Medicare supplement insurance, also known as Medigap, is a type of private health insurance that helps to cover the costs associated with Medicare. Medigap policies can help cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance. In 2022, Medigap covered 21% of Medicare beneficiaries overall, or 42% of those in traditional Medicare (12.5 million beneficiaries). The percentage of Medicare patients with supplemental insurance has been declining, with the number of traditional Medicare beneficiaries without supplemental coverage decreasing from 10% in 2018 to 5% in 2022. This decline is likely due to the increase in Medicare Advantage enrollment, which offers additional benefits such as dental, vision, hearing, and fitness enhancements.

| Characteristics | Values |

|---|---|

| Medicare beneficiaries with supplemental insurance | 90% (2019) |

| Medicare beneficiaries without supplemental insurance | 10% (2019) |

| Medicare beneficiaries with private supplemental insurance | 22% (2019) |

| Medicare beneficiaries with retiree coverage through a former employer | 18% (2019) |

| Medicare beneficiaries with an out-of-pocket cap through MA plan enrollment | 41% (2019) |

| Medicare beneficiaries with Medicaid | 9% (2019) |

| Medicare beneficiaries with Medicare Advantage | 50% (2022) |

| Medicare beneficiaries with traditional Medicare | 50% (2022) |

| Medicare beneficiaries with no supplemental coverage | 5% (2022) |

| Medicare beneficiaries with supplemental coverage through a group health insurance plan | Individuals 65+ years old: if the employer has <20 employees; persons with disabilities <65 years old: if the employer has <100 employees; individuals 65+ years old with retiree coverage through a former employer |

| Medicare beneficiaries with Medigap insurance | 21% (2022) |

| Medicare beneficiaries with employer- or union-sponsored health insurance coverage | 24% (2022) |

| Medicare beneficiaries with Medigap insurance under 65 years old | 2% (2022) |

| Medicare beneficiaries with Medigap insurance 65+ years old | 11% (2022) |

Explore related products

What You'll Learn

![]()

Medicare Advantage plans vs. traditional Medicare

Medicare Advantage plans, also known as Part C, are issued by private companies and typically combine Part A, Part B, and Part D (prescription drugs) all in one plan. In 2024, nearly 9 in 10 MA plans included prescription coverage, and Medicare Advantage covered 54% of all eligible beneficiaries. Medicare Advantage plans may have zero-dollar premiums, availability of extra benefits, and reduced cost-sharing for many services, as well as an out-of-pocket spending limit. However, they also come with provider networks and prior authorization requirements.

Original Medicare, on the other hand, is administered by the federal government. It consists of Part A, which covers inpatient hospital care, nursing facility care, nursing home care, hospice care, and home healthcare, and Part B, which covers certain doctors' services, outpatient care, medical supplies, and preventive services. Original Medicare does not automatically include prescription drugs, so you may need to purchase a separate Part D plan. Additionally, it does not cover routine dental, hearing, and vision care.

When it comes to supplemental insurance, Medigap, also known as Medicare supplement insurance, is private supplemental health insurance that helps cover cost-sharing requirements for Parts A and B, including deductibles, copayments, and coinsurance. In 2022, Medigap covered 21% of Medicare beneficiaries overall, or 42% of those in traditional Medicare. It is important to note that Medigap does not work with Medicare Advantage plans.

Federal law provides a 6-month guarantee issue period for adults aged 65 and older when they first enroll in Medicare Part B, allowing them to purchase a supplemental Medigap policy. However, these protections do not extend to adults under 65 who qualify for Medicare due to long-term disabilities. Most states do not require insurers to issue Medigap policies to beneficiaries under 65, and premiums may be higher for this age group.

In summary, the choice between Medicare Advantage and traditional Medicare depends on an individual's specific needs and circumstances. Medicare Advantage plans offer convenience and additional benefits but may have provider restrictions, while traditional Medicare provides more flexibility in choosing healthcare providers but may require separate plans for prescription drugs and supplemental coverage to manage out-of-pocket costs.

