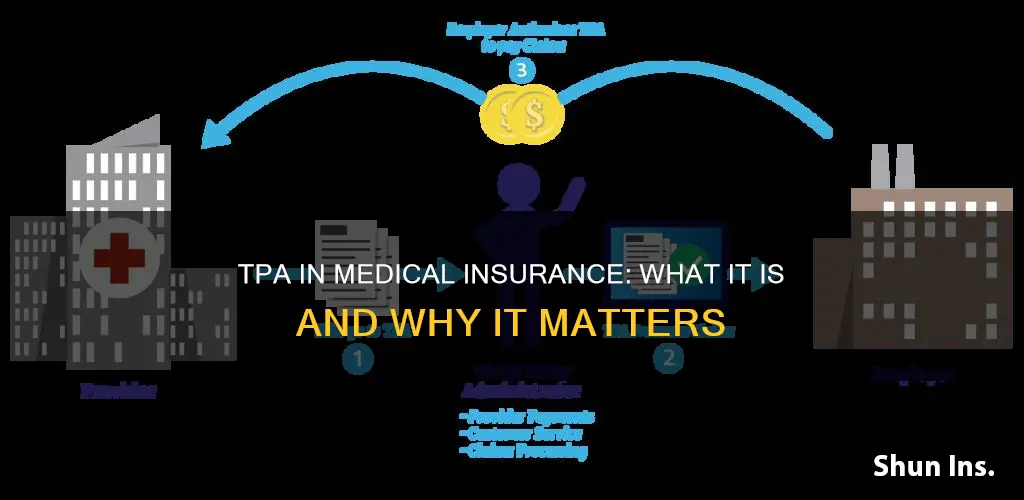

Third-party administrators (TPAs) are independent intermediaries that provide administrative services for self-funded health plans. They are often used by health insurance providers to outsource many of their administrative functions, such as claims administration, customer service, eligibility maintenance, and ID card production. TPAs may be independently owned and operated, owned by an insurance company, multi-employer group, or even by hospitals. They work on behalf of employers, offering a range of benefits, including cost savings and increased cash flow. They also have extensive knowledge of the healthcare industry and its regulatory requirements.

What is TPA in medical insurance?

| Characteristics | Values |

|---|---|

| Full Form | Third-Party Administrator |

| Function | Administrative services provider for self-funded health plans |

| Benefits | Cost savings, increased cash flow, access to reports, extensive knowledge and expertise in the healthcare industry, support for self-insured companies, more coverage and reimbursement options, managing administrative tasks and processes |

| Operations | Claims administration, premium billing, customer enrollment, eligibility maintenance, insurance claims processing, reporting, adjudicating claims, issuing payments, answering member phone calls, maintaining compliance with regulations |

| Structure | May be independently owned and operated, owned by an insurance company, multi-employer group, or hospitals |

| Relationship with Insurers | TPAs are not insurers and do not take on financial risk for claims; they work as connectors between businesses with self-funded plans and insurance providers |

| Specialization | Each TPA is unique in its culture, area of specialty, services offered, rates, and customer service level |

| Examples | Sedgwick Claims Mgt., UMR Inc., Crawford & Co., Planned Administrators Inc. (PAI) |

Explore related products

What You'll Learn

- Third-party administrators (TPAs) are independent of health insurance companies

- TPAs support self-insured companies and offer benefits to employers and brokers

- TPAs handle and process insurance claims

- TPAs may be owned by investment companies

- TPAs can help employers familiarise themselves with healthcare options

![]()

Third-party administrators (TPAs) are independent of health insurance companies

TPAs offer a range of benefits to employers and brokers, including cost savings and increased cash flow. They have extensive knowledge of the healthcare industry, regulatory requirements, and adjudicating claims. They can also help employers implement employee benefit plans and familiarise themselves with various healthcare options. TPAs handle and process insurance claims, manage eligibility and verification, adjudicate claims, and issue payments to healthcare providers or policyholders. They may also provide access to healthcare networks and source additional vendors such as stop-loss insurers.

The use of TPAs is becoming common in many businesses, and they are often used by health insurance providers who outsource their administrative functions. TPAs can provide a base level of service, including claims adjudication, customer service, eligibility maintenance, and ID card production. They can also offer additional services such as developing wellness programs, providing pharmacy benefits, and creating customised communication materials.

While TPAs offer flexibility in plan structure and healthcare network providers, it is important to note that they are not always open about pricing and have been known to hide administration fees. However, they can be a valuable partner for companies looking to self-insure their healthcare plans while reducing the administrative burden on HR and finance teams.

Overall, TPAs play a crucial role in supporting self-insured companies and providing administrative services for self-funded health plans, offering cost savings and expertise in the healthcare industry.

Medical Insurance: A College Student's Essential Companion?

You may want to see also

Explore related products

$39.12 $68.99

$40.27 $51.99

$17.75

![]()

TPAs support self-insured companies and offer benefits to employers and brokers

Third-party administrators (TPAs) are service providers that deliver support for self-insured health plans. They work on behalf of employers with the various outside vendors involved in the healthcare provider industry.

TPAs offer a wide variety of benefits for companies considering self-funded healthcare plans. They can help employers save costs and increase cash flow through planning, administering the plan, record-keeping, reporting, enrollment, and eligibility management. They can also provide access to reports on costs, claim history, and more, enabling informed decision-making and plan adjustments. TPAs have extensive knowledge and expertise in the healthcare industry, regulatory requirements, adjudicating claims, account management, and customer/member service needs.

