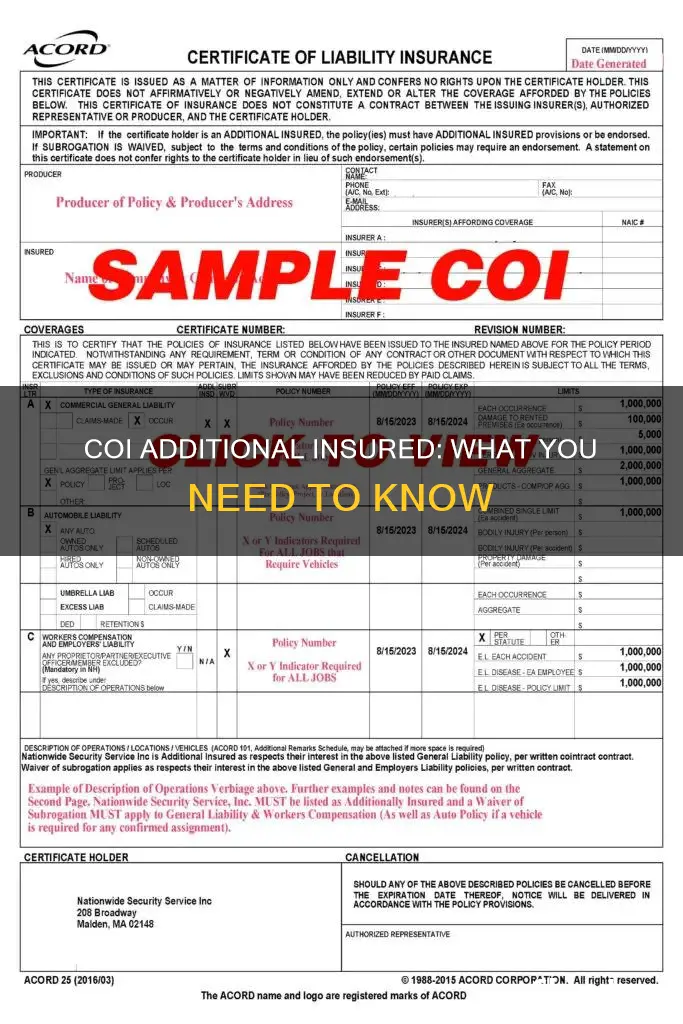

An additional insured endorsement extends the coverage of a liability insurance policy beyond the named insured to include other individuals or groups not initially named in the original policy. This means that the additional insured can make a claim on the policyholder's policy if they are sued for the policyholder's actions. On a Certificate of Insurance (COI), additional insured entities are indicated by an 'X' or checkmark in the 'ADDL INSR' box in the Certificate Holder section of the document.

| Characteristics | Values |

|---|---|

| Definition | Additional insured is a type of status associated with general liability insurance that provides coverage to other individuals/groups not initially named. |

| Who can be an additional insured? | An additional insured can be an individual or a company that has a vested interest in your business. |

| Rights | Additional insured entities have the right to file a claim under the policy. |

| Cost | The cost of adding an additional insured is typically low compared to the costs of the premium. |

| Where on COI | Additional insured entities are indicated by an X or checkmark in the ADDL INSR box on the General Liability section of the COI. |

Explore related products

What You'll Learn

![]()

Additional insured status and its benefits

Additional insured status is associated with general liability insurance. It provides coverage to individuals or groups not initially named in the original policy. This means that if a third party sues the additional insured, the policyholder can address the claim, covering legal defence fees, court fees, and settlement or judgment costs.

The additional insured can be indicated on a Certificate of Insurance (COI) with an X or checkmark in the 'ADDL INSR' box on the General Liability section. A certificate holder can request to be an additional insured on the policyholder's COI, which would show that they benefit from the coverage of another's policy. This is a common practice, especially for smaller companies working with larger businesses, as it reduces the loss history of the additional insured, leading to lower premiums.

However, it is important to note that there is debate about the extent of coverage an additional insured receives. Disagreements often arise over whether the additional insurance covers only liabilities caused by the named insured's acts or also includes "independent negligence" by the additional insured. Therefore, it is crucial to understand the terms of the insurance policy and any endorsements or amendments made to it.

Overall, additional insured status provides benefits such as protection from third-party claims, reduced costs for the additional insured, and assurance for companies working with contractors that they have the means to compensate in the worst-case scenario.

Leasing a Financed Car: How Does Insurance Work?

You may want to see also

Explore related products

![]()

Adding an additional insured to a policy

An additional insured endorsement allows the primary policyholder to add another insured party to their policy. This endorsement typically applies to general liability insurance policies, but can also be added to commercial property or commercial auto policies. It is usually a low-cost addition, as insurers consider the additional risk marginal.

The additional insured benefits from the coverage of the primary policyholder's policy and can make claims under it. This is particularly useful in the case of a lawsuit, as the financial responsibility of the claim is placed on the party that is most likely to be responsible. For example, if a business owner hires a contractor who causes an accident, the business owner can make a claim under the contractor's policy if they are named as an additional insured.

There are two types of additional insured endorsements: a blanket endorsement and a standard endorsement. A blanket endorsement provides the same coverage to a group of people who are not specifically named, such as drivers or subcontractors. A standard endorsement, on the other hand, requires the additional insured party to be named specifically on the policy.