Life Insurance: Non-Medical Options Explained

You may want to see also

Explore related products

![]()

Racial disparities in Medicare Advantage

Medicare supplement insurance, also known as Medigap, covered 21% of Medicare beneficiaries overall, or 42% of those in traditional Medicare (12.5 million) in 2022. Medigap policies, sold by private insurance companies, fully or partially cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance.

Medicare beneficiaries can choose to receive their Medicare Part A and B benefits through the traditional Medicare program or a Medicare Advantage plan. In 2022, half of Medicare beneficiaries were in traditional Medicare, and most had some form of additional coverage, such as Medigap. Medicare Advantage covered the other half (29.9 million people). Medicare Advantage enrollees were more likely to be Black or Hispanic, self-report relatively poor health, have incomes below $20,000 per person, and have lower levels of education.

A review of 20 studies published between 2018 and 2023 compared quality of care and beneficiary experiences between people of colour in Medicare Advantage and White enrollees. Results are less favourable for Black Medicare Advantage enrollees than White enrollees on more than half (24) of the 46 measures examined for this group in 19 studies. For example, a lower share of Black enrollees received prostate cancer screenings. A higher share of American Indian and Alaska Native enrollees than White enrollees received breast cancer screenings, and similar shares received a flu vaccine. A larger share of Black and Hispanic beneficiaries also reported trouble getting needed care than White beneficiaries.

While relatively few Medicare beneficiaries overall report problems with access to care, the COVID-19 pandemic has further highlighted stark racial/ethnic health inequities among Medicare Advantage enrollees, with Black, Hispanic, and American Indian/Alaska Natives disproportionately affected.

Pet Insurance: Medical Coverage for Your Furry Friends

You may want to see also

Explore related products

![]()

Medicare beneficiaries under 65

Medicare is a federal health insurance program for people aged 65 and over. However, certain individuals under 65 can qualify for Medicare if they:

- Have received Social Security Disability benefits for 24 months.

- Have End-Stage Renal Disease (ESRD).

- Have Amyotrophic Lateral Sclerosis (ALS), also known as Lou Gehrig's Disease.

In 2022, 7.7 million people under 65 with disabilities were covered by Medicare, representing 12% of all Medicare beneficiaries.

Medicare beneficiaries can choose to receive their Medicare Part A and B benefits through the traditional Medicare program or a Medicare Advantage plan. In 2022, half of all Medicare beneficiaries were in traditional Medicare, and most had some form of additional coverage to help with cost-sharing requirements, such as Medigap, employer-sponsored retiree benefits, or Medicaid.

Medigap, or Medicare Supplement Insurance, is private supplemental health insurance that covers Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance. Medigap policies limit the financial exposure of Medicare beneficiaries and provide protection against catastrophic medical expenses.

In 2022, Medigap covered 21% of Medicare beneficiaries overall, or 42% of those in traditional Medicare (12.5 million beneficiaries). However, a smaller share of traditional Medicare beneficiaries under 65 have a Medigap policy compared to those 65 and older (2% vs. 11%). Federal law provides a 6-month guarantee issue period for adults 65 and older when they first enroll in Medicare Part B, but this protection does not extend to adults under 65 who qualify for Medicare due to long-term disability. Most states do not require insurers to issue Medigap policies to beneficiaries under 65, and premiums may be higher for this age group.

In summary, while Medicare beneficiaries under 65 with disabilities make up a significant portion of Medicare enrollees, they face unique challenges in terms of insurance coverage, costs, and access to care. Medigap can provide valuable supplemental coverage for this population, but take-up may be limited by higher costs and a lack of guaranteed issue rights.

