When an insurance company comes to a medical office, it can be for a variety of reasons. They may be requesting access to medical records, which is necessary for underwriting and claims processing, especially in the case of life insurance policies. This can be an invasion of privacy, as they often request records going back to the patient's birth, even if it is unrelated to the current claim. Another reason for their visit could be to authorize tests or medical procedures, which is a tactic used by insurance companies to control costs. This can cause delays in treatment and frustration among patients and doctors. In some cases, insurance companies may also deny claims, requiring the medical office to argue for coverage. This can be a result of bad faith denials or the insurance company practicing medicine without a license.

| Characteristics | Values |

|---|---|

| Access to medical records | A claims representative can access your medical records only if you give them permission. |

| Medical history | Insurance companies can request medical records going back to your birth, including information unrelated to your current claim. |

| Underwriting and claims processing | Medical records are necessary for underwriting and claims processing. |

| Premium rates | Medical records are used to determine premium rates, especially for life insurance. |

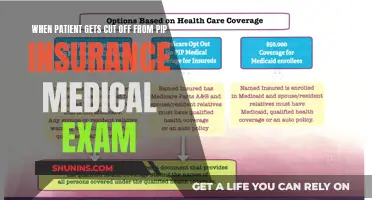

| Prior authorization | Insurance companies use prior authorization to control costs and limit the use of new treatments or medications. |

| Patient impact | The prior authorization process can delay necessary medical procedures and impact patient outcomes. |

| Denial of claims | Insurance companies may deny claims initially, requiring further conversation or argument for approval. |

Explore related products

What You'll Learn

![]()

Privacy concerns

In the United States, the Health Insurance Portability and Accountability Act (HIPAA) ensures that an individual's health information is protected and can only be accessed with their consent for treatment, payment, or healthcare operations. However, there is a risk of confidentiality breaches due to the HIPAA privacy rule allowing disclosure of Protected Health Information (PHI) without authorization in certain cases. This has led to concerns about insurance companies accessing medical records unrelated to the specific injury or claim. For instance, insurance companies often request medical records going back decades, even to the patient's birth, which is an invasion of privacy.

To address these concerns, patients should be aware of their rights under HIPAA and carefully review any authorizations they provide to insurance companies. Patients have the right to restrict disclosure of their health information if they believe it could jeopardize their safety or in cases of sensitive services. Additionally, patients can safeguard their health insurance records by regularly checking for errors, understanding what information is shared, and being cautious about sharing personal information.

It is important to note that insurance companies can access medical records with patient consent, which is typically provided when signing a life insurance application or authorization form. This consent allows insurance companies to request medical records from any doctor and obtain information on medical care and history. Therefore, patients should be mindful of what they authorize and only provide access to relevant medical records that explain their injury and treatment.

Medicaid Eligibility: Subsidies for Health Insurance Coverage?

You may want to see also

Explore related products

![]()

Patient consent

Patients should be aware that they are not obliged to share their medical records with an insurance provider that is not their own. Additionally, they have the right to privacy regarding their healthcare information, protected by the Health Insurance Portability and Accountability Act (HIPAA). This means that without the patient's written consent, their medical information cannot be disclosed to anyone except those they choose to share it with.

When presented with a medical authorization form, patients should refrain from signing it until they have consulted a lawyer. These forms often grant the insurance company access to the patient's entire medical history, which may be unrelated to the injuries being claimed. Patients should carefully review the form and understand the extent of the information they are disclosing. In some cases, insurance companies may request medical records that go back decades, even to the patient's birth, which is far beyond what is necessary for the current claim.

It is advisable for patients to seek legal representation when dealing with insurance companies. Lawyers can help protect the patient's interests and ensure they are not taken advantage of. They can review the authorization forms, explain the permissions granted, and guide patients on what information they are required to disclose. By understanding their rights and seeking legal advice, patients can make informed decisions about consenting to the release of their medical records to insurance companies.

Life Insurance Without a Medical Exam: Is It Possible?

