The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that provides deposit insurance to protect bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. The FDIC was created by the Banking Act of 1933, enacted during the Great Depression to restore trust in the American banking system. The FDIC receives no funding from the federal budget and assesses premiums on each member, accumulating them in a Deposit Insurance Fund (DIF) that it uses to pay operating costs and depositors of failed banks. The FDIC insures deposits in member banks up to $250,000 per depositor, per FDIC-insured bank, and per ownership category.

| Characteristics | Values |

|---|---|

| Name | Federal Deposit Insurance Corporation (FDIC) |

| Type of Organization | An independent agency of the United States government |

| Purpose | To maintain stability and public confidence in the nation's financial system |

| Function | Provides deposit insurance to protect bank depositors in the event of a bank failure |

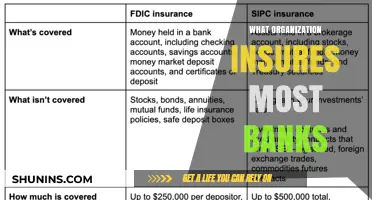

| Coverage | Deposits are insured up to $250,000 per depositor, per FDIC-insured bank, per ownership category |

| Funding | The FDIC receives funding from premiums assessed on each member bank, which are accumulated in a Deposit Insurance Fund (DIF) |

| Tools | Electronic Deposit Insurance Estimator (EDIE), an online tool to help depositors determine their insurance coverage |

| Resources | Information and guidance on regulations, examinations, and legislation for bankers and consumers |

| Contact | 1-877-275-3342 (1-877-ASK-FDIC) |

Explore related products

What You'll Learn

![]()

The Federal Deposit Insurance Corporation (FDIC)

The FDIC receives no funding from the federal budget. Instead, it assesses premiums on each member and accumulates them in a Deposit Insurance Fund (DIF) that it uses to pay its operating costs and the depositors of failed banks. The amount of each bank's premiums is based on its balance of insured deposits and the degree of risk that it poses to the FDIC. The DIF is fully invested in Treasury securities, and the interest earned supplements the premiums. Under the Dodd–Frank Act of 2010, the FDIC is required to fund the DIF to at least 1.35% of all insured deposits. During banking crises, the FDIC has expended its entire insurance fund and met insurance obligations directly from operating cash or by borrowing through the Federal Financing Bank.

The FDIC has the power to merge a failed institution with another insured depository institution and transfer its assets and liabilities without the consent or approval of any other agency, court, or party with contractual rights. It may also form a new institution, such as a bridge bank, to take over the assets and liabilities of the failed institution, or it may sell or pledge the assets of the failed institution. The two most common ways for the FDIC to resolve a closed institution and fulfil its role as a receiver are through a purchase and assumption agreement (P&A) or by establishing a temporary deposit insurance national bank that assumes the failed bank's deposits.

The FDIC provides extensive resources for bankers, including guidance on regulations, information on examinations, legislation insights, and training programs. It also offers information and forms for Call Reports and the Summary of Deposits survey. FDIC-insured institutions are permitted to display a sign stating the terms of its insurance, including the per-depositor limit and the guarantee of the United States government. The FDIC management consists of a five-member Board of Directors, including a Chairman, Vice Chairman, Appointive Director, Comptroller of the Currency, and Director of the Bureau of Consumer Financial Protection.

Private Housekeeper Insurance: What You Need to Know

You may want to see also

Explore related products

![Federal Deposit Insurance Act: [As Amended Through P.L. 117–263, Enacted December 23, 2022]](https://m.media-amazon.com/images/I/517mroyL3UL._AC_UY218_.jpg)

$5.99 $19.99

![]()

Deposit Insurance Fund (DIF)

The Deposit Insurance Fund (DIF) is managed by the Federal Deposit Insurance Corporation (FDIC) to ensure that deposits at member banks are protected. The FDIC is a United States government corporation that provides deposit insurance to depositors in American commercial banks and savings banks. The money in the DIF is set aside to reimburse customers for money lost due to the failure of a financial institution. The fund is sourced from insurance payments made by banks in the form of premiums based on their balance of insured deposits and the degree of risk they pose to the FDIC. The FDIC also earns interest on the fund's investments, which supplements the premiums.

The FDIC was created by the Banking Act of 1933, enacted during the Great Depression to restore trust in the American banking system. More than one-third of banks failed in the years before the FDIC's creation, and bank runs were common. The insurance limit was initially US$2,500 per ownership category, and this has been increased several times over the years. Since its inception, the FDIC has charged assessments and maintained a deposit insurance fund, and these systems have evolved based on data and experience from two banking crises.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 modified the FDIC's fund management practices by setting requirements for the Designated Reserve Ratio (DRR) and redefining the assessment base used to calculate banks' quarterly assessments. The DRR ratio is the DIF balance divided by estimated insured deposits. In response to these revisions, the FDIC developed a long-term plan to manage the DIF, aiming to reduce pro-cyclicality and achieve moderate and steady assessment rates. As part of this plan, the FDIC Board adopted the existing assessment rate schedules and a 2% DRR.

The FDIC provides deposit insurance to protect customers' money in the event of a bank failure. Deposits are automatically insured for up to $250,000 per ownership category at each FDIC-insured bank. The FDIC only insures money held in deposit accounts, and some financial products and services offered by banks are not covered. The FDIC has the power to merge a failed institution with another insured depository institution and transfer its assets and liabilities without seeking approval from any other agency or court.

