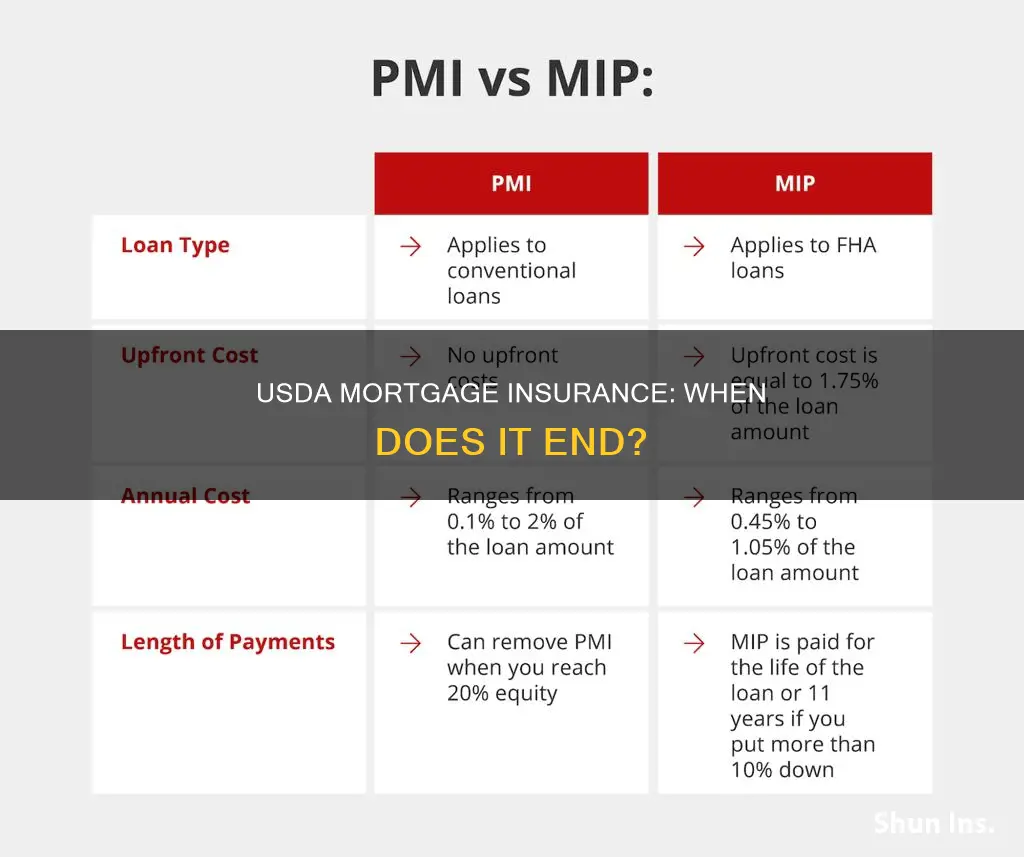

USDA loans are an affordable option for homebuyers in eligible rural and suburban areas. While USDA loans do not require private mortgage insurance (PMI), they do have two types of mortgage insurance fees: an upfront guarantee fee of 1% of the loan amount and an annual fee of 0.35% of the loan amount. These fees are paid for the life of the loan and help protect the lender against potential losses if the borrower defaults. The annual fee is calculated annually but paid monthly as part of the monthly mortgage payment. While there is no set time for when USDA mortgage insurance drops off, paying off the loan or refinancing to a conventional loan without PMI are options to stop paying the fees.

| Characteristics | Values |

|---|---|

| USDA mortgage insurance requirement | Not technically required but similar fees apply |

| Nature of fees | Upfront guarantee fee and an annual fee |

| Upfront guarantee fee | 1% of the loan amount |

| Annual fee | 0.35% of the loan amount |

| Annual fee payment frequency | Monthly |

| Annual fee payment duration | For the life of the loan |

| Annual fee purpose | Serves as protection for lenders against potential losses |

| Property location | USDA-eligible rural or suburban area |

| Income requirement | Household income must fall within USDA's income limits for the area |

| Credit score requirement | No official minimum score but typically 640 or higher |

Explore related products

What You'll Learn

![]()

USDA loans don't require PMI

USDA loans do not require private mortgage insurance (PMI). However, they do have what is called a guarantee fee, which functions similarly to mortgage insurance by protecting the lender. This guarantee fee is paid in two parts: an upfront fee of 1% of the loan amount, and an annual fee of 0.35% of the remaining principal. These fees are included in your monthly mortgage payment and are paid for the life of the loan.

USDA loans are backed by the US Department of Agriculture and are designed for people who want to live outside urban areas. They are geared towards lower-income home buyers in eligible rural and suburban areas. The home must be the buyer's primary residence, and their income must fall within the USDA's limits for the area.

USDA loans offer competitive interest rates and flexible credit score requirements, with most lenders accepting scores as low as 640. They also have no down payment requirement, making them an affordable option for eligible home buyers.

While USDA loans do not require PMI, they do have associated fees that function similarly to mortgage insurance. These fees help keep the loan sustainable and protect the lender in the event of default.

Haven Insurance: Easy Accident Reporting

You may want to see also

Explore related products

![]()

USDA loans require two fees

USDA loans do not require private mortgage insurance (PMI). However, they do require two different forms of mortgage insurance: an upfront guarantee fee and an annual fee. The upfront guarantee fee, also referred to as the USDA funding fee, is typically equal to 1% of the loan amount and is paid at closing. Borrowers can also choose to finance this fee into their loan to avoid the extra cost at closing. The annual fee, which serves as the monthly mortgage insurance premium, is typically 0.35% of the loan amount and is paid for the life of the loan. This fee is calculated annually but paid as part of the monthly mortgage payment.