You may want to see also

Explore related products

![CPC Exam Prep + Medical Billing & Coding + Medical Terminology [3-IN-1]: The Unfair Advantage Career System: Pass the Exam & Get Hired | Exam Simulator, ATS Resume & Interview Kit + Custom AI Coach](https://m.media-amazon.com/images/I/61rrA2UQUaL._AC_UL320_.jpg)

![]()

Insurance company's access to medical records

When an individual is applying for health or life insurance, the insurance company may request some information to determine their eligibility for coverage. This does not extend to their entire medical history, but insurance companies can gain access to medical records in certain circumstances.

According to the Department of Health and Human Services, a medical provider may share an individual's medical information with another medical professional "only as needed for treatment" or if the patient provides permission in writing. Written permission is not required if the sharing of medical records is related to the patient's treatment. For example, if a patient needs to see a specialist or is changing their primary care doctor, they may be asked to fill out a form to request a records transfer.

In the case of an accident, an insurance company may try to access an individual's medical records to determine the value of a claim and find reasons to deny it. However, there are limits to the access that must be granted. Typically, an insurance company will only need to view records of treatment received for the injuries in question. It is not uncommon, however, for adjusters to attempt to access past medical records to gain an advantage in a case.

When an individual is representing themselves, they should not sign anything until they have read and understood it. While insurance companies are entitled to relevant medical records that explain an individual's injury and treatment, it is not necessary for them to access records from years or decades prior that are unrelated to the current claim.

To protect their rights, individuals should be cautious about what records they release and can seek legal advice before signing any authorisation forms.

Understanding Pharmacy Services on Your Medical Insurance Bill

You may want to see also

Explore related products

![]()

Prior authorization

The prior authorization process can be frustrating for both doctors and patients, as it delays care and increases the risk of bad outcomes and hospitalization. Physicians must fill out extensive paperwork, and insurance companies often take their time to respond. This can result in patients not picking up their medications or receiving timely treatment.

To initiate the prior authorization process, patients should ask their healthcare provider if a prescription or treatment requires prior authorization. The provider will then give the necessary information to the insurance company, which will decide whether or not to cover the treatment or medication. If prior authorization is denied, patients can submit an appeal, which is more successful when the provider deems the treatment medically necessary or there was a clerical error.

Medically Needy: Is It a Health Insurance Alternative?

You may want to see also

Explore related products

![]()

Patient's rights

Patients have a number of rights when dealing with insurance companies and medical offices. When an insurance company requests medical records, patients have the right to deny access to their doctor or medical records. Patients are also not required to sign any documents they do not understand or agree with. While insurance companies are entitled to relevant medical records that explain a patient's injury and treatment, they are not entitled to a patient's entire medical history.

Patients also have rights regarding billing and payment. If a patient's health insurance covers emergency care, they cannot be charged more for emergency medical services than the in-network "cost-sharing" rate. This includes post-stabilization services in most cases. However, ground ambulance services are typically not covered by billing protections in the No Surprises Act and may charge out-of-network rates. Patients also have the option to give up protections and pay more for out-of-network care. Additionally, patients have the right to receive a good faith estimate of the cost of care if they do not have or use health insurance. They may be able to dispute their bill if it is significantly higher than the estimate.

In terms of treatment, HMOs and insurers cannot prohibit or restrict a provider from advocating on behalf of a patient for coverage of a particular treatment. However, prior authorization from an insurer may be required for certain tests, procedures, or medications, which can cause delays in treatment.

Understanding Your Family's Medical Insurance Deductible

You may want to see also

Frequently asked questions

Doctors often have to argue with insurance companies to get treatments covered due to bad faith denials based on in-house doctors determining medical necessity without seeing the patient.

Insurance companies request extensive medical records to find pre-existing conditions to blame your current complaints on. They are only entitled to relevant medical records that explain your injury and treatment.

Prior authorization is when insurance companies require authorization before covering the cost of a test or medical procedure. Insurance companies use this tactic to control costs.

Insurance companies can access medical records with patient consent, which is necessary for underwriting and claims processing.

It depends on your health plan. Some health plans do not cover emergency care.