Medicare is a health insurance program for individuals aged 65 and above, provided by the federal government. It is also available for individuals under 65 who qualify for premium-free Part A based on disability or End-Stage Renal Disease (ESRD). Individuals can also sign up for Medicare Part A and B if they are still working and have health insurance through their job or their spouse's job. Medicare Supplement Insurance (Medigap) is extra insurance that can be purchased from a private company to help pay for costs not covered by Original Medicare. This includes costs such as vision, dental, hearing aids, and prescription drugs. It is important to understand the different parts of Medicare and the enrollment periods to ensure that you get the coverage you need without incurring late enrollment penalties.

| Characteristics | Values |

|---|---|

| Medicare Part A | Hospital Insurance |

| Medicare Part B | Medical Insurance |

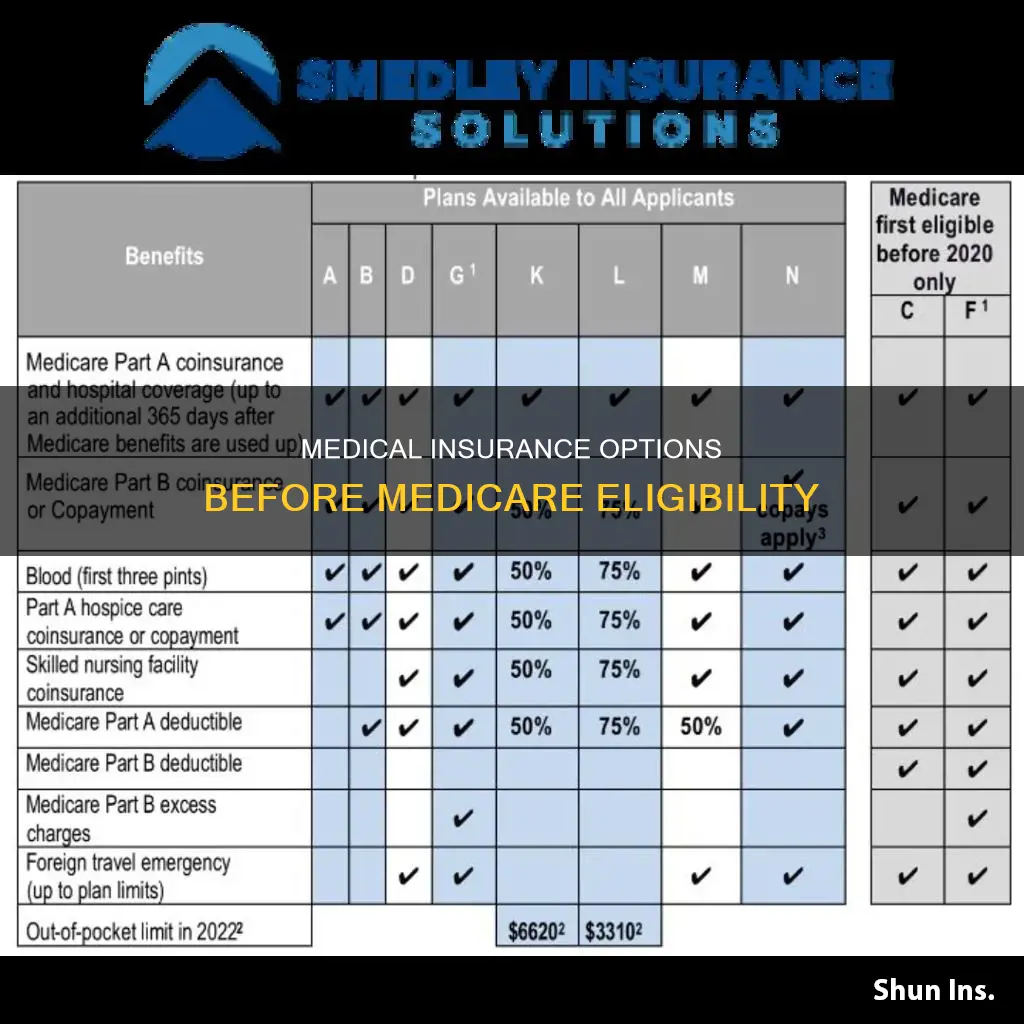

| Medicare Supplement Insurance | Extra insurance to help pay your share of costs in Original Medicare |

| Medicare Advantage | Available after signing up for Part A and Part B |

| Eligibility | Generally, individuals are eligible to sign up for Part A and Part B starting 3 months before turning 65 and ending 3 months after turning 65 |

| Enrollment Period | There is a Special Enrollment Period of 8 months to sign up for Part B after losing job-based health coverage |

| Penalties | There is a monthly penalty for late enrollment in Part B, which increases the longer one waits to sign up |

| Costs | Most people don't pay a premium for Part A, but there is a monthly premium for Part B |

