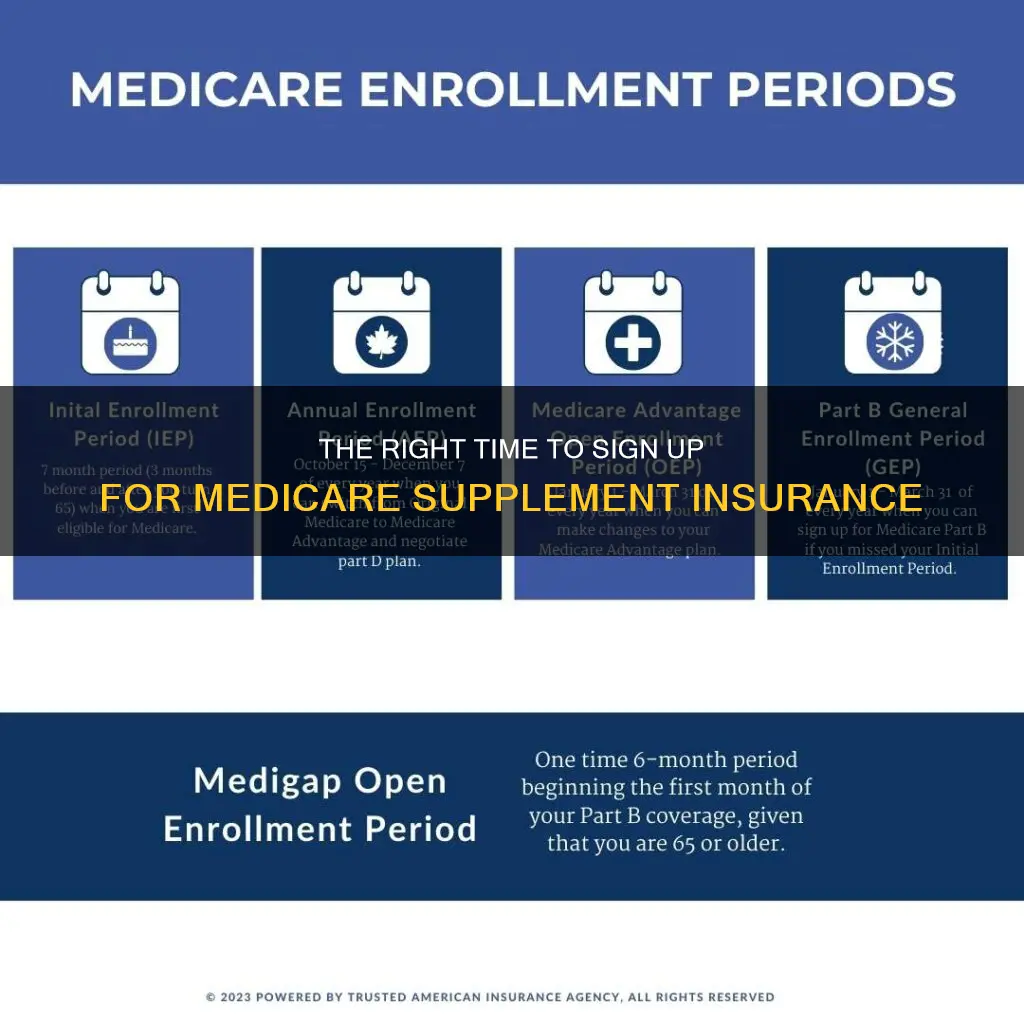

Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that can be purchased from a private insurance company to help cover out-of-pocket costs in Original Medicare. The best time to buy a Medigap policy is during the one-time, six-month Medigap Open Enrollment Period, which begins the first month an individual is 65 or older and has enrolled in Medicare Part B. During this period, individuals can enroll in any Medigap policy, and insurance companies cannot deny coverage based on pre-existing health conditions. After this period, Medigap policies may be more difficult to obtain and more expensive. Therefore, it is generally recommended to enroll in Medicare Supplement Insurance during the Medigap Open Enrollment Period to avoid penalties and ensure continuous coverage.

| Characteristics | Values |

|---|---|

| Best time to buy a Medicare Supplement Insurance policy | During your Medigap Open Enrollment Period |

| When does the Medigap Open Enrollment Period start | The first month you have Medicare Part B and you're 65 or older |

| How long does the Medigap Open Enrollment Period last | 6 months |

| What happens if you don't buy a policy during the Medigap Open Enrollment Period | Your options to buy a Medigap policy may be limited and the policy may cost more |

| What happens if you don't sign up for Medicare when you're first eligible | You'll have to wait to sign up and go months without coverage, and you might pay a monthly penalty for as long as you have Part B |

| What is Medicare Supplement Insurance | Extra insurance you can buy from a private insurance company to help pay your share of out-of-pocket costs in Original Medicare |

| What is covered by Medicare Supplement Insurance | All Medigap policies are standardized. This means policies with the same letter offer the same basic benefits no matter where you live or which insurance company you buy the policy from |

| How to buy a Medigap policy | Compare the benefits of each lettered plan, decide which benefits you need, and select the plan that meets your needs. You can buy a Medigap policy from any insurance company licensed in your state to sell one |

| How to find out if you qualify for a Medigap policy | Call your State Health Insurance Assistance Program |

