The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the US government that insures bank accounts. FDIC insurance covers traditional bank deposit products, including checking accounts, savings accounts, certificates of deposit (CDs), and money market deposit accounts. The FDIC was founded in 1933 to protect consumers and maintain stability and public confidence in the US financial system. FDIC insurance covers deposits in all types of accounts at FDIC-insured banks, up to $250,000 per depositor, per ownership category. This limit can be exceeded by spreading money across different banks or using programs like IntraFi Network Deposits, which provide FDIC insurance on millions through a network of financial institutions.

| Characteristics | Values |

|---|---|

| Name of Program | Federal Deposit Insurance Corporation (FDIC) |

| Type of Accounts Covered | Checking accounts, savings accounts, negotiable orders of withdrawal (NOW), money market deposit accounts (MMDA), certificates of deposit (CD) |

| Maximum Insurance Coverage | $250,000 per depositor, per FDIC-insured bank, for each account ownership category |

| Joint Accounts Coverage | $500,000 per co-owner |

| Insured Bank Deposit Program Coverage | $5 million for individual accounts and $10 million for joint accounts of two or more people |

| IntraFi Network Deposits Program Coverage | Millions of dollars through a network of financial institutions |

| Insured Accounts | Eligible bank accounts, cash management accounts, CDs, IRAs |

| Non-Insured Accounts | Stocks, bonds, money market funds, cryptocurrency, U.S. Treasury securities (T-bills), safe deposit boxes, annuities, insurance products, regular shares and share draft accounts of credit unions |

| Insured Institutions | FDIC-insured banks |

Explore related products

What You'll Learn

![]()

The Federal Deposit Insurance Corporation (FDIC)

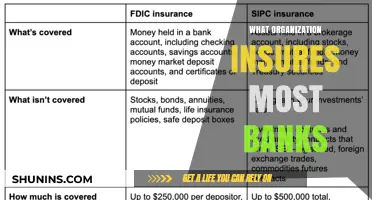

FDIC-insured institutions are permitted to display a sign stating the terms of its insurance, including the per-depositor limit and the guarantee of the United States government. This sign is meant to be a symbol of confidence for depositors. The FDIC insurance is backed by the full faith and credit of the government, and according to the FDIC, "since its start in 1933, no depositor has ever lost a penny of FDIC-insured funds". The FDIC insurance covers traditional deposit accounts such as certificates of deposit (CDs), negotiable orders of withdrawal (NOW), money market deposit accounts (MMDA), checking and savings accounts. However, it does not cover all types of accounts and financial instruments such as stocks, bonds, money market funds, cryptocurrency, U.S. Treasury securities (T-bills), safe deposit boxes, annuities, and insurance products.

The FDIC consists of a five-member Board of Directors, including a Chairman, Vice Chairman, Appointive Director, the Comptroller of the Currency, and the Director of the Bureau of Consumer Financial Protection. No more than three members of the Board can be from the same political party. The FDIC provides extensive resources for bankers, including guidance on regulations, information on examinations, legislation insights, and training programs. It also offers resources to educate and protect consumers, promote economic inclusion, and connect people with financial resources in their communities.

In addition to its insurance role, the FDIC has other responsibilities and initiatives. It regulates and supervises state non-member banks and has the authority to separate commercial and investment banking. The FDIC also works collaboratively with other agencies, such as the Office of the Comptroller of the Currency (OCC), the Board of Governors of the Federal Reserve System (Board), the Farm Credit Administration, and the National Credit Union Administration, to implement and enforce certain financial requirements and regulations.

Insuring Your Bank Deposits: What You Need to Know

You may want to see also

Explore related products

![]()

FDIC insurance limits

The Federal Deposit Insurance Corporation (FDIC) insures bank deposits in the US. FDIC insurance covers eligible bank accounts up to $250,000 per depositor, per FDIC-insured bank, for each account ownership category. This includes principal and any accrued interest through the date of the insured bank's closing. Coverage is automatic when you open a deposit account at an FDIC-insured bank.

FDIC insurance covers deposits in all types of accounts at FDIC-insured banks, including checking and savings accounts, negotiable orders of withdrawal (NOW) accounts, money market deposit accounts (MMDA), and certificates of deposit (CD). However, it does not cover non-deposit investment products, even if they are offered by FDIC-insured banks. It also does not cover regular shares and share draft accounts held at credit unions, which are insured by the National Credit Union Share Insurance Fund, administered by the National Credit Union Administration (NCUA).

FDIC insurance protects your money in the event of bank failure. If a bank fails, the FDIC will reimburse you for any losses you incur, up to the insurance limit. The FDIC helps maintain stability and public confidence in the US financial system. It was founded in 1933 during the Great Depression to protect consumers against losses in the event of bank failures. Since then, no depositor has lost any FDIC-insured funds.

To check if your bank is FDIC-insured, you can use the FDIC's BankFind Suite search tool. You can also use the FDIC's Electronic Deposit Insurance Estimator (EDIE) to calculate how much of your funds are covered by FDIC insurance.

It is important to note that FDIC insurance does not cover all financial products. For example, it does not cover stocks, bonds, money market funds, cryptocurrency, US Treasury securities (T-bills), safe deposit boxes, annuities, or insurance products. Additionally, FDIC insurance does not cover deposits above the $250,000 limit per ownership category, even if they are in different accounts at the same bank. However, you can get around this limit by spreading your money across multiple FDIC-insured banks or by using an Insured Bank Deposit program, which can provide up to $5 million of FDIC insurance ($10 million for joint accounts).