When adding an additional insured to a policy, it is important to note that they may not have the exact same coverage and benefits as the primary policyholder. The amount of coverage the additional insured receives depends on how the policy is written. It is also important to understand the difference between a certificate holder and an additional insured. A certificate holder is simply someone who receives a copy of the policyholder's certificate of insurance (COI) and is notified of any changes or cancellations. They are not authorized to make a claim under the policy.

Overall, adding an additional insured to a policy can be a useful way to manage risk and ensure that all necessary parties are covered in the event of a claim or lawsuit.

How Insurance Choice Affects Your UCAS Application

You may want to see also

Explore related products

![]()

The difference between a certificate holder and an additional insured

An additional insured endorsement is a type of status associated with general liability insurance that provides coverage to other individuals or groups not initially named. This endorsement protects the additional insured under the named insurer's policy, allowing them to file a claim if sued. For example, a general contractor might require subcontractors to name the general and the owner on the subcontractor's policies.

A certificate holder, on the other hand, is an entity that holds proof of insurance, or a Certificate of Insurance (COI), from the insured party they are working with. This certificate verifies that the insured party has the required coverage. The certificate holder is usually listed on the COI and will receive notifications of any changes, renewals, or cancellations. However, they are not authorized to make claims under the policy and do not have the same protection as an additional insured.

The main difference between a certificate holder and an additional insured is that the latter has coverage extended to them through the named insured's policy and can file claims. The certificate holder only receives verification of insurance and notifications but is not covered by the policy. This distinction is critical for businesses to understand to ensure they have adequate protection from claims.

Adding an additional insured to a policy typically incurs a low cost, as insurers consider the additional risk marginal. However, there may be disagreements about the extent of coverage for the additional insured, specifically whether it covers only liabilities caused by the named insured or also includes independent negligence. A certificate holder can request to be added as an additional insured on the COI, which would provide them with the rights and protection of an insured party.

In summary, understanding the difference between a certificate holder and an additional insured is crucial for businesses to ensure proper coverage and protection from claims. An additional insured has extended coverage and can file claims, while a certificate holder only receives verification of insurance and notifications but has no coverage or rights under the policy.

Uninsured Motorist Insurance: Is It Necessary?

You may want to see also

Explore related products

![]()

Additional insured endorsements

An additional insured endorsement is an addendum to an insurance policy that extends or restricts coverage to a third party identified by the policyholder in the event of a claim or negligent act. This third party is known as the additional insured.

The additional insured typically has some degree of liability due to their relationship with the named insured. They benefit from the coverage of the named insured's policy, including the ability to make claims under the policy. This means that if the additional insured is sued for the actions of the named insured, the insurance policy of the named insured will pay out for any claims or damages.

There are two main types of additional insured endorsements: blanket additional insured endorsements and standard additional insured endorsements. A blanket additional insured endorsement provides the same coverage to a group of people who aren't required to be specifically named, such as drivers or subcontractors. On the other hand, a standard additional insured endorsement requires the parties to be named specifically on the policy.

The cost of adding an additional insured is typically low compared to the cost of the premium. This is because insurance companies consider the additional risk associated with additional insureds as marginal. However, there are some limitations and potential pitfalls to be aware of when it comes to additional insured endorsements. For example, the endorsement may only cover a limited type of liability, or it may restrict coverage to ongoing operations, leaving the additional insured vulnerable to liability for incidents that occur after the work is complete.

It is important to carefully review the language of the endorsement to ensure it accurately reflects the desired coverage and contractual requirements. Submitting the incorrect form could result in a lapse in coverage. For example, if an endorsement only covers ongoing operations and a claim arises after the project is completed, the insurer would not cover the claim.

Signaling Fails: Insurance Impact of Traffic Citations

You may want to see also

Explore related products

![]()

Cost of adding an additional insured

An Additional Insured (AI) is someone who is added to an existing business insurance policy. This addition extends the insurance coverage to another person or company, providing them with two valuable kinds of protection. Firstly, if someone sues the AI for something covered by the insurance, the policy steps in to defend them. Secondly, the policy will pay on behalf of the AI for someone else's medical bills or property damage.

The cost of adding an additional insured depends on the insurance provider and the type of insurance. Some insurers charge a flat rate for adding as many additional insureds as desired, while others charge per additional insured, with prices starting at $25. Generally, adding endorsements increases the cost of business insurance. However, the additional cost is usually low compared to the premium costs.

A larger business may require smaller operations to name them as an additional insured. For example, a landlord may require a tenant to name them as an additional insured on their insurance policies. This arrangement leverages the larger business's bargaining power, as the smaller company wants to do business with them.

Before adding an additional insured, it is essential to understand how it will affect the premium. It is recommended to consult a broker or licensed insurance agent to determine the specific costs and coverage details.

Skydiving: Does This Extreme Sport Increase Your Insurance Rates?

You may want to see also

Frequently asked questions

An additional insured is an individual or business that the policyholder adds to an insurance policy, entitling them to the same coverage benefits.

Being an additional insured means being protected and defended when the primary insured is negligent. It does not insure them for their negligence but for their liability arising from the primary insured's negligence.

A certificate holder is a third party that may be named on a COI. They receive verification of insurance and notifications of any changes made to a policy but are not covered by the policy and cannot file a claim. An additional insured, on the other hand, has the right to file a claim.

To add an additional insured endorsement to your policy, talk to your insurance agent about your existing policy and any limitations that come with the endorsement. File the proper forms and paperwork, and your updated certificate of liability insurance will list the new additional insured.

Once you add an additional insured to your policy, send out the updated COI with the additional insured endorsement attached. The COI will list additional insured entities in the Certificate Holder section, with a check or X next to "ADDL INSR".