Explore related products

What You'll Learn

![]()

During your Medigap Open Enrollment Period

During this time, you will generally get better prices and more choices among policies. You can avoid or shorten waiting periods for a pre-existing condition if you buy a Medigap policy to replace creditable coverage. An insurance company cannot use medical underwriting to decide whether to accept your application—they cannot deny you coverage due to pre-existing health problems.

After this period, your options to buy a Medigap policy may be limited, and the policy may cost more. Insurance companies do not have to sell you a Medigap policy, except in specific circumstances. If you qualify, you will need to give the company proof of your situation.

To buy a Medigap policy, you will need to:

- Compare the benefits of each lettered plan.

- Think about your current and future healthcare needs.

- Decide which benefits you'll need.

- Remember, you might not be able to switch policies later.

- Select the plan that meets your needs.

- Find insurance companies selling the plan you want.

- Remember, not all plans are offered in every state, and if a state offers a plan, not all insurance companies sell policies for it.

- Contact more than one company that sells Medigap policies in your state to get an estimate.

- Contact your local State Health Insurance Assistance Program (SHIP) to get free help choosing an insurance company in your area.

Get Your Medical Insurance Reinstated: A Comprehensive Guide

You may want to see also

Explore related products

![]()

If you lose your job-based coverage

If you lose your job-based health insurance, you can enroll in a Marketplace plan. You will qualify for a Special Enrollment Period to get coverage for the rest of the year. You need to apply within 60 days of losing your job-based coverage. Your coverage can start the first day of the month after you lose your job-based coverage.

You can also consider COBRA coverage, which lets you pay to stay on your job-based health insurance for a limited time after your job ends (usually 18 months). You usually pay the full premium yourself, plus a small administrative fee. However, you should not wait until your COBRA coverage ends to sign up for Medicare Part B, as COBRA coverage does not extend your limited time to sign up for Medicare.

If you have employer coverage when you become eligible for Medicare, you can delay enrolling in Medicare Part B without incurring penalties, as long as your employer insurance qualifies as "creditable coverage". Once you lose your employer coverage, you can enroll in Medicare Part B during a Special Enrollment Period without facing late enrollment penalties. This period typically lasts for eight months after your coverage ends, and you will need to coordinate the timing of your Medicare Part B enrollment with the end of your employer coverage to ensure uninterrupted healthcare benefits.

If you have retiree coverage from a previous job, it may not pay for your health services if you don't have both Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). You should check with your benefits administrator about how your retiree coverage works with Medicare.

If you have employer coverage, it may provide coverage similar to Medigap, so you probably don't need to get a Medigap policy. However, once you lose your employer coverage, you will have 63 days to select a Medigap policy and have guaranteed issue rights.

Medical vs Prescription Insurance: What's the Difference?

You may want to see also

Explore related products

![]()

When you're first eligible

Most people sign up for Medicare Supplement Insurance (also known as Medigap) when they are first eligible, which is usually when they turn 65. This is because there are risks to signing up later, such as a gap in your coverage or having to pay a penalty. The monthly penalty for Part B goes up the longer you wait to sign up.

Your Medigap Open Enrollment Period starts when you sign up for Part B and lasts for 6 months. During this time, you can enroll in any Medigap policy, and insurance companies cannot deny you coverage due to pre-existing health problems. After this period, your options to buy a Medigap policy may be limited, and the policy may cost more. Therefore, it is recommended that you buy a Medigap policy during your Medigap Open Enrollment Period.

To prepare for buying a Medigap policy, you should compare the benefits of each lettered plan and decide which benefits you need. All Medigap policies are standardized, meaning that policies with the same letter offer the same basic benefits, regardless of the insurance company. The price is the only difference between policies with the same letter sold by different companies, and costs can vary widely. You can contact your local State Health Insurance Assistance Program (SHIP) to get free help in choosing an insurance company in your area. Once you have chosen a plan, you can select "Enroll" at Medicare.gov/plan-compare or contact the plan to join.

Best Medical Insurance for Unskilled Workers: Company Comparison

You may want to see also

Explore related products

![]()

If you have a disability or ESRD

If you have a disability or End-Stage Renal Disease (ESRD), you may be eligible for Medicare before the age of 65. The best time to sign up for Medicare Supplement Insurance, also known as Medigap, is during your Medicare Supplement Open Enrollment Period, which starts on the first day of the month you're both 65 or older and enrolled in Medicare Part B. However, for those with disabilities or ESRD, there are specific considerations to keep in mind.

