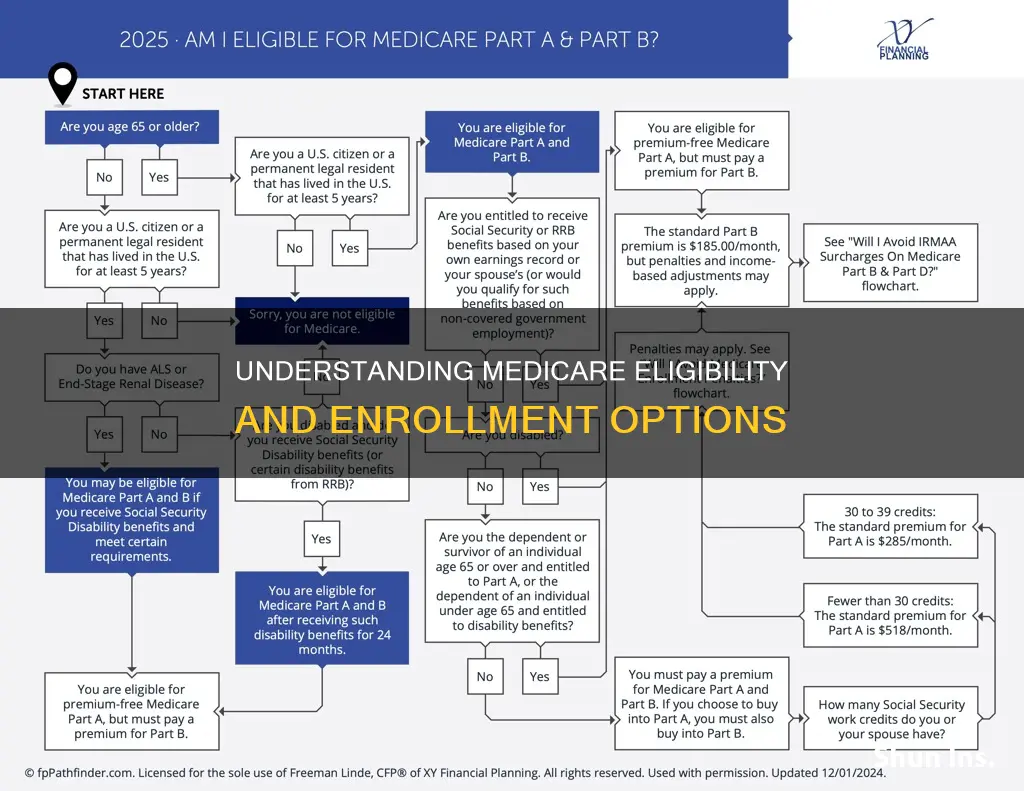

Medicare is a federal health insurance program for people aged 65 and over. The Initial Enrollment Period for Medicare begins 3 months before you turn 65 and ends 3 months after the month you turn 65, lasting a total of 7 months. If you miss this period, you may have to pay a monthly late enrollment penalty and wait to sign up. Most people are eligible for premium-free Part A (Hospital Insurance) if they are 65 or older and paid Medicare taxes while working for a certain amount of time. Part B (Medical Insurance) is also available at this time, but you will pay a monthly premium. If you are under 65, you may still be eligible for Medicare if you have a disability, End-Stage Renal Disease (ESRD), or ALS (Lou Gehrig's Disease).

| Characteristics | Values |

|---|---|

| Age | 65 or older |

| Medicare Taxes | Paid while working for a certain amount of time |

| Initial Enrollment Period | 7 months, starting 3 months before turning 65 and ending 3 months after turning 65 |

| General Enrollment Period | Between January 1 and March 31 each year |

| Part A | Hospital Insurance, free for most people |

| Part B | Medical Insurance, monthly premium |

| Part C | Medicare Advantage Plan, requires Part A and Part B |

| Part D | Medicare drug plan, requires Part A or Part B |

| Disability | Eligible for Medicare before turning 65 |

Explore related products

What You'll Learn

![]()

Initial Enrollment Period

The Initial Enrollment Period for Medicare insurance is a seven-month window that begins three months before your 65th birthday and ends three months after the month you turn 65. This period is when most people sign up for Medicare Parts A and B, as it is when they first become eligible.

Part A is hospital insurance, and most people do not pay a premium for it. If you are 65 or older and receive Social Security benefits, you will be automatically enrolled in Part A. Part A coverage can begin up to six months before the month you apply if you are over 65.

Part B is medical insurance, and you will pay a monthly premium for this coverage. If you don't sign up for Part B when you first become eligible, you will have to wait to sign up, and you may have to go months without coverage. You may also be subject to a monthly late enrollment penalty.

If you miss your Initial Enrollment Period, you may have to pay a monthly late enrollment penalty for as long as you have Part B coverage. This penalty increases the longer you wait to sign up. After your Initial Enrollment Period, you can sign up for Part B and premium Part A during the General Enrollment Period, which runs from January 1st to March 31st each year. Your coverage will begin the month after you sign up.

If you have Medicare due to a disability or ALS, you already have Part A. If you want Medicare coverage to start when your job-based health insurance ends, you need to sign up for Part B the month before you or your spouse plan to retire.

