Health insurance coverage is essential for accessing timely and affordable healthcare. However, the percentage of families without medical insurance varies across the United States, with an overall uninsured rate of around 8% in 2023. This rate differs by age, with 11.1% of adults aged 19-64 uninsured in 2023, a slight decrease from the previous year. Among working-age adults aged 19-64, the uninsured rate was 10.8% in 2022, a decrease from 14.7% in 2019. Racial disparities exist, with higher uninsured rates among Hispanic adults (27.6%) compared to Black, non-Hispanic (13.3%), White, non-Hispanic (7.4%), and Asian, non-Hispanic adults (7.1%). Cost is a significant factor, with many uninsured individuals lacking a regular place to seek medical advice and facing challenges in affording healthcare. The pandemic led to a drop in uninsured rates, and the Affordable Care Act has also contributed to gains in coverage.

Explore related products

What You'll Learn

- Racial disparities: Hispanic adults are most uninsured, followed by Black, non-Hispanic, White, non-Hispanic, and Asian, non-Hispanic adults

- Income disparities: Most uninsured people are in low-income families

- Employment-based insurance: This is the most common type of health insurance, covering over 50% of the population

- Children's insurance coverage: The share of children without health insurance was lower in 2023 than in 2019

- Healthcare affordability: Many uninsured people cite the high cost of insurance as the main reason for lacking coverage

![]()

Racial disparities: Hispanic adults are most uninsured, followed by Black, non-Hispanic, White, non-Hispanic, and Asian, non-Hispanic adults

While the US has made slow progress toward universal, comprehensive health coverage, racial disparities persist. Hispanic adults are the most uninsured demographic, followed by Black, non-Hispanic adults, then White, non-Hispanic adults, and finally, Asian, non-Hispanic adults.

Hispanic people have the highest uninsured rates and the most cost-related problems in getting care. The percentage of uninsured Hispanics is over two times higher than that of Whites. Black individuals are also more likely to be uninsured than Whites and non-Hispanic Whites. People of colour fare worse in terms of access to healthcare resources.

Several factors contribute to these disparities. Policy choices at the federal, state, and local levels have led to economic suppression, unequal educational access, and housing segregation, resulting in worse health outcomes for people of colour. Additionally, the availability of public coverage varies across states, with some states yet to expand eligibility for Medicaid under the Affordable Care Act (ACA).

The high cost of insurance is a significant barrier, particularly for low-income families, who make up a large portion of the uninsured population. Uninsured individuals often lack a regular place to go when they need medical advice, and many struggle to afford healthcare costs. They are also more likely to delay or forgo needed care due to financial concerns.

Disabilities also play a role in insurance disparities. Individuals with disabilities are more likely to be from racial/ethnic minority groups and have lower socioeconomic statuses. They face additional barriers to care, reporting higher out-of-pocket costs and unmet medical needs.

Understanding Tax Deductions: Medical Insurance Premiums and Itemization

You may want to see also

Explore related products

![]()

Income disparities: Most uninsured people are in low-income families

Income disparities are a significant factor contributing to the lack of medical insurance among certain populations. According to various sources, most uninsured individuals belong to low-income families, reflecting the limited availability of public coverage in certain states. Adults aged 19 to 64 are more likely to be uninsured than children, and within this age group, the uninsured rate decreased slightly from 11.3% in 2022 to 11.1% in 2023. Despite this improvement, the percentage of people without health insurance remained at around 8% in 2023, indicating that many still struggle to access coverage.

The high cost of insurance is a significant barrier for low-income families. Even with the implementation of the Affordable Care Act (ACA), which aimed to increase affordability and expand coverage, many individuals are unable to afford the insurance plans available to them. In 2015, 46% of uninsured adults reported that they had tried but failed to obtain coverage due to the high cost. This issue is particularly prevalent in states that have not expanded Medicaid, leaving many adults ineligible for financial assistance.

The consequences of lacking insurance go beyond financial strain. Uninsured individuals face worse access to healthcare, often delaying or forgoing needed medical care due to cost. This can lead to more severe health problems and adverse effects on their health status and mortality. They are less likely to receive preventive care and services for major health conditions and chronic diseases, potentially increasing the risk of infection for themselves and others, as seen during the COVID-19 pandemic.

Racial and ethnic disparities also intersect with income disparities, further complicating the issue. People of color are at a higher risk of being uninsured than non-Hispanic whites. During economic downturns, such as the Great Recession of 2008-2009, black and Hispanic individuals experienced significantly higher unemployment rates, which not only impacts their health but also increases the likelihood of losing employer-sponsored health insurance. These disparities have implications for healthcare access and outcomes, requiring urgent policy interventions to address them.