Legitimacy of No Insurance Medical Supplies: A Review

You may want to see also

Explore related products

![]()

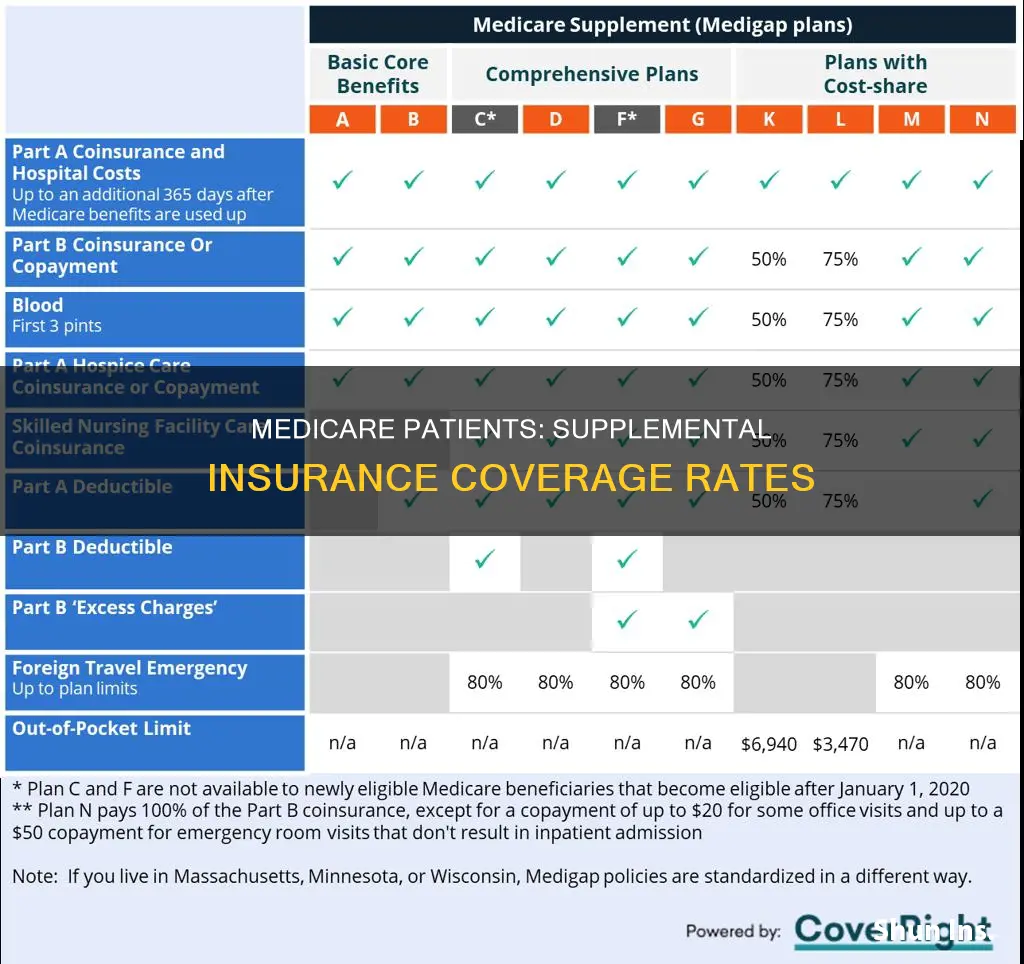

Medicare supplement insurance (Medigap)

Medicare supplement insurance, also known as Medigap, is extra insurance that covers the gaps in Original Medicare. Medigap policies are sold by private insurance companies and help to cover the out-of-pocket costs associated with Medicare Part A and Part B, including deductibles, copayments, and coinsurance. In 2022, Medigap covered 21% of Medicare beneficiaries overall, or 42% of those with traditional Medicare, totalling 12.5 million beneficiaries.

Medigap plays a crucial role in protecting Medicare beneficiaries from catastrophic medical expenses. While Medicare provides financial protection for around 67 million Americans, it does not have a limit on out-of-pocket spending. Medigap policies address this issue by limiting the financial exposure of beneficiaries. As a result, individuals with Medigap are less likely to report cost-related problems compared to those with Medicare Advantage or traditional Medicare without supplemental coverage.