Understanding Private Hire Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Deposit Insurance Fund (DIF)

The Deposit Insurance Fund (DIF) is managed by the Federal Deposit Insurance Corporation (FDIC) to ensure that deposits at member banks are protected. The fund was created in 1933 to maintain public confidence in the financial system. The money in the DIF is used to pay back customers whose money was lost due to the failure of a bank or other financial institutions.

The FDIC insures deposits in each account up to $250,000. This limit applies to each account ownership category. For example, if a customer has a savings account with a balance of $50,000 and a certificate of deposit (CD) with $150,000, both accounts are insured as they fall under the $250,000 limit. The FDIC also offers up to $5 million of FDIC coverage ($10 million for joint accounts of two or more people) through the Insured Bank Deposit program.

The DIF is funded by insurance premiums from FDIC-insured institutions and interest earned on invested funds. Banks pay assessments on their total liabilities, and these assessments must be risk-based. The FDIC's fund management practices were modified by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, which set requirements for the Designated Reserve Ratio (DRR) and redefined the assessment base, used to calculate banks' quarterly assessments. The DRR is the DIF balance divided by estimated insured deposits.

The FDIC developed a comprehensive, long-term plan to manage the DIF, aiming to reduce pro-cyclicality, achieve moderate and steady assessment rates, and maintain a positive fund balance during a banking crisis. The FDIC also manages the level of the DIF to resolve failed banks.

PPO Insurance: Understanding Private Plans and Their Benefits

You may want to see also

Explore related products

$50.85 $63.99

![]()

Non-deposit investment products

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the US government that insures bank deposits. The FDIC was created during the Depression in 1933 to protect customers against the loss of their deposits in the event of bank failure. FDIC insurance covers the principal and interest of eligible bank accounts, up to a limit of $250,000 per account owner. Examples of eligible accounts include checking and savings accounts, money market deposit accounts, and certificates of deposit.

However, it's important to note that the FDIC does not insure all types of accounts or financial institutions. Non-deposit investment products, such as those offered by third-party securities broker-dealers or insurance companies, are not insured by the FDIC. These products may include mutual funds, annuities, life insurance policies, stocks and bonds, and other securities. While these products may be offered on the premises of a financial institution, they are not backed by the same guarantees as FDIC-insured deposits.

When considering non-deposit investment products, individuals should be aware of the higher risks associated with these products. Sales representatives are required to disclose that these products are not insured by the FDIC and are subject to investment risks, including the potential loss of the principal amount invested. It is important for individuals to carefully consider their financial goals, risk tolerance, and investment horizons when evaluating non-deposit investment products.

While non-deposit investment products are not insured by the FDIC, there may be other forms of protection in place. For example, the Securities Investor Protection Corporation (SIPC) provides protection for customers of SIPC-member brokerage firms, replacing missing stocks and other securities in the event of firm failure.

In summary, while FDIC insurance provides important protection for bank deposits, it does not extend to all types of financial products. Non-deposit investment products carry higher risks and individuals should carefully consider their financial objectives and risk tolerance before investing in these products.

Private Insurance vs. Healthcare Marketplace: Which is the Better Option?

You may want to see also

Explore related products

![]()

FDIC-insured banks

The Federal Deposit Insurance Corporation (FDIC) is an independent agency created by the US Congress to maintain stability and public confidence in the nation's financial system. The FDIC insures deposits and examines financial institutions for safety, soundness, and consumer protection. It also makes large and complex financial institutions resolvable and manages receiverships. FDIC insurance covers the principal and interest of an account, not exceeding a $250,000 limit per depositor and per insured bank. This limit applies to all deposits that an account holder has in the same "ownership category" at a single bank or thrift institution.

The FDIC was created during the Great Depression in 1933 to protect consumers and maintain public confidence in the banking system. The FDIC provides deposit insurance to protect account holders' money in the event of bank failure. This means that if you have money in an FDIC-insured bank account and the bank fails, the FDIC will reimburse you for any losses you incur, up to the insured amount. Most banks offer FDIC-insured accounts, and this is often used as a selling point to attract customers.

FDIC insurance covers traditional deposit accounts, such as checking and savings accounts, negotiable orders of withdrawal (NOW) accounts, money market deposit accounts (MMDA), and certificates of deposit (CDs). Coverage is automatic when you open one of these accounts at an FDIC-insured bank. However, it's important to note that the FDIC does not insure all types of accounts or financial institutions. For example, financial instruments such as stocks, bonds, money market funds, cryptocurrency, US Treasury securities (T-bills), safe deposit boxes, annuities, and insurance products are not insured by the FDIC. Additionally, the FDIC does not insure regular shares and share draft accounts held at credit unions; instead, these are insured by the National Credit Union Share Insurance Fund, administered by the National Credit Union Administration (NCUA).

To determine if a bank is FDIC-insured, you can use the FDIC's Bank Find Suite page or contact the FDIC directly. You can also use the FDIC's Electronic Deposit Insurance Calculator to estimate how much of your bank deposits are insured. By utilising FDIC-insured banks, individuals can protect their deposits and maintain confidence in the safety of their money.

Egyptian Banks: Are Your Deposits Insured?

You may want to see also

Frequently asked questions

The FDIC is the Federal Deposit Insurance Corporation, an independent agency of the U.S. government that protects you against the loss of your deposit up to $250,000 if your bank fails.

FDIC insurance covers traditional bank deposit products, including checking accounts, savings accounts, and money market deposit accounts. It does not cover non-deposit investment products, even those offered by FDIC-insured banks.

FDIC insurance covers your money in the event of a bank failure. If your bank fails, the FDIC will either transfer funds to another insured bank or issue a check.

You can check if your bank is FDIC-insured by using the FDIC Bank Find Suite page or the FDIC's Electronic Deposit Insurance Estimator (EDIE).