Overall, income disparities play a significant role in determining who has access to medical insurance. The high cost of insurance and the limitations of public coverage disproportionately affect low-income families, leading to adverse health and financial consequences. Addressing these disparities through policy interventions, such as expanding health insurance coverage for low-income individuals, is crucial to improving the health and economic wellbeing of vulnerable populations.

Insurance Coverage for Medical Alert Systems: What's the Verdict?

You may want to see also

Explore related products

![]()

Employment-based insurance: This is the most common type of health insurance, covering over 50% of the population

Employment-based insurance is the most common type of health insurance in the US, covering over 50% of the population. In 2023, the specific figure was 53.7%. This type of insurance is partially paid for by businesses on behalf of their employees as part of an employee benefit package. Most private (non-government) health coverage in the US is employment-based. Nearly all large employers in America offer group health insurance to their employees, contributing about 85% of the insurance premium for their employees, and about 75% for their employees' dependents. These percentages have been stable since 1999.

The development of employer-based health insurance during World War II has contributed to the difficulty in the United States of enacting reforms to the health insurance system. This system of voluntary employment-based health benefits is not the result of a deliberate plan or policy, but rather a gradual accumulation of factors, including innovations in healthcare finance and conflicting political and social principles.

The availability of employment-based health benefits for active workers in the US has been stable, according to a 2007 analysis by the Employee Benefit Research Institute. However, the "take-up rate", or percentage of eligible workers participating in employer-sponsored plans, has decreased somewhat. The study also found that if a major employer discontinued health benefits, others might follow. A 2007 study also found that about 59% of employers at small firms (3–199 workers) in the US provide employee health insurance, a number that has been steadily dropping since 1999.

While employment-based insurance is the most common type of health insurance, the rate of uninsured individuals in the US is significant. In 2023, the percentage of people without health insurance was around 8%. The uninsured rate for adults aged 19-64 was 11.1% in 2023, and the rate for children under 19 increased to 5.8%. Most uninsured people are in low-income families, and adults in this age range are more likely to be uninsured than children.

Medical Insurance Administrator: Their Role and Responsibilities

You may want to see also

Explore related products

![]()

Children's insurance coverage: The share of children without health insurance was lower in 2023 than in 2019

In 2023, the percentage of people in the United States without health insurance remained around 8%, with about 9 million more people insured than in 2018, the last year of reporting before the COVID-19 pandemic impacted data collection. The increase in insured individuals was partially due to policies implemented during the pandemic, which increased enrollment in public health insurance programs and changes in the labor force.

Children under the age of 19 may have health coverage through various sources, including a parent's private plan or public programs like Medicaid or the Children's Health Insurance Program (CHIP). The share of children under 19 with public insurance rose from 5.9% in 2020 to 6.8% in 2023. The uninsured rate for children under the age of 19 increased by 0.5 percentage points to 5.8% between 2022 and 2023. Despite this uptick in uninsured rates for children in 2023, the share of children without health insurance coverage was lower in 2023 compared to 2019.

Most children under 19 and working-age adults had public insurance. In each year, over three-quarters of children under 19 and about half of working-age adults in poverty had public coverage. The uninsured rate of children under 19 in poverty ranged from 8.3% to 10.3% between 2020 and 2023. About a quarter of working-age adults in poverty were uninsured each year between 2020 and 2023.

Uninsured rates for children vary depending on income and poverty levels. Low-income children, those with family incomes below 200% of the Census poverty threshold, experienced rising uninsured rates in 2023. This could be due to the unwinding of the continuous coverage requirement of Medicaid, which began in 2023. Despite overall gains in coverage during the pandemic, they were most significant for AIAN and Hispanic people and individuals in low-income families.

