Credit checks are an important part of the process of applying for homeowners' insurance. In most states, insurance companies use credit-based insurance scores to determine home insurance rates and eligibility. These scores are calculated based on an individual's credit history and are used to assess how risky they are to insure. While a poor credit score can make it harder to find affordable insurance, it is still possible to get homeowners insurance with bad credit.

| Characteristics | Values |

|---|---|

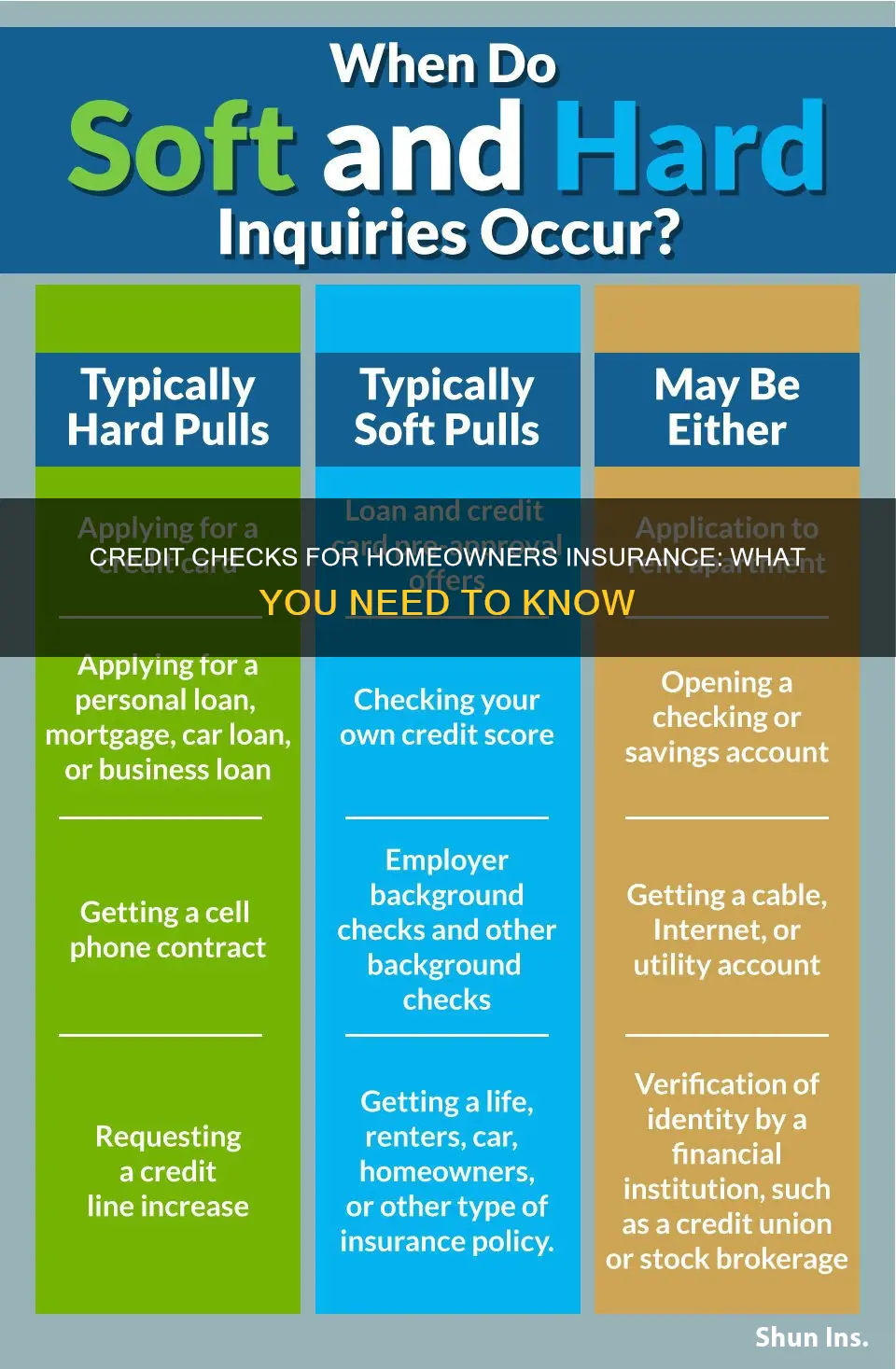

| Type of credit check | Soft credit pull |

| Impact on credit score | Does not impact credit score |

| Credit score impact on insurance | Credit score is one of many factors that insurance companies consider |

| Credit score impact on insurance offers | Credit score can impact whether an insurance offer is made and the premium |

| Credit score impact on insurance renewal | Credit score can impact insurance renewal |

| Credit score impact on insurance cost | A higher credit score is associated with lower insurance costs |

| Credit score impact on insurance in California, Maryland, and Massachusetts | Credit score cannot be used to set insurance prices in these states |

Explore related products

What You'll Learn

![]()

How credit history impacts insurance rates

Credit history is one of the factors that insurance companies consider when determining an individual's insurance rates. Home insurance companies look at a multitude of factors to measure risk, and in most states, credit history is one of them. While the impact of credit history on insurance rates varies across states, it can significantly affect the rates in some cases.