Walgreens Insurance: Understanding Your Medical Coverage Options

You may want to see also

Explore related products

![]()

Medicare Parts A and B

Part A of Medicare primarily covers inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. Most people are eligible for premium-free Part A if they or their spouse have paid Medicare taxes while working for a certain amount of time, typically at least 10 years. Individuals can also qualify for premium-free Part A if they receive monthly Social Security or Railroad Retirement Board (RRB) benefits at least four months before turning 65. Those who are not eligible for premium-free Part A can purchase it.

Part B of Medicare is medical insurance, and individuals pay a monthly premium for this coverage. The premium amount can vary based on income, and it is automatically deducted from Social Security, Railroad Retirement Board, or Civil Service Retirement checks. If an individual does not receive these payments, they will receive a bill for their Part B premium.

The Initial Enrollment Period for Medicare Parts A and B starts three months before an individual turns 65 and ends three months after their 65th birthday. Coverage begins on the first day of the month. If an individual misses this seven-month window, they may have to pay a monthly late enrollment penalty for as long as they have Part B coverage.

It is important to note that Medicare Advantage (Part C) is an alternative to Parts A and B, offering "bundled" coverage that includes Parts A, B, and usually Part D (prescription drug coverage). Individuals must have either Part A or Part B before enrolling in Medicare Advantage.

Finding Your Medical Insurance Provider: Decoding Your Card

You may want to see also

Explore related products

![]()

Monthly premium for Part B

Medicare is a health insurance program for people aged 65 and over who have paid Medicare taxes while working for a certain amount of time (usually at least 10 years). Most people become eligible for Medicare when they turn 65. This is known as the Initial Enrollment Period, which lasts for 7 months, starting 3 months before your 65th birthday and ending 3 months after the month you turn 65.

During this Initial Enrollment Period, you can sign up for Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). While most people do not pay a premium for Part A, you are required to pay a monthly premium for Part B coverage. This premium must be paid every month, even if you don't use any Part B-covered services.

The monthly premium for Part B can vary based on your income and may change each year. Most individuals have their premium deducted automatically from their Social Security, Railroad Retirement Board, or Civil Service Retirement check. However, if you do not receive these payments, you will receive a bill for your Part B premium, which you must pay directly to Medicare.

It is important to enroll in Part B when you are first eligible to avoid penalties. If you miss your Initial Enrollment Period, you may have to pay a monthly late enrollment penalty for as long as you have Part B coverage. This penalty increases the longer you wait to sign up. Therefore, if you want your Medicare coverage to start when your job-based health insurance ends, it is recommended to sign up for Part B the month before you or your spouse retires.

Best Time to Get Your Breast Pump via Insurance

You may want to see also

Explore related products

![]()

Special Enrollment Period

A Special Enrollment Period (SEP) allows you to enroll in Medicare or make changes to your Medicare coverage outside of the standard enrollment periods. There are two types of SEPs:

Qualifying Life Events

If you experience certain life events, you may qualify for a two-month SEP to switch your Medicare Advantage or Part D plan. Qualifying life events include:

- Moving, especially outside your current plan's service area

- Losing other health coverage

- Natural disasters or emergencies

Working Past 65

If you qualified to delay Medicare enrollment because you had creditable coverage, usually from an employer, you are eligible for an eight-month SEP to enroll in Medicare Parts A, B, C, and D when your employer coverage ends. Note that you only have the first two months of this SEP to enroll in Part C or Part D without penalty.

To qualify for the Part B SEP, you must have creditable employer or union health coverage based on current employment. Your SEP will begin eight months after your employer coverage ends or you leave your job, whichever happens first.

It is important to note that a Special Enrollment Period is only available for a limited time. If you don't sign up during your SEP, you may have to pay a monthly late enrollment penalty until you turn 65.

Get on Insurance Panels: A Guide for MFT Interns

You may want to see also

Explore related products

![]()

Medicare Advantage Plans

Part A (Hospital Insurance) is usually premium-free, and most people sign up for it when they turn 65. However, if you don't qualify for premium-free Part A, you might be able to buy it. Part B (Medical Insurance) comes with a monthly premium that you pay even if you don't use any of the covered services. The premium can change each year and may be higher depending on your income.

Your Initial Enrollment Period for Medicare starts 3 months before you turn 65 and ends 3 months after your 65th birthday. If you miss this 7-month window, you might have to pay a monthly late enrollment penalty for as long as you have Part B coverage. The penalty increases the longer you wait to sign up.

After your Initial Enrollment Period, you can still sign up for Medicare during the General Enrollment Period, which is from January 1 to March 31 each year. Your coverage will start the month after you sign up, and you might still be subject to late enrollment penalties.

Before joining a Medicare Advantage Plan, it is important to talk to your employer, union, or benefits administrator about their rules, as enrolling in Part C may cause you to lose your employer or union coverage.

Medicaid and Boston University: Can It Replace Student Health Insurance?

You may want to see also

Frequently asked questions

You can sign up for Medicare when you turn 65. This is called your Initial Enrollment Period and it lasts for 7 months, starting 3 months before your 65th birthday and ending 3 months after.

No, but it is recommended that you do, as you may have to pay a monthly late enrollment penalty if you sign up later.

If you or your spouse have health insurance through your job, you can sign up for Medicare at any time while you're still covered by that plan. You can also sign up within 8 months of the day you or your spouse stop working or within 8 months of the group health plan ending.