When it comes to insurance and taxes, it's essential to understand how to report insurance premiums and claims on your IRS Form 1040 to maximize your deductions and remain compliant. While money received from insurance claims or settlements is typically not taxed, as it aims to restore your financial state after an incident, there are instances where certain types of payouts may be taxable. For example, if you receive money for medical bills after a car accident, it isn't taxed, but punitive damages from a lawsuit might be. Similarly, if you itemize deductions, health insurance premiums can be reported as medical expenses on Schedule A of Form 1040, but specific criteria must be met. For self-employed individuals, accurately reporting health insurance costs is crucial for maximizing deductions, and understanding the implications of insurance purchased through the Marketplace is also important.

| Characteristics | Values |

|---|---|

| Reporting insurance premiums on Form 1040 | Can be crucial for maximizing tax deductions |

| Health insurance premiums | Can be reported as part of medical expenses on Schedule A of Form 1040 |

| Line on Schedule A for health insurance premiums | Line 1 |

| Criteria for reporting health insurance premiums on Schedule A | Must itemize deductions instead of taking the standard deduction; total medical expenses must exceed 7.5% of AGI for the year |

| Reporting health insurance premiums for self-employed individuals | Can deduct health insurance premiums directly from taxable income |

| Reporting health insurance premiums with premium tax credits | Cannot include the amount of the premium tax credit in medical expenses |

| Reporting health insurance premiums purchased through the Marketplace | Must complete Form 1095-A and Form 8962 |

| Reporting sick pay from employer | Report on line "Total amount from Form(s) W-2, box 1" on Form 1040 or 1040-SR |

| Reporting insurance claim or settlement payments | Generally not taxed unless it results in more wealth than before the incident |

| Reporting taxable lawsuit payments | Report using Form 1099 |

| Reporting medical claim payments | Not taxed |

Explore related products

What You'll Learn

- Health insurance premiums can be reported as part of medical expenses on Schedule A

- Self-employed individuals should report health insurance costs accurately to maximise deductions

- If you receive taxable payment from a lawsuit, you will receive a 1099 form

- If you receive sick pay, you can submit a Form W-4S to the insurance company

- If you have insurance through the Marketplace, reporting premiums involves additional steps

![]()

Health insurance premiums can be reported as part of medical expenses on Schedule A

When it comes to insurance payments and tax returns, there are a few things to keep in mind. Firstly, money received as part of an insurance claim or settlement is typically not taxed, as the IRS only levies taxes on income, which is money that increases your wealth. Insurance payouts are meant to "make you whole" and bring you back to the state you were in before an incident. However, certain types of insurance payouts may be taxable, such as short- and long-term disability insurance proceeds, which are taxed as income. If your insurance claim has resulted in a lawsuit, the tax situation can become more complex, with some payouts being taxable and others, such as compensation for medical bills, being non-taxable.

Now, regarding where insurance payments fit into the 1040 form, it depends on the nature of the insurance and the specific circumstances. For example, if you are reporting medical and dental expenses, you would refer to Schedule A of Form 1040. This includes health insurance premiums, which can be included in medical expenses. If you are self-employed and have health insurance, you can deduct expenses for yourself, your spouse, dependents, and children under 27 at the end of the tax year. If you are a federal employee with health insurance through the Federal Employee Health Benefits (FEHB) program, you cannot deduct premiums paid with pre-tax money.

Additionally, if you are itemizing deductions on Schedule A of Form 1040, you may be able to deduct medical and dental expenses for yourself, your spouse, and your dependents, provided they exceed 7.5% of your adjusted gross income for the year. This includes unreimbursed out-of-pocket healthcare costs. It's important to note that certain expenses are not deductible, such as funeral expenses, non-prescription medicines, and toiletries.

While health insurance premiums can be reported as part of medical expenses on Schedule A, auto and home insurance deductions are a bit more complicated. To deduct these expenses, you must itemize and fill out Form 1040, not the abbreviated versions. Additionally, you would need to file Schedule C Profit or Loss From Business. There is a simplified method for deducting auto insurance costs, which is 54 cents per mile, designed to cover payments, fuel, repairs, depreciation, maintenance, and insurance.

