Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that can be purchased from a private insurance company to help cover out-of-pocket costs in Original Medicare. The best time to buy a Medigap policy is during the Medigap Open Enrollment Period, which is a one-time, 6-month period that starts the first month an individual has Medicare Part B and is 65 or older. During this period, individuals can enrol in any Medigap policy, and insurance companies cannot deny coverage due to pre-existing health conditions. After this period, purchasing a Medigap policy may be more difficult and expensive, and it may only be available in specific circumstances. To purchase a Medigap policy, individuals should compare plans, select the plan that meets their needs, and buy from a licensed insurance company in their state.

| Characteristics | Values |

|---|---|

| What is Medicare Supplemental Insurance? | Extra insurance bought from a private insurance company to help pay your share of out-of-pocket costs in Original Medicare. |

| When to sign up for Medicare Supplemental Insurance | During your Medigap Open Enrollment Period, a 6-month period starting the first month you have Medicare Part B and are 65 or older. |

| What if I miss the Medigap Open Enrollment Period? | Your options to buy a Medigap policy may be limited and the policy may cost more. |

| What is the benefit of signing up during the Medigap Open Enrollment Period? | You can enroll in any Medigap policy, and insurance companies cannot deny you coverage due to pre-existing health problems. |

| What if I am under 65? | Federal law does not require insurance companies to sell Medigap policies to people under 65, but some states offer Medigap policies to people under 65. |

| How to choose a plan? | Compare the benefits of each lettered plan and select the plan that meets your needs. Price is the only difference between plans with the same letter sold by different companies. |

| How to buy a Medigap policy? | You can buy a Medigap policy from any insurance company licensed in your state to sell one. |

| What to watch out for? | Illegal practices by insurance companies. |

Explore related products

What You'll Learn

![]()

Medicare Supplement Insurance (Medigap)

Medicare Supplement Insurance, also known as Medigap, is extra insurance provided by private insurance companies to help pay your share of out-of-pocket costs in Original Medicare. Medigap policies are standardized, meaning that policies with the same letter offer the same basic benefits, regardless of the insurance company or where you live. There are 10 different types of Medigap plans offered in most states, named by letters from A-D, F, G, and K-N. The price is the only difference between plans with the same letter sold by different insurance companies.

To be eligible to buy a Medigap policy, you must have Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). You can sign up for Medicare during your Initial Enrollment Period, which starts three months before you turn 65 and ends three months after your 65th birthday. If you sign up during this period, your coverage will begin on the first day of the month in which you turn 65. It is recommended to sign up when you are first eligible to avoid gaps in coverage and potential penalties. If you miss the Initial Enrollment Period, you may qualify for a Special Enrollment Period of eight months, which starts when you stop working or lose your current coverage.

Once you have enrolled in Original Medicare, you will have a six-month Medigap Open Enrollment Period to purchase a Medigap policy. During this period, insurance companies cannot deny you coverage due to pre-existing health conditions. If you miss this open enrollment period, you may not be able to purchase a Medigap policy, or it may cost more. Therefore, it is important to be aware of the enrollment periods and plan accordingly.

When choosing a Medigap policy, it is essential to review the coverage and compare plans side-by-side to ensure it meets your needs. You should also check if your doctors and pharmacies are in the plan's network and understand the costs, such as monthly premiums and deductibles. Additionally, be cautious of illegal practices by insurance companies and protect yourself while shopping for a Medigap policy. You can contact your local State Health Insurance Assistance Program (SHIP) to receive free and personalized health insurance counseling to help you make an informed decision.

Medical Insurance for Your Child: California Application Guide

You may want to see also

Explore related products

![]()

When to sign up for Medicare Part A and B

Medicare Part A and Part B are generally the first steps of Medicare coverage. Part A is Hospital Insurance, and Part B is Medical Insurance. Most people sign up for both when they are first eligible, which is usually when they turn 65. You can sign up for Part A and Part B starting 3 months before you turn 65 and ending 3 months after you turn 65.

