The percentage that truck insurance agents make varies depending on the type of insurance, the size of the policy, and the commission structure of their employer. Most insurance agents are paid on a commission basis, earning a set percentage of the premiums per policy. This is typically calculated as a percentage of either the first-year premiums or the annual premiums if the policy is renewed, with the first-year premium commission usually being higher. The average commission rate for insurance agents ranges from 10% to 20%, but this can differ depending on the state, carrier, policy, and agent. Independent insurance agents generally earn higher commissions than captive agents, but they are responsible for their own business expenses. Additionally, insurance agents can also receive bonuses or profit-sharing incentives from their carriers if they have a profitable year.

| Characteristics | Values |

|---|---|

| Average commission rate | 10% to 20% |

| Commission rate range | 5% to 40% |

| Median wage | $59,080 to $74,000 per year |

| Top earners' salary | Over $135,000 per year |

| Entry-level salary | $20,000 to $26,000 per year |

| Average salary | $48,000 to $109,000 per year |

| Captive insurance agent commission | 5% to 10% |

| Independent insurance agent commission | Up to 15% |

| Life insurance agent commission | 40% to 120% |

| Life insurance agent renewal commission | 1% to 2% |

| Health insurance agent commission | 90%/5% |

| Group policies commission | 3% to 6% |

Explore related products

What You'll Learn

![]()

Captive vs. independent agents

The percentage that truck insurance agents make varies depending on whether they are captive or independent agents.

Captive insurance agents work for a single insurance company and are typically under contract with that insurance carrier. They receive a regular salary, plus commission on the policies sold. They benefit from the insurance company's broader marketing strategy and may receive bonuses and other perks. The company will typically provide them with a salary, commission, and benefits. Many captive insurance agents work as full-time salaried employees for insurance companies, but depending on their contract, they may receive commissions apart from their fixed wages.

Independent agents, on the other hand, work with multiple insurance companies, which increases their access to insurance products and allows them to meet sales quotas by selling policies from various carriers. They typically earn higher commissions than captive agents, but they are responsible for their own business expenses, including rent, office supplies, and advertising and marketing costs. They have more options to offer their clients, which can lead to higher closing ratios and the ability to act in their clients' best interests.

