Reinsurance is a crucial risk management tool for insurance companies, allowing them to transfer some of their policy risks to another company, known as the reinsurer. This process is often referred to as insurance for insurance companies, and it helps insurers manage large-scale natural disasters and major claims without overwhelming their financial resources. When a ceding insurer transfers a portion of its risk to an assuming insurer, this is known as Facultative Reinsurance, which allows for greater flexibility in risk selection and pricing. The ceding insurer retains liability for the reinsured policies, and in exchange for assuming a portion of the risk, the reinsurer receives a portion of the premiums from the ceding insurer. This transfer of risk is accomplished through a reinsurance contract, which outlines the conditions under which the reinsurance company will pay out claims.

Explore related products

$114.99 $146

What You'll Learn

![]()

Facultative reinsurance

The ceding insurer approaches the assuming insurer with specific risks, seeking to transfer a portion of the risk associated with those policies. The assuming insurer then has the autonomy to decide whether to accept or decline the specific risk. If the assuming insurer agrees to take on the risk, both parties negotiate the terms, including the reinsurance premium, coverage limits, and conditions of the transfer. This negotiation process is a key feature of facultative reinsurance, enabling a clear understanding and agreement on the coverage specifics and mitigating future disputes. It is a continuous component of the facultative reinsurance process, with each risk presented triggering a new round of negotiations.

Understanding Risk-Spreading Insurance: Protecting Your Assets

You may want to see also

Explore related products

![]()

Treaty reinsurance

Reinsurance is a transaction between two or more insurance companies to apportion risk so that a large loss does not fall on any one company. The insurer transferring part of the risk to another insurer is called the ceding or domestic insurer. The insurer accepting the risk is called the assuming insurer or reinsurer.

Remove Commercial Vehicle Insurance: Federal Filings Simplified

You may want to see also

Explore related products

![]()

Ceding commissions

Reinsurance is a transaction between two or more insurance companies to apportion risk so that a large loss does not fall on any one company. The insurer transferring part of the risk to another insurer is called the ceding or domestic insurer. The insurer accepting the risk is called the assuming insurer or reinsurer.

Ceding insurers transfer a portion of their risk to assuming insurers on a case-by-case basis through Facultative Reinsurance. Facultative Reinsurance allows the ceding insurer to select specific risks that they wish to reinsure with another insurer. The reinsurance contract outlines the conditions under which the reinsurance company will pay out claims. The reinsurer can reject or accept individual parts of a contract proposed by the ceding company or accept or reject the contract in its entirety.