Medigap is particularly important for individuals with modest incomes and limited savings, who may struggle to afford unexpected medical expenses. However, Medigap premiums can be costly, especially for those on lower incomes, and they may increase with age and vary depending on the state. As of 2019, 22% of Medicare beneficiaries had purchased private Medigap policies, making it a significant source of supplemental coverage.

Eligibility for Medigap plans is restricted in certain cases. Federal law does not require Medigap insurers to sell policies to beneficiaries under 65 who qualify for Medicare due to long-term disabilities. Additionally, Medigap does not work with Medicare Advantage plans. As such, Medigap is primarily a source of supplemental insurance for individuals with traditional Medicare who do not have employer-sponsored retiree benefits or Medicaid.

Understanding Coordination of Benefits: Primary Insurance First

You may want to see also

Explore related products

![]()

Medicare cost-sharing requirements

Medicare is the primary payer for beneficiaries in most cases, with any supplemental coverage providing secondary, wraparound coverage. However, Medicare beneficiaries are responsible for Medicare's premiums, deductibles, and other cost-sharing requirements unless they have private supplemental coverage, a Medicare Advantage plan, or qualify for the Medicare Savings Programs and Part D Low-Income Subsidy (LIS).

Medicare supplement insurance, also known as Medigap, covered 21% of Medicare beneficiaries or 42% of those in traditional Medicare in 2022. Medigap policies sold by private insurance companies help cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance. They limit the financial exposure of Medicare beneficiaries and protect against catastrophic medical expenses.

Medigap policies also make healthcare costs more predictable by spreading costs over the year through monthly premium payments and reducing the paperwork burden associated with medical bills. Beneficiaries with Medigap are less likely to report cost-related problems than similar Medicare Advantage enrollees or traditional Medicare beneficiaries without supplemental coverage.

Federal law provides a 6-month guarantee issue period for adults 65 and older when they first enroll in Medicare Part B, allowing them to purchase a supplemental Medigap policy. However, these protections do not extend to adults under 65 who qualify for Medicare due to long-term disabilities. Most states do not require insurers to issue Medigap policies to beneficiaries under 65, and premiums may be higher for this age group.

In 2022, 24% of Medicare beneficiaries, or 14.5 million people, also had employer or union-sponsored health insurance coverage in addition to Medicare Part A and Part B. Medicare Advantage covered half of all Medicare beneficiaries (50%) or 29.9 million people in 2022, with this number increasing to 54% or 33 million in 2024. Medicare Advantage plans can provide an out-of-pocket cap for beneficiaries.

Medicare beneficiaries can choose to receive their Medicare Part A and B benefits through the traditional Medicare program or a Medicare Advantage plan. Most traditional Medicare beneficiaries have additional coverage, such as Medigap, employer-sponsored benefits, or Medicaid, to help with cost-sharing. Medicare beneficiaries with limited incomes and resources may receive assistance with premiums and other costs from their state.

Medical Insurance Deductibles: Tax Implications and Savings

You may want to see also

Frequently asked questions

In 2022, 21% of all Medicare beneficiaries had Medicare supplement insurance, also known as Medigap. This equates to 42% of those in traditional Medicare (12.5 million beneficiaries).

Medigap is a private supplemental health insurance that helps cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance.

Medigap limits the financial exposure of Medicare beneficiaries and provides protection against catastrophic medical expenses. It also makes healthcare costs more predictable by spreading costs over the course of the year through monthly premium payments.

Beneficiaries are eligible to enroll in a Medigap plan during their open enrollment period, which is the first six months of their enrollment in Part B. During this period, Medigap coverage must be offered on a guaranteed-issue basis, meaning insurers cannot deny coverage based on age, gender, or health status.

A larger share of traditional Medicare beneficiaries with Medigap are White (94% vs 86%), have incomes of $40,000 or above (54% vs 47%), and report their health as excellent, very good, or good (88% vs 82%) compared to traditional Medicare beneficiaries overall.