By partnering with a TPA, companies can gain more coverage options as well as funding and reimbursement options. They can also help employers implement employee benefit plans and familiarize them with healthcare options they may not have considered. TPAs can also assist with claims adjudication, reviewing claims to decide whether they are reimbursable and processing eligible claims. They can further help with employee health plan onboarding by creating educational materials to ensure employees are informed about health plan benefits for easy enrollment.

TPAs also ensure state and federal compliance, using their depth of expertise to ensure health plans remain compliant with federal and state-mandated regulations. They can also facilitate making payments to service providers, streamlining the administrative process. They work with brokers and health insurance consultants, providing a broad understanding of how the pieces of the health insurance puzzle fit together.

TPAs are a good option for organizations looking to take advantage of the significant cost savings associated with self-insuring their healthcare plans. They can help self-insured companies without adding significantly to the administrative burden on human resources (HR) and finance teams.

Understanding Medical Insurance Coverage: Key Factors for Determination

You may want to see also

Explore related products

![]()

TPAs handle and process insurance claims

Third-party administrators (TPAs) are widely used in the insurance industry to manage and process insurance claims. They are administrative services providers that deliver support for self-insured health plans. They work as a connector between businesses with self-funded health plans and insurance providers.

TPAs can be independently owned and operated, owned by an insurance company, a multi-employer group, or even by hospitals. They work on behalf of employers with the broad variety of outside vendors involved in the healthcare provider industry. They may work directly with an employer or through agents and/or consultants.

TPAs handle all aspects of administration, including sales commissions, and are especially useful for insurers as they allow them to focus on their core business functions such as underwriting and marketing while leaving administrative work in expert hands. They can also help with cost savings, increased cash flow, planning, record-keeping, reporting, enrollment, eligibility management, and more.

When a policyholder files a claim, it is forwarded to the assigned TPA for review. The TPA assesses the validity of the claim, communicates with relevant parties such as healthcare providers or contractors, and makes payments based on their findings. They handle any disputes that may arise during this process. TPAs also have access to advanced technology that enhances their ability to process large amounts of data efficiently, leading to faster turnaround times for policyholders' claims.

While TPAs offer many benefits, there are some potential disadvantages to consider. For example, outsourcing claim management might be more expensive than handling it in-house due to additional costs associated with hiring a TPA. Additionally, some TPAs have been charged with hiding administration fees and using questionable tactics to collect alleged overpayments.

Blue Cross Blue Shield: Understanding Horizon's Medicaid Offerings

You may want to see also

Explore related products

![]()

TPAs may be owned by investment companies

A TPA, or Third Party Administrator, is an organisation or individual that acts as an independent intermediary, providing administrative services for self-funded health plans. They work on behalf of employers, handling the intricacies of health plans, which many employers do not have the resources to manage themselves.

TPAs can be independently owned and operated, or owned by an insurance company, a multi-employer group, or even a hospital. They offer a variety of benefits, including cost savings, increased cash flow, and extensive knowledge of the healthcare industry and regulatory requirements. They can also help employers implement employee benefit plans and familiarise themselves with healthcare options.

While TPAs are not the insurer and do not take on the financial risk for a company's health benefit claims, they do handle and process all insurance claims, manage eligibility and verification, adjudicate claims, and issue payments to healthcare providers or policyholders. They also evaluate the medical necessity and appropriateness of healthcare services or treatments to ensure they meet established guidelines.

In summary, TPAs provide valuable support for self-insured companies and can be owned by investment companies, insurance companies, or operate independently. They offer a range of benefits and play a crucial role in managing administrative tasks and processes for employers.

Submitting Medical Bills to Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

TPAs can help employers familiarise themselves with healthcare options

A Third-Party Administrator (TPA) in the health insurance industry is an administrative services provider that delivers support for self-insured health plans. They work on behalf of employers with the variety of outside vendors involved in the health care provider industry. Some TPAs work directly with an employer, while others work through agents and/or consultants.

TPAs have extensive knowledge and expertise in the healthcare industry, regulatory requirements, adjudicating claims, account management, and customer/member service needs. They can help employers familiarise themselves with healthcare options in several ways. Firstly, they can help employers implement employee benefit plans and introduce them to healthcare options they may not have considered. Secondly, they can provide access to healthcare networks and source additional vendors, such as stop-loss insurers, which help limit high claims risks for employers. Thirdly, TPAs can negotiate rates with healthcare providers and vendors to ensure their clients receive the best possible prices for medical services and supplies. By pooling resources, they can often offer better rates and discounts than an employer could negotiate on their own. Fourthly, they can provide valuable insights into a plan's utilisation, spending, and the overall health status of an employee base, allowing employers to make informed adjustments. Lastly, they can handle the entire enrollment process, including paperwork and mailing ID cards, and provide ongoing support as employees join and leave the business, thus reducing the administrative burden on the employer.

Understanding Medical Insurance: What is AV?

You may want to see also

Frequently asked questions

TPA stands for Third Party Administrator.

A Third Party Administrator provides administrative services for self-funded health plans, sometimes referred to as self-insured health plans. They handle and process insurance claims, manage eligibility and verification, and issue payments to healthcare providers or policyholders.

Third Party Administrators offer cost savings and increased cash flow for clients. They can also help employers implement employee benefit plans and familiarise themselves with healthcare options.