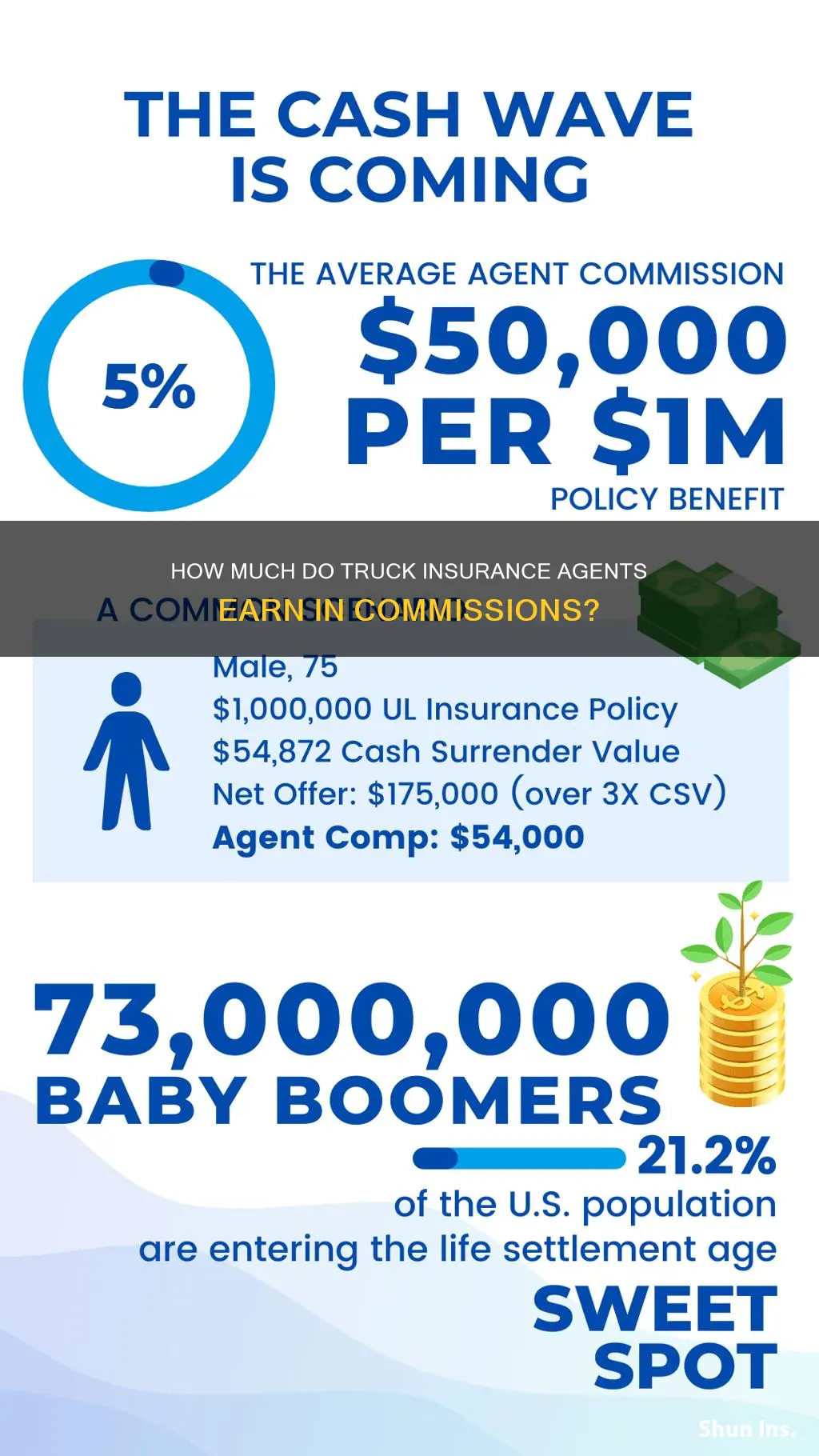

The median wage for insurance agents is around $60,000 to $74,000 per year, depending on the type of insurance they sell. The bottom 10% of earners in the industry made less than $36,390, while the top 10% earned more than $135,000 per year. Commissions for captive agents on auto and home policies are typically around 5% to 10% of the entire premiums paid for the first year, while independent agents may receive about 15%. Life insurance agents can earn commissions of up to 120% of the first-year premiums, while health insurance agents typically earn between 5% and 10%.

Humana: Understanding Private Insurance and Its Benefits

You may want to see also

Explore related products

![]()

Commission structures

The commission structure for insurance agents varies depending on the type of insurance, the company they represent, and the volume of policies sold. There are two main types of insurance agents: captive agents, who work for a single insurer, and independent insurance agents, who may sell policies for a range of carriers.

Captive agents are often paid a salary, but they may also receive commissions. For auto and home policies, captive agents typically earn about 5% to 10% of the entire premiums paid for the first year. Commission rates for renewals range from 2% to 15%, averaging around 2% to 5%. Life insurance agents receive front-loaded commissions of 40% to 120% of a policy's first-year premiums, but renewal commissions drop significantly to 1% to 2%.

Independent agents, on the other hand, are typically paid solely through a commission structure. They usually earn higher commissions than captive agents, with rates ranging from 10% to 20% of the premium cost. For auto and home policies, independent agents receive about 15% of the entire premiums. Health insurance agents, including independent agents specializing in health insurance, earn an average of between 5% and 10% of the policy's total premiums in the first year. Agents selling group policies earn slightly lower commissions at around 3% to 6%. Commercial insurance policies often generate higher commissions due to higher premiums, with rates typically ranging from 10% to 25%.

In addition to premium commissions, insurance agents may receive contingent commissions based on performance metrics such as meeting sales targets or maintaining low claim ratios. Residual commissions, or renewal commissions, are earned on policies with ongoing premiums. This structure promotes long-term relationships between agents and policyholders and provides a stable income over time. The percentage earned on renewal is usually lower than on the original sale. Upfront commissions are earned at the time the insurance policy is sold and are typically a one-time payment, providing a quick boost to an agent's income.

The geographic market can also impact commission structures, as insurance agents in certain states may have different opportunities to sell insurance based on risk. For example, commercial property insurance rates in Texas are typically higher due to weather risks, leading to larger commissions. Experience and reputation also play a role, with established agents often commanding higher commissions or better splits.

Why You Need an Insurance Agent

You may want to see also

Explore related products

![]()

Salary and bonuses

The salary and bonuses of truck insurance agents depend on various factors, including the type of insurance, the size of the policy, and the commission structure of their employer. While some insurance agents work on a straight salary, most insurance agents are paid based on commissions, receiving a set percentage of the premiums per policy. This commission is calculated as a percentage of either the first year of premiums or the annual premiums if the policy is renewed, with the first-year premium commission typically being much higher.

The average commission rate for insurance agents ranges from 10% to 20%, with some agents earning as much as 30% or more. For instance, if an agent sells a policy with an annual premium of $1,200 and the commission rate is 15%, the agent would earn $180 per policy. The commission amount can vary depending on the type of policy and the company, with individual policies ranging from 20% to 40% and group policies having lower commission rates.

For auto and home policies, captive insurance agents typically earn a commission of about 5% to 10% of the entire premiums paid for the first year, while independent agents receive a higher commission of up to 15%. Independent agents have the potential to earn higher commissions due to their access to a wider range of policies, but they also have to bear their own business expenses. The commission rates for renewals usually range between 2% and 15%, averaging around 2% to 5%.

Life insurance agents often receive front-loaded commissions, with rates varying from 40% to 120% of the first-year premiums, but the rates for renewals drop significantly to 1% to 2%. Term life insurance commissions typically fall between 30% and 70% of the first year's premiums, while whole life insurance may pay as high as 120% in commissions. Health insurance sales can also be attractive due to the high demand and mandatory nature of certain types of health insurance.

