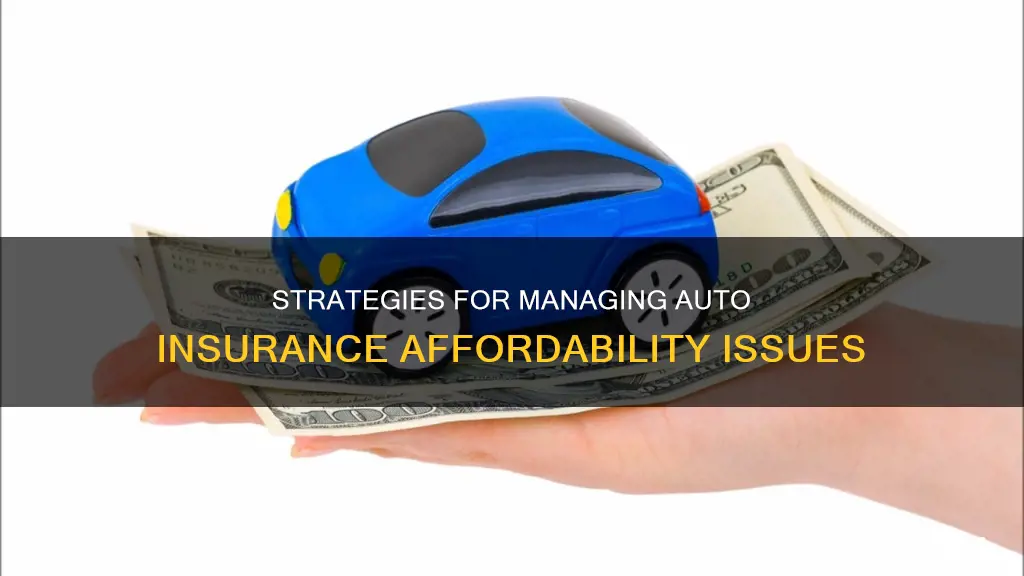

Auto insurance is a necessity, but it can be expensive. If you can't afford it, there are several options to consider. Firstly, don't cancel your policy or drive without insurance, as this can lead to legal and financial repercussions. Instead, contact your insurance company to discuss payment options and discounts. You can also shop around for a new policy, as rates vary across insurers. To reduce costs, consider raising your deductible, changing your coverage, or opting for pay-per-mile insurance. Additionally, improving your credit score and maintaining a clean driving record can lower premiums over time.

Explore related products

What You'll Learn

![]()

Don't cancel your policy

While it may be tempting to cancel your auto insurance policy, especially when you're struggling to afford it, it's important to understand the potential consequences and explore alternative options to keep your coverage. Here are some reasons why you should avoid cancelling your auto insurance policy:

Legal Requirements and Financial Risks:

Almost every state in the US legally requires drivers to carry a minimum amount of car insurance. Driving without insurance can result in an insurance lapse on your record, impacting your future insurance costs and accessibility. An insurance lapse could lead to your state requiring you to file an SR-22 form, which proves you have the minimum auto insurance coverage. This can stay on your record for several years, and some insurers may refuse to cover you during this period.

Additionally, driving without insurance exposes you to significant financial risks. If you cause an accident, you will be responsible for paying out of pocket for any resulting costs, including medical bills and vehicle repairs.

License Suspension and Vehicle Repossession:

Failing to maintain auto insurance can have serious repercussions on your driving privileges. Your license may be suspended, and if you have an auto loan or lease, you could even lose your car through repossession.

Higher Future Premiums:

Cancelling your current policy and starting a new one in the future is typically more expensive than maintaining continuous coverage. Insurance companies consider a lapse in coverage as a risk factor, which may result in higher premiums when you seek insurance again.

Alternative Options:

Instead of cancelling your policy, contact your insurance company to discuss alternative options. They may offer payment plans or discounts that can make your premiums more affordable. You can also explore raising your deductible, reducing your coverage, or switching to pay-per-mile insurance to lower your costs.