There are risks to signing up later, such as a gap in your coverage or having to pay a penalty. If you miss an enrollment period, you might qualify for a Special Enrollment Period. For example, if you want Medicare coverage to start when your job-based health insurance ends, you need to sign up for Part B the month before you or your spouse plan to retire. Your coverage will then start the month after Social Security (or the Railroad Retirement Board) gets your completed forms.

If you have to pay a premium for Part A, you can ask if your state will pay it for you. Your state may ask you to contact Social Security to sign up for Part A. Depending on the type of Medicaid you have, you may also qualify to get help paying your share of Medicare costs.

Your Medigap Open Enrollment Period, which is when you can buy Medicare Supplement Insurance (Medigap) from a private insurance company, starts when you have Part B and are 65 or older. During this 6-month period, you can enroll in any Medigap policy, and the insurance company cannot deny you coverage due to pre-existing health problems. After this period, you may not be able to buy a Medigap policy, or it may cost more.

Medical Insurance: What's the Right Budget Allocation?

You may want to see also

Explore related products

![]()

Medigap Open Enrollment Period

Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy you can buy from a private insurance company. It helps pay your share of out-of-pocket costs in Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). Medigap policies are standardized, meaning that policies with the same letter offer the same basic benefits regardless of the insurance company.

The Medigap Open Enrollment Period is a one-time, six-month period that starts the first month a person is 65 or older and has Medicare Part B. During this time, individuals can enroll in any Medigap policy, and insurance companies cannot deny coverage due to pre-existing health conditions. It is important to note that the Medigap Open Enrollment Period is not an annual occurrence like the Medicare Open Enrollment Period.

If you miss the Medigap Open Enrollment Period, your options for purchasing a Medigap policy may be limited, and the policy may cost more. In certain situations, you may be able to buy a Medigap policy outside of the Medigap Open Enrollment Period. These situations are called "guaranteed issue rights" or "Medigap protections," and you can check with your State Insurance Department to understand your rights in this regard.

Additionally, if you are under 65 and have Medicare due to a disability or ESRD (End-Stage Renal Disease), you may not be able to purchase a Medigap policy until you turn 65. However, some states do offer Medigap policies to individuals under 65, so it is worth checking with your State Insurance Department to understand your specific state's laws and rights.

To summarize, the Medigap Open Enrollment Period is a one-time, six-month window that begins when an individual turns 65 and enrolls in Medicare Part B. During this period, they can freely enroll in any Medigap policy without worrying about pre-existing health conditions affecting their coverage. If you miss this window, your options may be limited, and policies may be more expensive. However, there are exceptions and state-specific variations, so it is important to consult official sources and your State Insurance Department for personalized advice.

Medical Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

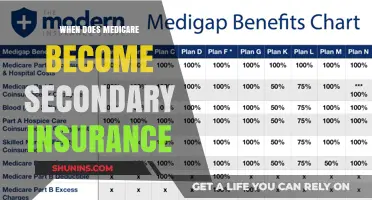

Comparing Medigap policies

Medicare Supplement Insurance, or Medigap, is extra insurance you can buy from a private insurance company to help pay your share of out-of-pocket costs in Original Medicare. You can only buy Medigap if you have Original Medicare, which means signing up for Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) before purchasing a Medigap policy.

When comparing Medigap policies, it's important to review the benefits offered by each plan, including Plan A, Plan B, Plan C, and more. All Medigap policies are standardized, meaning policies with the same letter offer the same basic benefits regardless of the insurance company or location. However, price is the differentiating factor between plans with the same letter sold by different insurance companies. In some states, you may have the option to purchase a Medicare SELECT policy, which allows you to change your mind within 12 months and switch to a standard Medigap policy.

Medigap policies cover a range of benefits, including full or partial coverage for coinsurance, copayments, deductibles, and specific medical services. For example, Medigap typically covers hospice care, which includes inpatient and outpatient care, prescription drugs, counselling, and social services. Additionally, Medigap policies enable you to see any doctor who participates in Medicare, providing access to a vast network of providers across the United States.

When comparing Medigap policies, consider the following:

- Review the benefits covered by each plan and choose the one that best suits your needs.