Credit-based insurance scores are used by insurance companies to assess an individual's credit stability and predict the likelihood of filing an insurance claim. These scores are calculated based on various factors, including previous credit performance, payment history, outstanding debt, credit history length, pursuit of new credit, and credit mix. A good credit score indicates lower risk and can lead to lower insurance rates, while a poor credit score can result in higher rates. For example, in the context of homeowners insurance, individuals with poor credit may pay up to 82% more for their insurance compared to those with excellent credit. Similarly, for car insurance, drivers with poor credit may pay up to 104% more for full coverage than those with excellent credit.

It is important to note that insurance scores are not the same as FICO credit scores. FICO scores are calculated by credit bureaus and focus on the likelihood of an individual paying back debt. On the other hand, insurance scores, also known as CBI scores, are calculated by individual insurers and are based on the likelihood of an individual filing an insurance claim. While there is no standardized data, as each company uses its own scoring metric, CBI scores are influenced by similar factors as FICO scores, such as payment history and debt.

Improving one's credit history can have a positive impact on insurance rates. Paying bills on time, maintaining low credit card balances, and regularly checking one's credit report to address errors are essential steps in improving credit health. Additionally, factors such as marital status, location, and the presence of safety and security equipment in the home can also influence insurance rates.

While credit history is a significant factor, it is not the sole determinant of insurance rates. Insurance companies consider various other factors, and it is essential to shop around and compare quotes to find the best rates. In some states, such as California, Maryland, and Massachusetts, the use of credit history as a rating factor for home insurance is prohibited or limited.

Stucco Damage: Is Your Homeowners Insurance Enough?

You may want to see also

Explore related products

$76.49 $99.99

![]()

CBI scores and FICO scores

When it comes to homeowners insurance, your credit history is a crucial factor that insurance companies use to determine your rates. This includes both your CBI (credit-based insurance) score and your FICO credit score. While these two types of scores are similar, there are some key differences to note.

Firstly, CBI scores are calculated by individual insurers and are designed to predict the likelihood of you making an insurance claim. The specific calculation methods vary across different insurance companies, but they generally consider factors such as your payment history, outstanding debt, credit history length, pursuit of new credit, and credit mix. CBI scores are often referred to as "credit scores" or "insurance scores," and they can significantly impact your homeowners insurance rates. A high CBI score can lead to discounted rates, while a low CBI score may result in higher premiums.

On the other hand, FICO credit scores are calculated by credit bureaus and are widely used by lenders to assess the risk of lending money or providing credit cards to individuals. FICO scores range from 300 to 850, with higher scores indicating lower risk. These scores focus on predicting the likelihood of an individual repaying their debts. FICO scores consider similar factors to CBI scores, including payment history, outstanding debt, credit history length, new credit applications, and credit mix. However, the weighting of these factors may differ, with FICO scores placing less emphasis on payment history and credit mix.

While CBI scores and FICO scores have distinct purposes, they are often influenced by similar financial behaviours. Improving your credit history can positively impact both types of scores. This includes paying bills and credit card balances on time, maintaining low credit card balances, and being cautious about opening new lines of credit.

It's important to note that not all states allow the use of credit-based insurance scores in determining homeowners insurance rates. California, Maryland, and Massachusetts prohibit the use of credit as a rating factor for home insurance. Additionally, while your credit score may impact your insurance rates, it is just one of several factors considered by insurers. Other factors, such as claims history, home age, and appliances, also play a role in determining your homeowners insurance premiums.

Home Insurance in Ohio: Is It Mandatory?

You may want to see also

Explore related products

![]()

Credit checks and insurance applications

When applying for homeowners insurance, your credit history and credit-based insurance score can impact whether your application is accepted and how much you'll pay in premiums. Insurers use credit-based insurance scores to evaluate your credit history and calculate premiums in most states. However, it's important to note that California, Maryland, and Massachusetts do not allow credit to be used as a factor in home insurance rates.

Credit-based insurance scores are similar to FICO credit scores but are calculated differently by each individual insurer. These scores are based on various components, including previous credit performance, such as timely bill payments, and the amount and type of outstanding debt. Insurers use these scores to assess the risk of insuring an individual and the likelihood of them filing a claim. A higher credit score indicates lower risk, which can lead to lower insurance rates. Conversely, a lower credit score may result in higher insurance premiums or difficulty in obtaining coverage.