Explore related products

What You'll Learn

![]()

Job insurance

Medicare is the federal health insurance program for people aged 65 and over in the US. If you are under 65, you may be eligible for Medicare earlier if you have a disability, End-Stage Renal Disease (ESRD), or ALS (Lou Gehrig's Disease).

If you are employed and seeking insurance before you turn 65, you may be offered job-based health insurance. A survey by the Commonwealth Fund found that 96% of Americans believe it is important that a job offer health insurance, and 93% of respondents with job insurance were satisfied with their insurance. However, the same survey found that 52% of respondents did not strongly agree that insurance was affordable, and more than 70% did not say it was comprehensive or convenient.

Employer-sponsored insurance (ESI) is the primary source of health insurance coverage in the United States, covering about 178 million people in 2023. However, the costs of ESI, including premium contributions, deductibles, and co-payments, can pose a significant financial burden on employees, especially those with low and moderate incomes. The average insurance deductible for employer health plans with single coverage was $1,434 for all covered workers in 2021, and out-of-pocket maximums averaged $4,272 for single coverage.

If you have a Marketplace insurance plan and are then offered job-based insurance, you may no longer qualify for savings on your Marketplace plan, even if you do not accept the job-based coverage. However, you can choose to cancel your Marketplace plan and enrol in the job-based insurance plan.

If you have job-based insurance and are considering enrolling in Medicare, you should be aware that you will need to end your contributions to your Health Savings Account (HSA) at least six months before enrolling in Medicare Part A or Part B.

Pennsylvania Medical Marijuana Insurance Coverage: What's the Deal?

You may want to see also

Explore related products

![]()

Spouse's job insurance

If you are covered by your spouse's employer health insurance plan, you may not need to sign up for Medicare at 65. This depends on the size of the employer. If your spouse works for a large employer (20 or more employees), you do not need to sign up for Medicare at 65. The company-sponsored health insurance will continue to be the primary payer, and Medicare will be the secondary payer. Employers with 20 or more employees must offer the same health benefits to all employees and their spouses, regardless of age, and they cannot require enrolment in Medicare at 65.

However, if your spouse works for an employer with fewer than 20 employees, Medicare typically becomes the primary coverage at 65, and you will need to enrol to avoid gaps in coverage. You can enrol in Medicare Parts A & B, Part D prescription drug coverage, or a Medicare Advantage (Part C) plan. You can also look at adding a Medicare supplement insurance plan to Original Medicare (Parts A & B) to help with out-of-pocket costs.

If you are covered by your spouse's employer plan and eligible for Medicare, you may choose to delay enrolling until you lose your spouse's employer coverage or only enrol in Part A, as it usually has no premium. You can delay Part B and Part D, but you'll need creditable coverage to avoid paying late premium penalties. Before making any decisions, it is recommended to talk with the employer's health care benefits department to understand how Medicare will work with your current coverage.

If your spouse is older and enrols in Medicare instead of keeping their employer's insurance, you may lose your private health insurance coverage. In this case, you may need to find other sources of coverage before turning 65 and becoming eligible for Medicare. One option is to continue the employer's coverage through COBRA, which can last up to 36 months. Alternatively, you can buy a private plan through the Affordable Care Act federal insurance marketplace or a state exchange.

Medical Insurance in Mexico: What's Covered?

You may want to see also

Explore related products

![]()

Family member's job insurance

If you are eligible for Medicare due to age (meaning you are 65 or older) or disability, and are covered by your spouse's or family member's job-based insurance, you have a Special Enrollment Period (SEP) to enroll in Medicare Part B. This period lasts for eight months after your job-based insurance coverage ends. To qualify for the Part B SEP, you must be currently working. You are considered to be currently working as long as you have employment rights at your company, even if you are on sick leave, are a seasonal worker, or have been temporarily laid off.