Before making any decisions, carefully review your policy, understand the cancellation process and fees, and explore all available options to make an informed choice. Remember, maintaining auto insurance is not just a legal requirement but also a crucial financial safeguard in case of an accident.

Insurance Process for Wrecked Vehicles

You may want to see also

Explore related products

![]()

Contact your insurance company

If you're struggling to afford your car insurance, it's important to contact your insurance company as soon as possible. They may allow you to delay your payment or combine it with future payments. Insurers typically offer a grace period during which you can pay without risking cancellation, but this varies by company and state, so be sure to ask.

It's always better to be proactive than reactive. If you've missed a payment, get in touch quickly to find out how much time you have left. You should also ask about any discounts they offer. You could save money for a variety of reasons, including having a student with good grades, bundling your car insurance with another policy, or signing up for automatic payments and paperless billing.

If you're a safe driver, you might be able to save money by switching to usage-based insurance, which monitors your driving habits and rewards safe and consistent driving with cheaper premiums. Your current insurance company may offer a usage-based discount program, so it's worth asking about this option.

Remember, it's important to maintain your insurance coverage. Driving without insurance is illegal in almost every state and can result in fines, a suspended license, or even jail time.

Alabama Auto Insurance: Understanding No-Fault Claims

You may want to see also

Explore related products

![WSKEN 4 Pack Screen Protector for Apple Watch Series 11/10 42mm - [Auto Align Box] [100% Zero Bubble] [Flexible TPU Film - No Glass] 11 HD Full Coverage for iWatch Cover Accessories](https://m.media-amazon.com/images/I/714mC7bzrmL._AC_UL320_.jpg)

![]()

Raise your deductible

Raising your deductible is a guaranteed way to lower your car insurance costs. Your deductible is the amount you pay out of pocket when filing a claim before your insurance covers the rest. Typically, the higher the deductible, the lower the premium, as you are assuming more financial responsibility in the event of a claim.

For example, if you have a $500 deductible and $3000 in damage from a covered accident, your insurer will pay $2500, and you will be responsible for the remaining $500. If you increase your deductible to $1000, your insurer will only pay $2000, and you will be responsible for the remaining $1000.

While raising your deductible can save you money in the long run, it is important to consider whether you can afford the larger deductible in the event of a claim. You should also evaluate your driving habits and history. If you are a consistently safe driver who doesn't drive often, you might be more comfortable with a higher deductible than those who drive more or have a history of driving violations.

Additionally, consider the types of coverage that typically include deductibles, such as collision, comprehensive, uninsured motorist, and personal injury protection. If you drive an older car, you can likely drop these coverages as they only pay out up to your car's market value minus your deductible.

Before raising your deductible, review your emergency fund to ensure you have enough savings to cover the higher deductible if needed.

Auto Insurance Without Lapse: What You Need to Know

You may want to see also

Explore related products

![]()

Change your coverage

If you're struggling to afford your auto insurance payments, changing your coverage can be a good way to reduce your costs. Here are some ways you can adjust your coverage to make it more affordable:

- Reduce coverage on older cars: If you have an older car, consider dropping comprehensive and collision coverage. Comprehensive coverage includes damage caused by acts of nature, vandalism, theft, and fire, while collision coverage is for damage to your car in a crash. These types of coverage may not be cost-effective if your car is worth less than 10 times the premium. Before making a decision, be sure to check your car's market value and weigh it against the cost of coverage.

- Carry only the required minimum coverage: Each state has a minimum amount of auto insurance that you need to have. While it may not be ideal, you can opt to carry only this minimum amount to reduce your premiums. However, note that minimum coverage typically only includes liability insurance, which covers the expenses of others in the event of a crash you cause. Any damage to your own car will not be covered.

- Increase your deductible: Your deductible is the amount you pay out of pocket before your insurance policy kicks in. By increasing your deductible, you can lower your premiums substantially. For example, raising your deductible from $200 to $500 could reduce your coverage costs by 15-30%. Just be sure that you can afford to pay the higher deductible if you need to make a claim.