While credit is a significant factor, it is not the sole criterion for an insurance company's decision. Other factors, such as location, marital status, and the presence of certain dog breeds, can also impact insurance rates. Additionally, insurance companies may offer discounts for installing safety and security equipment, bundling policies, or increasing deductibles.

It's worth noting that applying for homeowners insurance typically results in a soft credit inquiry, which does not negatively impact your credit score. Individuals with poor credit can still obtain homeowners insurance, and they may explore options like state Fair Access to Insurance Requirements (FAIR) plans or companies that do not heavily weigh credit history. Shopping around and comparing quotes from different insurers can help individuals find the best coverage at competitive rates.

Rental Insurance: Credit Report Inclusion and Its Benefits

You may want to see also

Explore related products

$111.92 $159.99

![]()

Credit scores and insurance eligibility

While CBI scores are similar to FICO credit scores, they are calculated differently by each insurer and are based on a multitude of factors. These factors include an individual's previous credit performance, such as their payment history, whether they pay their bills on time, and the amount and types of outstanding debt. For example, a $200,000 mortgage is weighed differently from $200,000 in credit card debt.

The impact of credit scores on insurance eligibility varies depending on the state and the insurer. In most states, credit history and CBI scores can influence the availability of homeowners insurance policies and the premium rates. However, in certain states like California, Hawaii, Maryland, Massachusetts, Michigan, Oregon, and Utah, there are strict limitations on the use of credit scores in homeowners insurance decisions. These states prohibit insurance companies from using credit-based scores when offering or renewing policies or setting premium rates.

It's important to note that while credit scores are a factor in insurance eligibility, they are not the sole determinant. Other factors, such as claims history, location, and the specific home being insured, also play a significant role in the insurer's decision-making process.

Additionally, individuals with poor credit histories may still be able to obtain homeowners insurance through alternative options. State FAIR (Fair Access to Insurance Requirements) plans are designed to provide coverage for high-risk individuals who cannot find insurance in the standard market. However, FAIR plans typically offer limited coverage and tend to be more expensive.

To improve insurance eligibility and potentially lower premium rates, individuals can focus on maintaining a good credit history and CBI score by making timely payments, keeping credit card balances low, and regularly reviewing their credit report for errors.

Home and Dorm Insurance: What State Farm Covers

You may want to see also

Explore related products

![]()

Credit scores and insurance in different states

Credit scores are an important factor in determining insurance rates in the United States. While FICO credit scores are a common measure of credit risk, credit-based insurance scores (CBI) are used by insurers to assess a person's overall credit stability and likelihood of filing a claim. These CBI scores are based on credit history, including timely bill payments and the amount and types of debt.

In most states, credit history and CBI scores are considered when determining insurance rates and eligibility. However, the impact of credit scores on insurance varies across different states. California, Hawaii, Maryland, Massachusetts, Michigan, Oregon, and Utah have strict limitations on the use of credit for homeowners insurance. In these states, credit history and CBI scores cannot be the sole reason for denying coverage or increasing premiums.

For example, in California and Massachusetts, credit information is not used for setting homeowners insurance rates. Similarly, in Maryland, homeowners insurance companies cannot refuse coverage or base rates on an individual's credit history. On the other hand, in Hawaii, credit ratings can influence homeowners insurance rates, but they cannot be the sole factor in determining premiums.

In states where credit information is permitted for underwriting and rating insurance policies, CBI scores can significantly impact insurance rates. Individuals with poor credit may face higher insurance rates or difficulty finding affordable coverage. Conversely, those with excellent credit scores may enjoy lower premiums and more favourable insurance options.

It is important to note that insurance companies use various factors beyond credit scores when determining rates and eligibility, such as claims history, location, and the specific characteristics of the property being insured. Additionally, FAIR plans are available in some states as a last resort for individuals who struggle to obtain coverage through the standard insurance market due to credit or other factors.

Update Rite Aid on Insurance Changes: A Step-by-Step Guide

You may want to see also

Frequently asked questions

A credit-based insurance score is a number that describes your overall credit stability in the eyes of an insurance company. It is calculated differently for each individual insurer and is based on your credit history.

In most states, your credit score can impact your homeowner's insurance rates. A higher credit score generally means lower rates, while a lower credit score means higher rates. This is because insurers consider you less risky when you have a higher credit score.

A FICO credit score is calculated by credit bureaus and is used to determine the likelihood of paying back debt. A credit-based insurance score is calculated by individual insurers and is used to determine the likelihood of making insurance claims.

No, not all insurance companies check credit scores. Certain states, including California, Hawaii, Maryland, Michigan, Massachusetts, and Washington, prohibit insurance companies from using credit scores when calculating premiums.

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)