In addition to commissions, insurance agents may also receive bonuses. Some insurance companies implement profit-sharing programs, rewarding agencies with a percentage of the written or earned premiums when certain revenue targets are met. Agents can also earn bonuses from their carriers if they have a "profitable year," meaning their claim figures are under a certain loss percentage.

According to the Bureau of Labor Statistics (BLS), the median annual wage for insurance sales agents was $59,080 in May 2023, with the top 10% of earners making more than $135,000 per year. However, these figures may vary depending on the source, with some reporting a median wage of $60,000 to $74,000 for licensed insurance agents. Entry-level independent insurance agents may start with an annual salary of $20,000 to $26,000, while the majority of their annual salaries fall between $48,000 and $109,000.

Contacting Your Insurance Agent: After-Hours Support

You may want to see also

![]()

Policy types

Insurance agents typically make a set percentage of the premiums per policy. This is calculated as a percentage of either the first-year premiums or the annual premiums if the policy is renewed, with the first-year premium commission usually being higher. The percentage may vary depending on the type of insurance and the state. For instance, in North Carolina, commission ranges tend to start at 5% and can go up to 20%, with the average being roughly 10%.

Liability Insurance

Liability Insurance is the foundation of trucking insurance policies and is mandated by law in most regions. It serves two purposes: bodily injury liability and property damage liability. Bodily injury liability covers costs associated with injuries to others in an accident involving a truck, while property damage liability covers damages caused by the vehicle to someone else's property. This type of insurance is essential for mitigating the financial repercussions of lawsuits and claims, ensuring that trucking businesses can continue operating without significant disruptions.

Gap Coverage

Gap Coverage is crucial for businesses that finance or lease their vehicles. It bridges the gap between the actual cash value of a vehicle at the time of loss and the amount still owed on its financing or lease agreement. Gap coverage ensures that businesses do not suffer a financial shortfall if a vehicle is stolen or deemed a total loss, protecting them from paying out of pocket for a vehicle they can no longer use.

Physical Damage Coverage

Physical Damage Coverage protects trucks from natural disasters like fires and floods, as well as theft. This type of insurance is particularly important in the trucking industry, where theft is a significant issue.

Non-trucking Liability

Non-trucking Liability, also known as bobtail insurance or deadhead coverage, applies when trucks are travelling without a trailer or are off the road for servicing.

Trailer Interchange Insurance

Trailer Interchange Insurance provides physical damage coverage for non-owned trailers. It protects against damage to trailers due to collision, fire, theft, explosion, or vandalism.

Medical Payment Coverage

Medical Payment Coverage pays for any medical bills incurred by the driver or passengers while in the truck. The extent of this coverage may vary depending on the state.

Cargo Insurance

Cargo Insurance provides protection if the cargo on a commercial truck is lost or damaged. The premiums for this type of insurance will depend on the type of freight being transported.

The above-mentioned policy types are just a few examples of the insurance coverages available to truckers and trucking companies. It is important for truckers and trucking businesses to stay informed about insurance requirements and maintain appropriate coverage to ensure regulatory compliance and adequate protection against financial risks.

Strategies for Independent Insurance Agents to Grow Their Business

You may want to see also

![]()

Location

The location of an insurance agent can have a significant impact on their earnings. The commission-based structure of their pay means that areas with higher insurance premiums will also provide higher commissions. For example, California brokers earned more than the national average, at $39.36 pmpm in the California Small Group marketplace.

The number of available customers in a given area can also affect an agent's income. A large city with a dense population will offer more opportunities to sell insurance than a small town with fewer residents. Competition in a given area can also impact earnings, as it may be harder to get new clients if the market is saturated with agents. Areas with higher renewal rates can also mean higher average incomes for insurance agents.

The type of insurance sold also varies by location and can impact earnings. For example, health insurance is required in California, so agents in that state may focus on health insurance plans. Agents in states with a high number of registered cars and trucks may focus on property and casualty insurance.

Additionally, the commission rates can vary from state to state, carrier to carrier, policy to policy, and sometimes even agent to agent. For instance, in North Carolina, commission ranges tend to start at around 5% and can go up to 20%, while independent agents in other states can earn up to 15% on comparable policies.

Overall, while the location of an insurance agent can impact their earnings, other factors such as the type of insurance sold, the commission structure, and the number of clients also play a significant role in determining their income.

Medi-Cal Insurance: Understanding California's Health Coverage

You may want to see also

Frequently asked questions

The average commission rate for insurance agents ranges from 10% to 20%, with some agents earning as much as 30% or more.

The type of insurance policy significantly impacts an agent's commission. Life insurance agents, for instance, earn higher commissions of 40% to 120% of the first-year premiums, while health insurance agents earn an average of 5% to 10%.

It depends on their contract. Captive insurance agents often work as full-time salaried employees for insurance companies and may receive additional commissions. In contrast, independent agents typically rely solely on commissions.

Yes, insurance companies may offer incentives such as supplemental and contingent commissions or profit-sharing programs for agents who help them achieve specific business targets or have a profitable year.