for medical and dental expenses, on the other hand, only applies to expenses that exceed 7.5% of your adjusted gross income (AGI) for the year.

Medical Insurance: Understanding Average Costs and Bills

You may want to see also

Explore related products

![]()

Employer-paid insurance premiums

In the United States, employer-paid premiums for health insurance are exempt from federal income and payroll taxes. This exclusion also applies to accident insurance and qualified long-term care insurance. The portion of premiums that employees pay is typically excluded from taxable income, lowering most workers' tax bills and their after-tax cost of coverage. This tax subsidy is a significant factor in why most American families have health insurance coverage through their employers.

The amount an employer pays for health insurance depends on the number of employees in the company and the type of plan chosen. Small employers may cover a larger percentage of their employees' premiums than larger businesses. According to KFF's health benefits report, in 2023, employers covered 83% of their employees' self-only insurance plans and 73% of employees' family insurance plans on average. Small employers covered the entire self-only premium for 30% of covered workers, compared to only 6% of covered workers in large firms.

The annual cost of providing health insurance to employees depends on several key factors, including the health insurance company, the plan type, the network of providers in a plan, and plan features such as the annual deductible, copayment, and out-of-pocket maximum. The rising cost of health insurance, which has increased more than workers' wages or inflation over the last decade, can make it challenging for employers to continue offering competitive health benefits.

It is worth noting that if an employer increases an employee's compensation, the cash wages will be lower than the increase due to the additional employer payroll taxes. This results in a lower net increase in compensation for the employee. For example, if an employer increases compensation by $1,000, the cash wages only increase by $929 due to the employer payroll taxes.

Additionally, self-employed individuals may be eligible for the self-employed health insurance deduction, which allows them to adjust their income for premiums paid on health insurance policies covering themselves, their spouses, and dependents.

Disability Insurance and Medicaid: How Does Private Pay Affect Eligibility?

You may want to see also

Explore related products

![]()

Medical expense deductions

Medical and dental expenses are deductible from your taxes if they exceed 7.5% of your adjusted gross income (AGI). This includes unreimbursed payments for preventative care, treatment, surgeries, dental and vision care, visits to psychologists and psychiatrists, prescription medications, appliances such as glasses, contacts, false teeth and hearing aids, and expenses that you pay to travel for qualified medical care.

If you are self-employed and have a net profit for the year, you may be eligible for the self-employed health insurance deduction. This is an adjustment to income, rather than an itemized deduction, for premiums you paid on a health insurance policy covering medical care, including a qualified long-term care insurance policy for yourself, your spouse, and dependents.

If you are an eligible retired public safety officer, you cannot include premiums for long-term care insurance if you elected to pay these premiums with tax-free distributions from a qualified retirement plan made directly to the insurance provider. However, you can include in medical expenses the cost of meals at a hospital or similar institution if a principal reason for being there is to get medical care. You can also include in medical expenses amounts paid for admission and transportation to a medical conference if the medical conference concerns the chronic illness of yourself, your spouse, or your dependent.

If you didn't claim a medical or dental expense that would have been deductible in an earlier year, you can file Form 1040-X, Amended U.S. Individual Income Tax Return, to claim a refund for the year in which you overlooked the expense. Generally, a claim for refund must be filed within 3 years from the date the original return was filed or within 2 years from the time the tax was paid, whichever is later.

UCI Medical Center: Understanding Insurance Coverage and Options

You may want to see also

Explore related products

![]()

