Health insurance can be costly and challenging for people with low or moderate incomes to afford. The Affordable Care Act (ACA) offers sliding-scale subsidies that reduce premiums and insurers offer plans with lower out-of-pocket costs for eligible individuals. The Premium Tax Credit (PTC) is a refundable tax credit that helps eligible individuals and families cover the premiums for their health insurance purchased through the Health Insurance Marketplace. To be eligible for the PTC, your household income must be at least 100% and no more than 400% of the federal poverty line for your family size, though there are exceptions. The PTC is available immediately upon enrollment in an insurance plan, and individuals can choose to have payments go directly to insurers or wait until they file taxes to claim them. Additionally, Medicare Savings Programs are available in each state to help eligible individuals pay for Medicare Part A and Part B premiums, deductibles, coinsurance, and copayments.

Explore related products

What You'll Learn

![]()

Premium tax credits

The Affordable Care Act (ACA) provides sliding-scale subsidies that lower premiums and insurers offer plans with reduced out-of-pocket (OOP) costs for eligible individuals. The first type of financial assistance available to Marketplace enrollees is the premium tax credit, which reduces enrollees’ monthly payments for insurance coverage. The second type is the cost-sharing reduction (CSR), which reduces enrollees’ deductibles and other out-of-pocket costs when they go to the doctor or have a hospital stay.

To receive a premium tax credit, individuals must be U.S. citizens or lawfully present in the United States. They can’t receive a premium tax credit if they are eligible for other “minimum essential coverage,” which includes Medicare, Medicaid, or employer-sponsored coverage. The premium tax credit is available to individuals and families with incomes at or above the federal poverty level who purchase coverage in the ACA marketplace in their state.

For tax years 2021 and 2022, the American Rescue Plan of 2021 (ARPA) temporarily expanded eligibility for the premium tax credit by eliminating the rule that a taxpayer is not allowed a premium tax credit if their household income is above 400% of the Federal Poverty Line. For 2021, if you or your spouse received or were approved to receive unemployment compensation for any week, your household income is considered to be no greater than 133% of the federal poverty line for your family size, and you are considered to have met the household income requirements for a premium tax credit.

The premium tax credit is available immediately upon enrollment in an insurance plan, and people can choose to have payments go directly to insurers to pay a share of their monthly health insurance premiums charged or wait until they file taxes to claim them. The amount of the premium tax credit is based on a sliding scale, with generally greater credit amounts available to those with lower household incomes. To receive either type of financial assistance, qualifying individuals and families must enrol in a plan offered through a health insurance marketplace.

State Insurance vs. Medicaid: What's the Difference?

You may want to see also

Explore related products

![]()

Household income

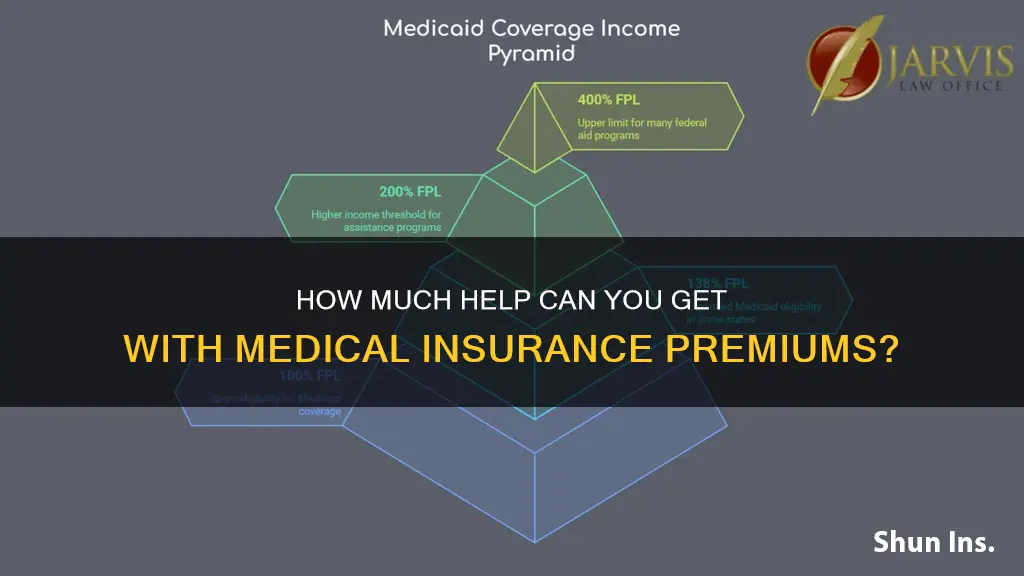

To be eligible for the premium tax credit, household income typically needs to fall within a certain range relative to the federal poverty line for the applicable family size. For most years, eligibility is determined by an individual's or family's income being at least 100% and no more than 400% of the federal poverty line. However, there are exceptions for certain individuals with household incomes below 100% of the poverty line, as outlined in Form 8962. The amount of the premium tax credit is generally higher for those with lower household incomes within this eligibility range.

In 2021 and 2022, the American Rescue Plan Act (ARPA) temporarily expanded eligibility by removing the upper income limit of 400% of the federal poverty line. This meant that individuals and families with incomes above this threshold could still qualify for the premium tax credit. Additionally, those who received unemployment compensation in 2021 were considered to meet the household income requirements if their income was no greater than 133% of the federal poverty line for their family size.

It's important to note that eligibility for the premium tax credit is not solely based on income. Other criteria, such as citizenship or legal residency status, access to employer-provided insurance, and enrollment in other government programs like Medicare or Medicaid, also come into play. Furthermore, income limits and eligibility criteria may vary slightly from state to state, with some states having higher income limits for certain programs.