Understanding Magnacare: Private Insurance Options and Benefits

You may want to see also

Explore related products

$37.99

![]()

Deposit Insurance Estimator (EDIE)

In the United States, the Federal Deposit Insurance Corporation (FDIC) is a government corporation that provides deposit insurance. The FDIC was created by the Banking Act of 1933 to restore trust in the American banking system after the Great Depression, during which more than one-third of banks failed. FDIC deposit insurance protects money held in traditional deposit accounts at FDIC-insured banks. Coverage is automatic for these types of accounts.

The FDIC provides an Electronic Deposit Insurance Estimator (EDIE) to help consumers and bankers understand how insurance rules and limits apply to a depositor's specific group of deposit accounts. EDIE calculates the insurance coverage for various types of accounts, including:

- Personal Accounts: deposits held by people in single accounts, joint accounts, payable on death (POD)/in trust for (ITF) accounts, living trust accounts, and Individual Retirement Accounts (IRAs).

- Business Accounts: deposits held by corporations, partnerships, and organizations, both for-profit and not-for-profit.

- Government Accounts: deposits held by public units such as school districts, cities, municipalities, counties, and states.

EDIE can be used to calculate the insurance coverage of all types of deposit accounts offered by an FDIC-insured bank. It is designed to give an accurate deposit insurance calculation, assuming the account information is correctly entered. However, the results and conclusions generated by EDIE are strictly advisory, and actual claims are governed by the information in the FDIC-insured institution's records and applicable federal statutes and regulations.

As of April 1, 2024, the maximum insurance coverage for a trust owner with five or more beneficiaries is $1,250,000 per owner for all trust accounts held at the same bank. This coverage change applies to both existing and new trust accounts, for all deposit products, including Certificates of Deposit (CDs) regardless of purchase or maturity date.

How Much of Your Bank Funds Are Insured?

You may want to see also

Explore related products

![]()

BankFind tool

In the United States, the Federal Deposit Insurance Corporation (FDIC) insures deposits in member banks. The FDIC is a government corporation that was established by the Banking Act of 1933 to restore trust in the American banking system after the Great Depression, during which many banks failed. The FDIC currently insures deposits of up to $250,000 per ownership category in member banks.

The FDIC offers a free database called BankFind, which provides general information about FDIC-insured financial institutions. Both consumers and employees can use this tool to make informed decisions. BankFind offers a concise overview of a financial institution, including details such as whether the institution is well-run and trustworthy. This can be particularly useful for consumers who want to ensure that their money is deposited with sound financial institutions.

Banking professionals also utilise BankFind for various purposes. For instance, bankers can refer to BankFind when researching another bank or credit union before entering into a loan participation agreement. They can quickly access information about potential partner institutions to determine if they are comfortable proceeding with a deal. Additionally, financial institutions can use BankFind to identify peer institutions and perform peer comparisons to assess their performance relative to their competitors.

The FDIC's BankFind tool simplifies the process of gathering relevant information about financial institutions. It serves as a valuable resource for both consumers and banking professionals, enabling them to make informed decisions and assess the financial landscape effectively.

Who Hires Private Fire Fighters and Why?

You may want to see also

Explore related products

![]()

Dodd-Frank Act of 2010

The Dodd-Frank Wall Street Reform and Consumer Protection Act, also known as Dodd-Frank Act, was enacted in 2010 as a response to the financial crisis of 2007–2008 and the government bailouts that followed. It was the most far-reaching Wall Street reform in history, aiming to prevent a repeat of the financial crisis and end government bailouts.

The Act brought comprehensive reform to the regulation of swaps, which had been at the centre of the 2008 financial crisis. Swap dealers were now subject to capital and margin requirements, and had to meet robust business conduct standards and record-keeping requirements. Standardized derivatives were required to be traded on regulated exchanges or swap execution facilities, increasing transparency and competition in the marketplace.

The Act also established the Financial Stability Oversight Council and the Orderly Liquidation Authority, which monitor the financial stability of major financial firms. The council has the authority to break up banks that are considered too large and pose a systemic risk. The law also provides for liquidations or restructurings via the Orderly Liquidation Fund, which was established to assist with the dismantling of financial companies without using taxpayer money.

Additionally, the Dodd-Frank Act included protections for consumers, such as the Credit CARD Act, which prohibits unfair practices like raising rates on existing balances and imposes transparency requirements on credit card companies. The law also created a new consumer watchdog to prevent mortgage companies and payday lenders from exploiting consumers.

The Volcker Rule, included in the Act, restricts how banks can invest, limits speculative trading, and eliminates proprietary trading. It also prohibits banks from involvement with hedge funds or private equity firms, which are considered too risky.

While the Dodd-Frank Act was intended to target large financial institutions, some researchers argue that it has hurt smaller banks and that regulatory barriers have fallen most heavily on them. However, others dispute this claim, noting that community bank failures have decreased since the Act was passed.

Deposit Insurance: Preventing Bank Panic and Protecting Your Money

You may want to see also

Frequently asked questions

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that insures bank deposits.

The FDIC insures deposits of up to up to $250,000 per depositor, per FDIC-insured bank, per ownership category.

The FDIC does not receive federal funding. Instead, it assesses premiums on each member institution, which are accumulated in a Deposit Insurance Fund (DIF) used to cover operating costs and depositor payouts.

You can ask a bank representative, look for the FDIC sign at your bank, or use the FDIC's BankFind tool, which provides detailed information on all FDIC-insured institutions.

The FDIC steps in to ensure that insured depositors have access to their accounts. This may involve negotiating a purchase and assumption transaction, where a healthy institution acquires the failed bank's assets and deposits, or liquidating the institution and issuing checks to insured depositors.