- Drop comprehensive and collision coverage: If you drive an older car, you may be able to eliminate comprehensive and collision coverage altogether. Comprehensive coverage includes damage from events like natural disasters, vandalism, or fire, while collision coverage is for damage to your car in a crash. However, if your car is worth less than your deductible, these types of coverage may not provide much benefit. Keep in mind that without these coverages, you'll have to pay out of pocket to replace your vehicle if it's totaled.

- Consider pay-per-mile insurance: If you don't drive often, pay-per-mile insurance could be a more affordable option. This type of insurance charges a base rate plus a fee for each mile driven. It may be worth considering if you use public transportation, work from home, or have a second vehicle that isn't driven frequently.

Switching Auto Insurance: Post-Accident

You may want to see also

Explore related products

![EGV 4 Pack for Apple Watch Series 11/10 Screen Protector 42mm [Auto Install Box] Ultra-thin Soft TPU Film for 42mm Apple Watch Screen Protector [0 Bubbles] Anti-Scratch Max Coverage](https://m.media-amazon.com/images/I/71kC-UuMmrL._AC_UL320_.jpg)

![]()

Shop for a new policy

Shopping around for a new insurance policy is a great way to find cheaper rates. Here are some tips to help you shop for a new policy:

- Compare quotes from multiple insurance companies: Get quotes from at least three different insurance companies to ensure you're getting the best rate possible. This is because auto insurance premiums can vary widely from one insurance company to another.

- Check reviews: While getting a lower quote from a company is great, it doesn't necessarily mean they're the right company for you. Be sure to also check reviews of the company before deciding.

- Look for companies that offer a variety of discounts: Many insurers offer a range of discounts for things like safe driving, customer loyalty, having safety features in your car, or being a good student.

- Check if the company offers a discount for switching: Many insurers will offer you a discount if you switch to them, so be sure to shop around.

- Consider usage-based insurance: If you're a safe driver or don't drive often, consider usage-based insurance. This type of insurance determines the price of your premiums by monitoring your driving habits and can result in cheaper premiums. Some companies, like Root Insurance, will calculate your premiums after tracking your driving through a smartphone app.

- Check if your current insurer offers a usage-based discount: Your current insurance company may offer a usage-based discount program, which works in a similar way to usage-based insurance. You install a plug-in into your vehicle or use a mobile app that tracks your driving, and safe drivers can get a significant discount off their premiums. Examples of these programs include Progressive’s Snapshot, State Farm’s Drive Safe & Save, and Allstate’s Drivewise.

- Trade in your car for a cheaper one to insure: If you haven't bought a car yet, consider the type of car you are buying. Certain vehicles are cheaper to insure than others.

- Check if you qualify for state-subsidized car insurance: Several states, including California and New Jersey, offer programs that help people access car insurance if they can't otherwise afford it. To qualify, you may need to be below a certain income level or be enrolled in Medicaid, for example.

Auto Insurance: Tricks for Discounts

You may want to see also

Frequently asked questions

You should not cancel your policy, as this could have long-term consequences. Instead, you should contact your insurance company to discuss payment options and discounts. You can also shop around for a new policy, as you may be able to get a cheaper rate elsewhere.

You can increase your deductible, reduce your coverage, look for discounts, or drive less. You can also compare prices from multiple insurance companies to find a more affordable policy.

If you are caught driving without insurance, your license could be suspended, and you may be fined or jailed. You will also be responsible for any costs resulting from an accident you cause.

![Mothca 2 Pack Matte Glass Screen Protector for iPhone 17 Pro/iPhone 16 Pro/iPhone 17 6.3-inch [Auto Fit Box Dust-Free] Full Coverage Anti-Glare & Anti-Fingerprint Tempered Glass, Smooth as Silk](https://m.media-amazon.com/images/I/71WfsCFpCAL._AC_UL320_.jpg)

![Ferilinso Full Coverage 3 Pack Privacy Screen Protector for Google Pixel 9 Pro [Phone Case Friendly], 3 Pack Tempered Glass Camera Lens Protector Accessories [Auto- Dusting & Adhesive]](https://m.media-amazon.com/images/I/61eHjK+SkKL._AC_UL320_.jpg)