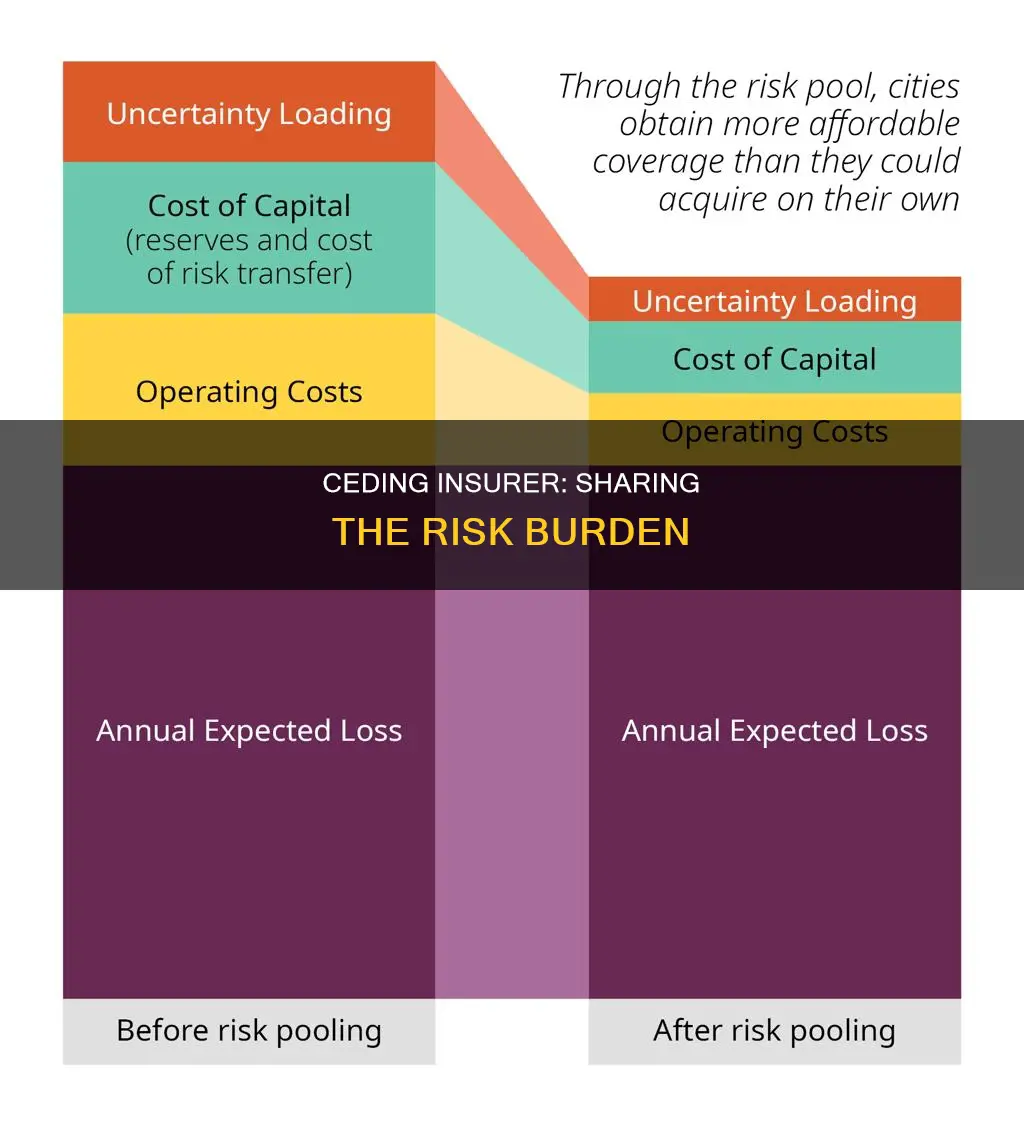

The ceding commission is determined by either the use of a proportional treaty, also called a pro-rata treaty, or a quota share agreement. In a proportional agreement, both the ceding company and the reinsurer share in the premium payment and in covering any claim losses based on an agreed-upon percentage. For example, a ceding insurer may retain 60% of the premium and risk while ceding 40% away. Alternatively, the insurer may use a quota share agreement.

High-Risk Dog Breeds: Insurance and Liability

You may want to see also

Explore related products

![]()

Risk transfer

Reinsurance is a risk-sharing process used by insurance companies to transfer some of their policy risks to another company, the reinsurer. This is also known as "insurance for insurance companies". Reinsurance ceded is the action taken by an insurer to pass off a portion of its obligation for coverage to another insurance company. The insurer seeking to transfer some of its risk to another insurer is known as the ceding company. The company receiving the policy is called the reinsurance company, while the insurer passing the policy to the reinsurer is called the ceding company.

The reinsurance process allows insurance companies to protect themselves against the possibility of a claim for catastrophic damages that would be beyond their financial resources. By offloading some portion of the overall risks they underwrite, the insurance company reduces its overall risk and is able to keep premium costs lower for all of its clients. The agreement between the ceding company and the accepting company is called the reinsurance contract, and it covers all terms related to the ceded risk. The contract outlines the conditions under which the reinsurance company will pay out claims.

There are two main types of reinsurance: facultative and treaty. Facultative reinsurance covers specific individual, generally high-value or hazardous risks, such as a hospital, that wouldn't be acceptable under a treaty. In a facultative reinsurance contract, each type of risk that may be passed to the reinsurer in exchange for a premium is negotiated individually. The reinsurer can reject or accept individual parts of a contract proposed by the ceding company or can accept or reject the contract in its entirety. Treaty reinsurance, on the other hand, covers a broad set of insurance transactions that are covered by reinsurance. For example, the ceding insurance company may cede all of the risks for flood damage, and the accepting company may accept all flood damage risks in a particular geographic area such as a floodplain.

The ceding insurer must manage its reinsurance program to ensure diversification. It must notify the commissioner within 30 days after it has ceded to any one reinsurer or group of reinsurers more than 20% of its gross written premiums in the prior calendar year or determines that the reinsurance ceded is likely to exceed that limit.

Cash Management Accounts: Are Your Funds Insured?

You may want to see also

Explore related products

![]()

Reinsurance market

Reinsurance is a transaction between two or more insurance companies to share and apportion risk so that a large loss does not fall on any one company. The insurer transferring part of the risk is called the ceding insurer, and the insurer accepting the risk is called the assuming insurer or reinsurer. Reinsurance allows insurance companies to protect themselves against the possibility of a claim for catastrophic damages that would be beyond their financial resources. For example, a major hurricane could be financially devastating. By offloading some of the risks they underwrite, the insurance company reduces its overall risk and is able to keep premium costs lower for its clients.

There are two types of reinsurance contracts: facultative reinsurance and treaty reinsurance. Facultative reinsurance is the process where a ceding insurer transfers part of its risk to an assuming insurer on a case-by-case basis. This allows for greater flexibility in terms of risk selection and pricing. In a facultative reinsurance contract, each type of risk that may be passed to the reinsurer in exchange for a premium is negotiated individually. The reinsurer can reject or accept individual parts of a contract proposed by the ceding company or can accept or reject the contract in its entirety. Treaty reinsurance, on the other hand, involves the ceding company and the accepting company agreeing on a broad set of insurance transactions that are covered by reinsurance. For example, the ceding insurance company may cede all of the risks for flood damage, and the accepting company may accept all flood damage risks in a particular geographic area.

The reinsurance market has recently undergone significant changes, with the industry entering a ""hard market"" characterised by significant price rises, limited availability of reinsurance coverage, and increased demand. This shift has been influenced by various factors, including an increase in natural disasters, geopolitical events, inflation, supply chain shortages, and a decrease in available reinsurance capacity. To adapt to these changes, insurance companies have been raising premiums and reducing their risk appetite.

Specialized Commercial Insurance: What's Available?

You may want to see also

Frequently asked questions

Reinsurance is a transaction between two or more insurance companies to apportion risk so that a large loss does not fall on any one company. It is a risk-sharing process used by insurance companies to protect themselves against the possibility of a claim for catastrophic damages that would be beyond their financial resources.

Facultative Reinsurance is the process where a ceding insurer transfers part of its risk to an assuming insurer on a case-by-case basis. Treaty Reinsurance, on the other hand, applies to a broader category of risks and does not allow for individual risk selection. Treaty Reinsurance is typically used for catastrophic events.

Reinsurance allows the ceding insurer to reduce its risk exposure and enhance its financial stability. It also helps the ceding company to free up capital to use in writing new insurance contracts.