For individuals with a disability, you may be eligible for Medicare before turning 65 if you receive Social Security Disability Insurance (SSDI) payments for a certain amount of time. Once you receive SSDI benefits for 24 months continuously, you will automatically qualify for Medicare in the 25th month. This is true regardless of your age. During this initial enrollment period, you can sign up for Medicare Parts A and B, and you also have the option to enroll in a Medicare Supplement plan.

If you have ESRD, your Medicare options are a bit different. ESRD is life-threatening kidney failure that requires dialysis or a kidney transplant. If you're diagnosed with ESRD and meet certain requirements, you may be eligible for Medicare at any age. The first month after you begin dialysis or have a kidney transplant, you'll have a chance to enroll in Medicare Parts A and B. You can also sign up for a Medicare Supplement plan during this initial enrollment period.

It's important to note that Medicare Supplement plans are sold by private insurance companies, and the availability and pricing of these plans can vary depending on your location and the insurance company. During your initial enrollment period, you have guaranteed-issue rights to buy a Medicare Supplement plan, and insurance companies cannot deny you coverage or charge you more based on your health status. This makes it crucial to enroll during this period if you think you may need a Medicare Supplement plan to help cover the costs that original Medicare doesn't cover.

If you miss your initial enrollment period for Medicare Supplement Insurance, you may still have opportunities to enroll later, but you might face medical underwriting, which could affect your acceptance and the cost of your plan. These additional enrollment periods include the Annual Election Period (AEP), also known as Open Enrollment Period (OEP), and your birthday month. However, enrolling during these periods may be more restrictive, and you might have to answer health questions or undergo medical exams. So, it's always best to enroll during your initial enrollment period if possible.

Ohio Medical Billing: Understanding Balance Billing and Insurance

You may want to see also

Explore related products

![]()

If you qualify for guaranteed issue rights

There are several situations in which you may qualify for guaranteed issue rights. One common scenario is when you experience a loss of coverage. This could include losing your employer-sponsored retiree plan, COBRA coverage, or union coverage. In some states, losing Medicaid due to a change in financial circumstances also qualifies for guaranteed issue rights. It is important to note that the loss of coverage must be involuntary in some states to qualify for guaranteed issue rights.

Another situation that triggers guaranteed issue rights is when there are changes to your Medicare Advantage plan. If you enroll in a Medicare Advantage plan at age 65, you have the right to change your mind within 12 months. If you decide to switch back to Original Medicare, you can purchase a Medicare supplement, and the insurance company is obligated to accept your application. Similar trial rights exist if you switch to a Medicare Advantage plan after turning 65 or if you move out of your plan's service area.

To take advantage of guaranteed issue rights, it is important to act promptly. In most cases, you have up to 63 days from the date your previous coverage ends to elect a new plan under guaranteed issue rights. Additionally, it is crucial to gather the necessary documentation, including your Medicare card, identification, and any correspondence related to your Medicare enrollment or previous coverage. Understanding the specific rules and plans available in your state is also essential, as guaranteed issue rights and Medigap plans can vary across states.

By understanding your guaranteed issue rights and the available Medigap plans, you can ensure that you secure the coverage you need without worrying about medical underwriting or variations in benefits. Remember to review the costs, benefits, and network restrictions associated with each plan to make an informed decision that best suits your healthcare needs and financial situation.

Best Medical Insurance Company in Kerala: Your Guide

You may want to see also

Frequently asked questions

The best time to buy a Medicare Supplement Insurance (Medigap) policy is during your Medigap Open Enrollment Period. This is a one-time, 6-month enrollment period that starts the first month you have Medicare Part B and are 65 or older.

After your Medigap Open Enrollment Period ends, insurance companies are not obligated to sell you a Medigap policy, and your options may be limited and more expensive. However, there are certain situations where you may be able to buy a Medigap policy outside of this period, known as "guaranteed issue rights" or "Medigap protections."

The benefits in each lettered plan are the same, regardless of the insurance company. The price is the only difference between policies with the same letter sold by different companies, so it is important to shop around and compare prices. You should also carefully review the summary of your Medigap policy and keep it for your records.

If you are under 65 and have Medicare due to a disability or ESRD, you may not be able to buy a Medigap policy until you turn 65. Federal law generally does not require insurance companies to sell Medigap policies to people under 65, but some states do offer these policies. Check with your State Insurance Department for more information.

If you lose your job-based health coverage before you or your spouse stop working, you have 8 months to sign up for Medicare. If you want your Medicare coverage to start immediately after your job-based health insurance ends, you need to sign up for Part B the month before you retire.