These fees help to guarantee the loan, as USDA loans are government-backed. If a borrower defaults on a USDA loan, the government agency pays the lender to help them recoup their losses. While USDA loans have two fees, the total costs of mortgage insurance are often significantly lower than other loan options. Mortgage insurance costs on FHA and conventional loans can be double or triple those of USDA mortgages, making them a more affordable option for low-income buyers.

USDA loans are designed for low-to-average income families looking to purchase homes in rural areas. They are one of only two major loan products that do not require a down payment, the other being VA loans, which are for those with eligible military service. While a down payment is not required for a USDA loan, it can lower the loan and guarantee fee amounts. For example, a $10,000 down payment on a $250,000 loan would lower the guarantee fee from $2,500 to $2,400.

In addition to the guarantee and annual fees, there are also closing costs associated with USDA loans. These costs can total thousands of dollars and vary by lender and company. While some fees are standard across all mortgage types, there are also unique fees associated with the USDA rural development loan program. It is important for borrowers to understand these closing costs when considering a USDA loan.

Missed Event Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

USDA loans are for rural homes

USDA loans are a type of mortgage geared towards lower-income home buyers in areas deemed rural by the U.S. Department of Agriculture, the agency that guarantees these loans. The USDA's Single-Family Housing Guaranteed Loan Program assists approved lenders in providing low- and moderate-income households the opportunity to own adequate, modest, decent, safe, and sanitary dwellings as their primary residence in eligible rural areas.

To qualify for a USDA loan, the home must be in a USDA-eligible rural or suburban area. You can check this using the USDA's property eligibility map. The home must be your primary residence—no vacation homes or investment properties. The program provides a 90% loan note guarantee to approved lenders to reduce the risk of extending 100% loans to eligible rural homebuyers.

USDA loans do not require private mortgage insurance (PMI). However, they require two different forms of mortgage insurance: an upfront guarantee fee and an annual fee that serves as the monthly mortgage insurance premium. The upfront guarantee fee is equal to 1% of the loan amount, while the annual fee is 0.35% of the loan amount. These fees help guarantee the loan and protect the lender in the event of default.

USDA loans offer lower interest rates compared to conventional or FHA loans, making them an affordable option for homebuyers in eligible rural areas.

Marketplace Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

USDA loans have low MIP rates

USDA loans are a type of mortgage geared towards lower-income home buyers in rural or suburban areas deemed eligible by the US Department of Agriculture. The USDA guarantees these loans, which are funded directly by the USDA under its Rural Development Program.

USDA loans do not require private mortgage insurance (PMI). However, they do have what is called a guarantee fee, which works like mortgage insurance by helping to guarantee the loan. This guarantee fee is paid via two fees: an upfront fee of 1% of the loan amount, and an annual fee of 0.35% of the loan amount. These fees are comparable to and often significantly lower than the mortgage insurance costs on FHA and conventional loans, making USDA loans a more affordable option for low-income buyers.

The upfront guarantee fee is a one-time fee, also referred to as the USDA funding fee, and is typically financed into the loan. The annual fee, on the other hand, is paid monthly as part of the borrower's monthly mortgage payment and is paid for the life of the loan.

USDA loans offer competitive interest rates, flexible credit requirements, and the option of zero down payment, making them an attractive mortgage option for buyers in eligible rural and suburban areas.

Insuring Your Dream Home Build

You may want to see also

Explore related products

![]()

USDA loans have no down payment

USDA loans are a great option for homebuyers who cannot afford a down payment. These loans are specifically designed to help people purchase homes in rural and some suburban areas, encouraging economic development in these communities.

USDA loans do not require a down payment, which is a significant advantage for buyers who may be struggling to save for a home. The USDA loan program is aimed at lower-income buyers, and the loans are guaranteed by the USDA Rural Development Guaranteed Housing Loan Program, a part of the U.S. Department of Agriculture.

While USDA loans do not require a down payment, there are some upfront costs. These include a guarantee fee, which is similar to mortgage insurance and helps to guarantee the loan. This is a one-time upfront fee of 1% of the loan amount, paid at closing and typically financed into the loan. There is also an annual fee of 0.35% of the loan balance, paid monthly as part of the mortgage payment.

USDA loans are an incredibly affordable option for buyers in eligible rural and suburban areas. The loans have relatively low overall costs compared to other mortgage types, and the interest rates are often lower than those of conventional mortgages. This is because the government backs the loans, taking on the risks associated with lending.

To qualify for a USDA loan, there are several requirements that must be met. Firstly, the home must be in a USDA-eligible rural or suburban area, which can be checked using the USDA's property eligibility map. Secondly, the household income must fall within the USDA's income limits for the area, which vary based on location and family size. The income cannot exceed 115% of the median household income in the area. Other requirements include the home being the primary residence and a minimum credit score of 640.

Cheap Insurance: Worth the Risk?

You may want to see also

Frequently asked questions

USDA loans do not technically require mortgage insurance, but they do have what’s called a guarantee fee, which works like mortgage insurance in helping to guarantee the loan.

The guarantee fee for USDA loans comes in two forms: a one-time upfront guarantee fee of 1% of the loan amount and an annual fee of 0.35% of the loan amount.

The upfront guarantee fee is paid at closing and is typically financed into the loan.

The annual fee is calculated annually but paid monthly as part of your monthly mortgage payment. This fee is paid for the life of the loan.

The annual fee is distinct from PMI and serves as a protective measure for lenders against potential losses. PMI can be cancelled once sufficient equity is built, but the annual fee is paid for the life of the loan.