The ACA's sliding-scale subsidies and cost-sharing reductions (CSR) also help make health insurance more affordable for individuals and families with lower or moderate incomes. These reductions lower deductibles and other out-of-pocket costs associated with medical care.

Medical Insurance Gaps: How Long is Too Long?

You may want to see also

Explore related products

![]()

Federal poverty guidelines

The poverty guidelines are one version of the federal poverty measure. They are issued annually in the Federal Register by the Department of Health and Human Services (HHS). The guidelines are a simplification of the poverty thresholds and are used for administrative purposes, such as determining financial eligibility for certain federal programs. The poverty guidelines are sometimes referred to as the "federal poverty level" (FPL), although this phrase is ambiguous and should be avoided in contexts where precision is important.

The HHS provides three sets of federal poverty guidelines: one for residents of the contiguous 48 states and Washington, D.C., one for Alaska residents, and one for Hawaii residents. The separate guidelines for Alaska and Hawaii reflect an administrative practice that began in the 1966-1970 period. The poverty guidelines are not defined for Puerto Rico, the U.S. Virgin Islands, American Samoa, Guam, the Republic of the Marshall Islands, the Federated States of Micronesia, the Commonwealth of the Northern Mariana Islands, and Palau.

The poverty guidelines are used to determine eligibility for various federal programs, including Head Start, the Supplemental Nutrition Assistance Program (SNAP), the National School Lunch Program, the Low-Income Home Energy Assistance Program, and the Children's Health Insurance Program. Certain programs, such as cash public assistance programs and the Earned Income Tax Credit program, do not use the poverty guidelines for eligibility determination.

The Affordable Care Act (ACA) provides financial assistance to eligible individuals purchasing health insurance through the Marketplace. This assistance comes in two forms: the premium tax credit and the cost-sharing reduction (CSR). The premium tax credit reduces monthly payments for insurance coverage, while the CSR lowers deductibles and other out-of-pocket costs. To receive financial assistance under the ACA, individuals must meet specific income requirements and other eligibility criteria. For 2021 and 2022, the American Rescue Plan of 2021 (ARPA) expanded eligibility by removing the rule that disqualifies individuals with household incomes above 400% of the Federal Poverty Line.

Travel Insurance: Medical Expense Claims and Their Validity

You may want to see also

Explore related products

![]()

Medicare Savings Programs

QMB, SLMB, and QI pay for a person's Medicare Part B premium, while QMB also covers additional cost-sharing in Parts A and B, and QDWI helps pay for a person's Part A premium. To qualify for QMB, an individual must have an income of less than 100% of the Federal Poverty Level (FPL) and resources under $9,660 if single and $14,470 if married.

MSPs are available to older adults and younger adults with disabilities who may not qualify for full Medicaid. Enrollment in MSPs provides significant financial benefits, including savings on Medicare costs and automatic qualification for the Medicare Part D Low-Income Subsidy (LIS/Extra Help) for prescription drug coverage.

It is important to note that income limits for MSPs are slightly higher in Alaska and Hawaii, and some states may have different names for these programs. Additionally, individuals should apply for MSPs through their respective states, as eligibility is determined by each state. Even if individuals do not meet the federal income limits, they are still encouraged to apply as they may qualify based on state-specific criteria.

Using Dual Medical Insurance Coverage to Your Advantage

You may want to see also

Explore related products

![]()

Eligibility criteria

Premium Tax Credit

The Premium Tax Credit is a component of the Affordable Care Act (ACA) that provides financial assistance to eligible individuals and families to help them pay for health insurance purchased through the Health Insurance Marketplace. To be eligible for the Premium Tax Credit, individuals must meet certain requirements, including:

- U.S. citizenship or lawful presence in the country: Lawfully present immigrants with incomes below 100% of the federal poverty line may be eligible if they meet other criteria. Deferred Action for Childhood Arrivals (DACA) recipients are also eligible.

- Income requirements: For 2021 and 2022, there was no maximum income limit. In other years, household income must be at least 100% and no more than 400% of the federal poverty line for your family size. The federal poverty guidelines vary for residents of different states.

- Enrollment in a health insurance plan: The credit is available for individuals and families who purchase coverage in the ACA marketplace in their state.

- Not having access to other minimum essential coverage: This includes employer-sponsored coverage, Medicare, or Medicaid.

- Filing a tax return: Individuals must file a tax return and meet other eligibility criteria as determined by the Marketplace.

Medicare Savings Programs

Medicare Savings Programs are state-run initiatives that help individuals with their Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) premiums, deductibles, coinsurance, and copayments. While specific eligibility criteria may vary by state, some general criteria include:

- Income limits: To qualify, individuals must have income and resources below certain limits. These limits vary by state and tend to be slightly higher in Alaska and Hawaii. Some states do not consider certain types or amounts of income or resources when determining eligibility.

- Enrollment in both Medicare Part A and Part B: In most cases, individuals must have both parts to qualify for assistance with Part B premiums.

It is important to note that eligibility criteria may change over time and can vary based on specific circumstances. Individuals seeking assistance with medical insurance premiums should refer to the official websites or relevant government organizations for the most up-to-date and accurate information regarding eligibility.

Medicaid and Insurance: Can Texans Have Both?

You may want to see also

Frequently asked questions

The threshold for assistance with medical insurance premiums depends on the state and the year. For example, for tax years 2021 and 2022, the American Rescue Plan of 2021 (ARPA) temporarily eliminated the rule that a taxpayer is not allowed a premium tax credit if their household income is above 400% of the federal poverty line.

There is no maximum income limit for the premium tax credit for the 2025 coverage year.

Lawfully residing immigrants with incomes below the poverty line who are not eligible for Medicaid due to their immigration status are eligible for the premium tax credit.