Job-based insurance is primary if it is from an employer with 20 or more employees, in which case Medicare is secondary. If your job-based insurance is primary, you may choose to delay enrolling in Medicare Part B, as it is not required during your Initial Enrollment Period (IEP). However, if your job-based insurance is secondary, delaying Medicare enrollment may result in high costs for your care.

If you plan to delay enrolling in Part B and use the SEP later, keep records of your health insurance coverage. You will need to submit proof of your enrollment in job-based insurance when using the SEP to enroll in Part B. This includes documents that show health insurance premiums paid, such as W-2s, pay stubs, tax returns, and/or receipts, as well as health insurance cards with the appropriate effective date.

If you have a child with a disability, they may be covered by your job-based insurance. The employing office may approve coverage due to disability for a limited period of time (e.g., one year) or without time limitation. If approved for a limited period, the enrollee must be reminded to submit a new certificate or a statement that they will not submit a new certificate at least 60 days before the expiration date. If the enrollee does not renew a medical certificate for a disabled child age 26 or over, the child's status as a family member automatically ends, and they are no longer covered.

Travel Insurance and COVID-19: What Medical Expenses Are Covered?

You may want to see also

Explore related products

$69.32 $105.95

![]()

Veterans Affairs insurance

If you are a US veteran, you may be eligible for health care coverage through the Department of Veterans Affairs (VA). The VA provides a range of health benefits and services to veterans, including medical care, routine eye exams, preventive tests, and coverage for most care services. Each veteran's medical benefits package is unique and depends on various factors, including their primary care provider's advice.

Veterans who are not enrolled in VA benefits or other veterans' health coverage can obtain insurance through the Health Insurance Marketplace®. Depending on household size and income, veterans may be eligible for reduced monthly premiums and out-of-pocket costs on private insurance plans. Additionally, they may qualify for free or low-cost coverage through Medicaid or the Children's Health Insurance Program (CHIP).

VA health care can be used alongside other forms of health care coverage, such as private insurance plans, Medicare, Medicaid, or TRICARE. However, the VA will bill private health insurance providers for treating non-service-connected conditions. The VA also encourages veterans to sign up for Medicare as funding for VA health care may change in the future, and Medicare provides more options for choosing hospitals and doctors.

It is important to note that VA health care benefits are subject to funding availability, and veterans in lower priority groups may lose their benefits in the future. Therefore, it is recommended to maintain private insurance or Medicare coverage in addition to VA benefits to ensure continuous health coverage.

Veterans can also access long-term care services through the VA, including assisted living, residential, or home health care. Additionally, the VA provides transportation services to help veterans get to and from their medical appointments. Overall, the VA health care system aims to provide comprehensive coverage and support to veterans, ensuring they receive the necessary care to maintain their health and well-being.

North Cypress Medical Center: Insurance and You

You may want to see also

Explore related products

![]()

Medicaid

To be eligible for Medicaid, individuals must typically meet requirements related to age, disability, income, and other factors. In Mississippi, for example, individuals must be citizens of the United States or qualified aliens to qualify for basic Medicaid benefits. The Affordable Care Act (ACA) has also created insurance affordability programs, allowing individuals and families with incomes above the poverty level but below 400% of the federal poverty level to purchase insurance at a lower cost.

It is important to note that Medicaid is sometimes confused with Medicare, which is a federally administered and funded health insurance program primarily for individuals over 65 and some people with disabilities. However, there is overlap between the two programs, with some low-income seniors and people with disabilities enrolled in both.

Sanford Medical: Is Medica Insurance Accepted at Their Facilities?

You may want to see also

Frequently asked questions

Medicare Part A is hospital insurance. Most people don't pay a premium for Part A, so you may want to sign up when you turn 65.

Medicare Part B is medical insurance. You pay a monthly premium for Part B, so you may want to delay signing up until you need it.

Medicare Supplement Insurance, or Medigap, is extra insurance you can buy from a private company to help pay your share of costs in Original Medicare. Generally, you need Part A and Part B to buy a Medigap policy.