Universal life insurance (UL) is a form of permanent life insurance with an investment savings element. Unlike term life insurance, UL insurance policyholders can adjust their premiums and death benefits, and the policy can accumulate cash value. The cash value earns an interest rate set by the insurer, which can change frequently, although there is usually a minimum rate that the policy can earn.

| Characteristics | Values |

|---|---|

| Type | Permanent life insurance |

| Flexibility | Flexible benefits, premiums and death benefits |

| Investment savings | Yes, UL insurance can accumulate cash value |

| Tax implications | No tax implications for policyholders who borrow against the accumulated cash value of their UL policy, although some withdrawals may be taxed |

Explore related products

What You'll Learn

![]()

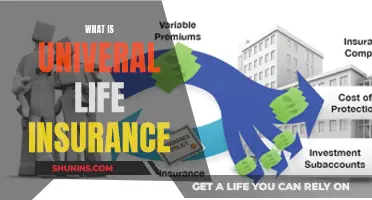

UL insurance is a form of permanent life insurance

Universal life (UL) insurance is a form of permanent life insurance with an investment savings element. Unlike term life insurance, UL insurance policies can accumulate cash value. This cash value earns an interest rate set by the insurer, which can change frequently, although there is usually a minimum rate that the policy can earn. The interest rate is often set at a minimum of 2%.

UL insurance provides more flexibility than whole life insurance. Policyholders can adjust their premiums and death benefits. UL insurance premiums consist of two components: a cost of insurance (COI) amount and a saving component, known as the cash value. The excess of premium payments above the current cost of insurance is credited to the cash value of the policy, which is credited each month with interest. The policy is debited each month by a COI charge as well as any other policy charges and fees drawn from the cash value, even if no premium payment is made that month.

There are no tax implications for policyholders who borrow against the accumulated cash value of their UL policy, although some withdrawals may be taxed. If the investments underperform, the cash value can go down and premiums could eventually go up.

Terminal Diagnosis: Life Insurance Options and Availability

You may want to see also

Explore related products

![]()

UL insurance has an investment savings element

Universal life (UL) insurance is a form of permanent life insurance with an investment savings element. Unlike term life insurance, UL insurance policies can accumulate cash value. This cash value earns an interest rate set by the insurer, which can change frequently, although there is usually a minimum rate that the policy can earn. The interest rate is often set at a minimum of 2%.

The cash value of a UL insurance policy is credited each month with interest. The policy is also debited each month by a cost of insurance (COI) charge, as well as any other policy charges and fees, which are drawn from the cash value. Even if no premium payment is made in a particular month, these charges are still taken from the cash value.

The excess of premium payments above the current cost of insurance is credited to the cash value of the policy. This means that if the investments underperform, the cash value can go down and premiums could eventually increase. However, there are no tax implications for policyholders who borrow against the accumulated cash value of their UL policy, although some withdrawals may be taxed.

UL insurance provides more flexibility than whole life insurance, as policyholders can adjust their premiums and death benefits. UL insurance premiums consist of two components: a cost of insurance (COI) amount and a savings component, known as the cash value. This flexibility is a key feature of UL insurance, allowing policyholders to customise their coverage to meet their specific needs and budget.

Life and Health Insurance: Producers' License Requirements

You may want to see also

Explore related products

![]()

UL insurance premiums are flexible

Universal life (UL) insurance is a form of permanent life insurance with an investment savings element, flexible premiums and a death benefit. Unlike term life insurance, a UL insurance policy can accumulate cash value. The cash value earns an interest rate set by the insurer, and it can change frequently, although there is usually a minimum rate that the policy can earn.

The interest credited to the account is determined by the insurer but has a contractual minimum rate (often 2%). If the investments underperform, your cash value can go down and your premiums could eventually go up. There are no tax implications for policyholders who borrow against the accumulated cash value of their UL policy, although some withdrawals may be taxed.

Who Can Be Your Life Insurance Beneficiary?

You may want to see also

Explore related products

![]()

UL insurance accumulates cash value

Universal life (UL) insurance is a form of permanent life insurance with an investment savings element. It is one of the two main types of permanent life insurance, the other being whole life insurance. UL insurance provides more flexibility than whole life insurance, allowing policyholders to adjust their premiums and death benefits. UL insurance premiums consist of two components: a cost of insurance (COI) amount and a saving component, known as the cash value. This cash value can accumulate over time, earning interest at a rate set by the insurer. The interest rate can change frequently, but there is usually a minimum rate that the policy can earn, often around 2%.

The excess of premium payments above the current cost of insurance is credited to the cash value of the policy each month, along with the interest. At the same time, the policy is debited each month by the COI charge and any other policy charges and fees, even if no premium payment is made that month. The cash value of UL insurance can be a useful feature, as it allows policyholders to borrow against it without tax implications. However, it is important to note that if the investments underperform, the cash value can decrease, and premiums may eventually increase.

Overall, UL insurance provides a flexible option for those seeking permanent life insurance, with the added benefit of accumulating cash value that can be borrowed against. The interest-earning potential of the cash value component can help offset the costs of insurance and provide a source of funds for policyholders.

Bedridden and Seeking Life Insurance: What Are Your Options?

You may want to see also

Explore related products

![]()

UL insurance is sold primarily in the United States

Universal life (UL) insurance is a form of permanent life insurance with an investment savings element and flexible premiums and death benefits. Unlike term life insurance, a UL insurance policy can accumulate cash value. The cash value earns an interest rate set by the insurer, and it can change frequently, although there is usually a minimum rate that the policy can earn. UL insurance is sold primarily in the United States.

UL insurance is one of the two main types of permanent life insurance, the other being whole life insurance. UL insurance provides more flexibility than whole life insurance. Policyholders can adjust their premiums and death benefits. UL insurance premiums consist of two components: a cost of insurance (COI) amount and a saving component, known as the cash value. The excess of premium payments above the current cost of insurance is credited to the cash value of the policy, which is credited each month with interest. The policy is debited each month by a COI charge as well as any other policy charges and fees drawn from the cash value, even if no premium payment is made that month.

The interest credited to the account is determined by the insurer but has a contractual minimum rate (often 2%). If the investments underperform, your cash value can go down and your premiums could eventually go up. There are no tax implications for policyholders who borrow against the accumulated cash value of their UL policy, although some withdrawals may be taxed.

Trusts and Life Insurance: Who Gets the Payout?

You may want to see also

Frequently asked questions

UL stands for Universal Life Insurance. It is a form of permanent life insurance with an investment savings element and flexible premiums and death benefits.

Unlike term life insurance, UL insurance can accumulate cash value. This cash value earns an interest rate set by the insurer, which can change frequently but there is usually a minimum rate.

UL insurance provides more flexibility than whole life insurance. Policyholders can adjust their premiums and death benefits.

UL insurance premiums consist of two components: a cost of insurance (COI) amount and a saving component, known as the cash value. The excess of premium payments above the current cost of insurance is credited to the cash value of the policy, which is credited each month with interest.