- Compare plans side-by-side to understand the differences in coverage and cost.

- Check if the plan covers your prescriptions and includes the benefits you require.

- Evaluate the costs, such as monthly premiums, deductibles, and estimated yearly expenses for any medications you take.

- Be aware of any illegal practices by insurance companies and protect yourself during the shopping process.

Medigap policies are an excellent option for those seeking to supplement their Original Medicare coverage. By comparing the available plans, you can make an informed decision based on your specific needs and budget. Remember to consider the benefits, costs, and accessibility offered by each Medigap policy before making your choice.

Inadequate Medical Insurance: What to Do?

You may want to see also

Explore related products

![]()

Protecting yourself from illegal insurance practices

Medicare is a federal health insurance program that covers most healthcare costs for people aged 65 and up, as well as certain individuals under 65 with disabilities. Medicare has two parts: Part A, which covers hospital services, and Part B, which covers other medical expenses. You can buy Medicare supplement insurance, also known as Medigap insurance, from a private insurance company to help pay for out-of-pocket costs that Medicare doesn't cover.

When signing up for Medicare and considering supplemental insurance, it's important to protect yourself from illegal insurance practices. Here are some ways to do that:

- Be aware of illegal Medigap practices: Medigap policies are part of the Medicare program, and it is illegal for Medigap insurance companies to claim to be Medicare representatives. They also cannot sell you a Medigap policy that isn't allowed in your state, ask about your family history or require genetic testing, or imply that the policy is approved or recommended by the federal government.

- Understand your needs and the coverage offered: Review what Medigap covers and compare plans side-by-side. Understand how Medigap works with other Medicare coverage and whether you truly need supplemental insurance. For example, if you have group health insurance through an employer or a Medicare Advantage plan, you may not need Medigap.

- Avoid duplicate coverage: It is illegal to sell you more than one Medicare supplement policy. However, insurance companies may offer other policies with different benefits, such as cancer, specified disease, hospital indemnity, and long-term care policies. Be aware of any duplication of benefits and understand that paying for duplicate coverage is usually a waste of money.

- Verify licenses and buy from a trusted agent: Ensure that both the insurance agent and the company are licensed. Try to purchase from an agent you know and trust, and ask friends or family for recommendations. Ask questions and take notes during your conversations with agents.

- Utilize free resources and support: Contact your local State Health Insurance Assistance Program (SHIP) to receive free personalized health insurance counseling. They are not connected to any insurance company or health plan, so you can get unbiased advice. Additionally, if you live in another state for part of the year, remember to check if your plan will cover you there.

- Review costs and benefits: Before joining a plan, review the costs, such as monthly premiums and deductibles, and estimate your yearly costs, especially for any prescription drugs you take. Check if your doctors and pharmacies are in the plan's network.

Remember, it's important to be vigilant and informed when shopping for Medigap policies to protect yourself from illegal insurance practices and make the best decisions for your healthcare needs.

Understanding Medical Insurance Claims: Eligibility and Process

You may want to see also

Frequently asked questions

Medicare Supplemental Insurance, also known as Medigap, is extra insurance that you can buy from a private insurance company to help pay your share of out-of-pocket costs in Original Medicare.

The best time to buy Medicare Supplemental Insurance is during the Medigap Open Enrollment Period. This is a one-time, 6-month period that starts the first month you have Medicare Part B and are 65 or older. During this time, you can enrol in any Medigap policy, and insurance companies cannot deny you coverage due to pre-existing health conditions.

If you miss the Medigap Open Enrollment Period, your options to buy a Medigap policy may be limited, and the policy may cost more. In some cases, insurance companies may not be required to sell you a Medigap policy after this period. However, there are certain situations where you may still be able to buy a Medigap policy outside of the Medigap Open Enrollment Period, such as having guaranteed issue rights or Medigap protections.

To be eligible for Medicare Supplemental Insurance, you must have Original Medicare, which includes Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). Additionally, you must be 65 or older, although some states offer Medigap policies to people under 65 in certain circumstances, such as having a disability or End-Stage Renal Disease (ESRD).