Tax credits

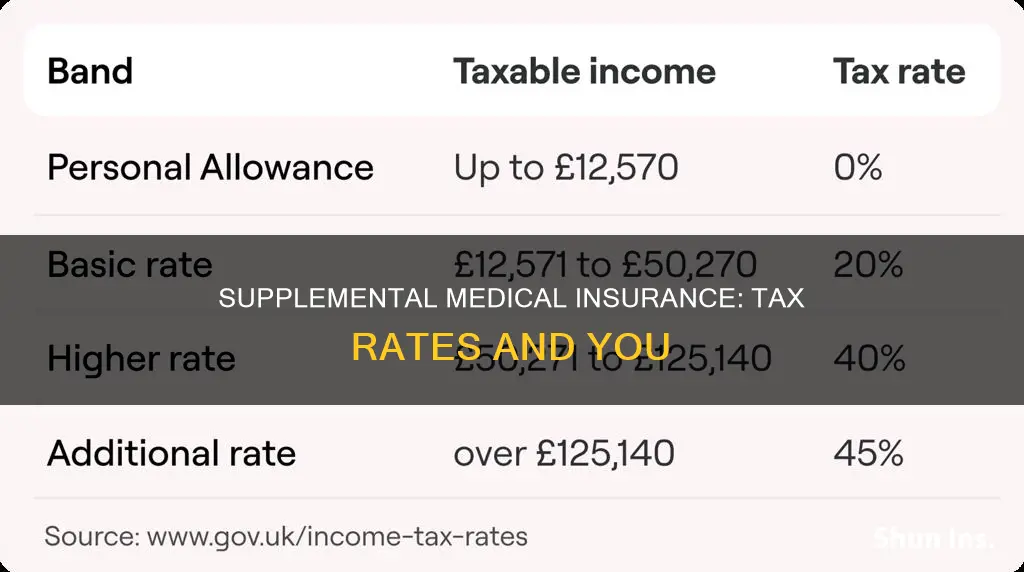

The tax rate on supplemental medical insurance is not a fixed rate. This is because the tax treatment of health insurance premiums depends on a few factors. Firstly, it depends on how you pay for your premiums. If your health insurance is provided by your employer, and your premiums are paid before taxes, then you cannot deduct your health insurance premiums. However, if you pay for health insurance coverage after taxes are taken out of your paycheck, you might qualify for the medical expense deduction.

Secondly, tax deductibility will depend on how much you spent on medical care for the year. If you are self-employed, you can deduct the cost of your health insurance premiums from your taxable income. If you are a W-2 employee, you can only deduct the out-of-pocket portion of your employer-sponsored health insurance premium if you take the

Supplemental health insurance premiums, like hospital indemnity insurance and critical illness insurance, are generally tax-deductible, but only as a qualified medical expense. You can deduct the cost if the total cost of your medical expenses and supplemental health insurance premiums exceeds 7.5% of your AGI and you take the itemized deduction.

You can use a premium tax credit to lower your monthly insurance payment. This may result in you owing taxes if you used more of the premium tax credit than you qualified for. You can also get a refund or lower the amount of tax you owe if you used less of the premium tax credit than you qualified for.

Replacing the exclusion for employer-sponsored health insurance with a tax credit would equalize tax benefits across taxpayers in different tax brackets. It would also equalize benefits between those who get their insurance through their employers and those who obtain coverage from other sources.

Workman's Comp: Medical Insurance or Separate Entity?

You may want to see also

Explore related products

![]()

Supplemental health insurance premiums

If you are self-employed and pay all your health insurance premiums, you can deduct the cost from your taxable income. This can be done as an 'above the line' deduction on Form 1040, without needing to itemize deductions on Schedule A. However, if you are a W-2 employee, the rules are stricter. You can only deduct the out-of-pocket portion of your employer-sponsored health insurance premium if you take the itemized deduction on your tax return.

If you obtain a health insurance policy through your employer, your medical insurance premiums are typically deducted from your paycheck. On the other hand, if you purchase a policy through the Health Insurance Marketplace, you must pay your first premium directly to the insurance company. In this case, the premium is deductible when it is an out-of-pocket cost.

Additionally, COBRA insurance premiums are eligible for a tax deduction as a medical expense since they are paid out-of-pocket without employer assistance. However, you can only deduct the cost if your total medical expenses, including COBRA premiums, exceed 7.5% of your AGI, and you take the itemized deduction. Similarly, short-term health insurance premiums are generally deductible as medical expenses if paid out-of-pocket using pre-tax dollars, and your total annual medical expenses exceed 7.5% of your AGI.

Understanding Auto Insurance: Medical Coverage Costs

You may want to see also

Frequently asked questions

There is no single tax rate for supplemental medical insurance. The tax rate depends on how much you spent on medical care for the year and whether you’re self-employed. If you are self-employed, you can deduct the cost from your taxable income. If you are not self-employed, you can only deduct the out-of-pocket portion of your employer-sponsored health insurance premium if you take the itemized deduction on your tax return.

If you are getting a healthcare plan from your employer, your medical insurance premiums are usually deducted from your paycheck. If you are getting health care coverage via the Health Insurance Marketplace, you must pay your first premium directly to the insurance company.

Medical expenses that are tax-deductible include the cost of meals at a hospital, transportation expenses, and premiums paid by you and your employer.

A premium tax credit is a tax credit that you can use to lower your monthly insurance payment.