Passing Life Insurance Medical Exams: Nicotine Strategies

You may want to see also

Explore related products

![]()

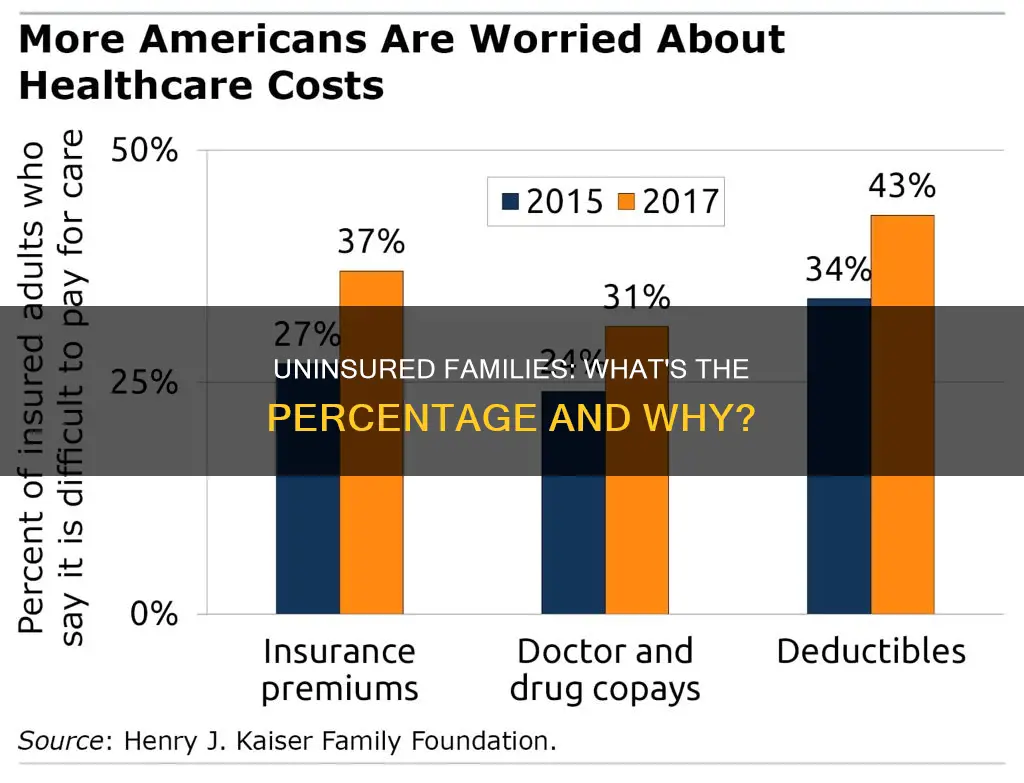

Healthcare affordability: Many uninsured people cite the high cost of insurance as the main reason for lacking coverage

The percentage of people without health insurance in the United States remained around 8% in 2023, with rates varying by age and poverty level. The uninsured rate for adults aged 19-64 decreased to 11.1% in 2023, while the rate for children under 19 increased to 5.8%.

Many uninsured people cite the high cost of insurance as the primary reason for lacking coverage. In 2023, 63% of uninsured adults aged 18-64 said they were uninsured due to the high cost of coverage. Uninsured adults in this age group are much more likely than insured adults to lack confidence in their ability to afford medical costs. Nearly half (49%) of uninsured adults reported that they or a family member had difficulties paying for healthcare, compared to 21% of insured adults. Over 84% of uninsured adults worry that healthcare costs will push them into debt or increase their existing debt, compared to 71% of insured adults.

The lack of access to affordable health coverage is a significant issue for many people. While most working-age adults in the US obtain health insurance through their employer, not all workers are offered this option or can afford the premiums. Medicaid covers many low-income individuals, especially children, but eligibility for adults is limited in states that have not adopted the ACA expansion. Marketplace subsidies can make coverage more affordable, but even with these subsidies, the cost may still be prohibitive for some.

The high cost of healthcare is a burden for many US families, and these costs factor into decisions about insurance coverage. Uninsured adults are more likely to forgo or postpone necessary healthcare due to concerns over costs. About one in five adults (21%) have not filled a prescription due to cost, and a similar proportion have opted for over-the-counter alternatives. Additionally, about one in ten adults have cut pills in half or skipped doses of medicine in the last year to save money.

Insurances: Comprehensive Coverage for Medical Procedures?

You may want to see also

Frequently asked questions

The percentage of people without health insurance remained around 8% in 2023, but rates vary by age and poverty level. In 2022, the overall number of Americans without health insurance dropped by 5.6 million from 2019.

Many uninsured people cite the high cost of insurance as the main reason they lack coverage. Nearly half of uninsured adults said they or a family member had problems paying for healthcare.

People across the insurance system, both public and private, may have plans that don't provide adequate cost protection. This can lead to people skipping needed care or taking on medical debt.

Adults aged 18-64 in non-Medicaid expansion states were twice as likely to be uninsured in 2022 compared to those in Medicaid expansion states. In the same year, more than 1 in 4 Hispanic adults aged 18-64 lacked health insurance, a greater percentage than Black, White, and Asian non-Hispanic adults.