Navigating Insurance: Out-of-Network: What to Expect

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![]()

Self-employed individuals should report health insurance costs accurately to maximise deductions

Self-employed individuals can purchase a health insurance policy in their name or their business's name to qualify for the self-employed health insurance deduction. This deduction is applied on a month-to-month basis, and it is adjusted to their gross income on Schedule 1 of Form 1040. Self-employed individuals can deduct premiums for medical, dental, and qualifying long-term care insurance coverage for themselves, their spouses, and their dependents.

To calculate the deduction, one must first determine their total annual health insurance premiums paid for coverage that qualifies under IRS rules. This includes medical, dental, and long-term care coverage. Once this figure is calculated, it must be compared to the net profit from self-employment. The deduction is generally limited to the amount of net profit, and any excess premiums cannot be deducted. For example, if an individual has a net profit of $80,000 and paid $9,000 in health insurance premiums, their deduction is limited to $80,000.

Additionally, transportation costs to medical facilities for check-ups, tests, prescription refills, and other healthcare-related activities can also be deducted. Other deductible necessities include insulin, wheelchairs, hearing aids, and crutches.

It is important to note that the rules and limitations surrounding self-employed health insurance deductions can be complex and may vary depending on individual circumstances. Consulting with a tax professional or utilizing tax software can help ensure accurate calculations and compliance with IRS regulations.

Farmers Insurance: Will Policyholders Get Refunds?

You may want to see also

Explore related products

![]()

If you receive taxable payment from a lawsuit, you will receive a 1099 form

Generally, money received as part of an insurance claim or settlement is not taxed, as it is not considered income by the IRS. However, if your insurance claim has evolved into a lawsuit, you may receive several different forms of compensation, some of which may be taxable. For example, punitive damages awarded by a judge in a car accident case are taxable, whereas payments for medical bills are not.

If you receive a taxable payment from a lawsuit, you will likely receive a 1099 form to help you file your taxes. This form is used to report income and match it with your Social Security number. Most settlements are reported on 1099 forms, and defendants or insurance companies issuing taxable settlement payments are required to provide them. However, there are exceptions, and not all taxable lawsuit payments require a 1099 form. For example, if you receive a settlement for lost wages, it may be reported on a W-2 form instead.

It's important to note that the taxability of lawsuit settlements depends on the specific circumstances and the purpose of the payment. While compensation for lost wages and damages, including wrongful termination, is generally taxable, payments for personal injuries, certain discrimination claims, and physical injuries are usually not. Additionally, if you receive payments from your employer while sick or injured, you can report them on Form 1040 and may be able to exclude certain payments received under life insurance contracts for terminally or chronically ill individuals.

To maximize your deductions when filing taxes, you may need to itemize and fill out Form 1040, Schedule C (Profit or Loss from Business), and calculate your insurance premiums using either the simplified method or your actual insurance expenditure. Consulting official IRS sources or a tax professional can provide specific guidance on reporting taxable lawsuit payments and maximizing deductions.

Kaiser Insurance: Which Hospitals Can I Attend?

You may want to see also

Explore related products

![]()

If you receive sick pay, you can submit a Form W-4S to the insurance company

If you receive sick pay, you can submit a Form W-4S, Request for Federal Income Tax Withholding From Sick Pay, to your insurance company. This form is used to request federal income tax withholding from your sick pay payments. It is particularly important if you are receiving benefits from sources other than your employer, such as insurance companies. By submitting Form W-4S, you can ensure that the correct amount of tax is withheld from your sick pay.

To fill out Form W-4S, you will need to provide your personal information, including your name, address, and Social Security number. You will also need to indicate the amount of federal income tax you wish to have withheld from each sick pay payment. Additionally, you must complete a worksheet to estimate your withholding based on your expected income and deductions. Signing the form validates your request. It is recommended that you submit Form W-4S as early as possible, ideally before you start receiving sick pay, to ensure accurate tax withholding.

It's important to note that money received as part of an insurance claim or settlement is typically not taxed. This is because the purpose of insurance is to "make you whole," meaning you should only receive enough payment to restore your previous state before an incident occurred. However, certain types of insurance payouts may be taxable. For example, short- and long-term disability insurance proceeds are taxed as income. If your insurance claim has resulted in a lawsuit, the tax implications can become more complex, and you may receive different forms of compensation taxed in different ways.

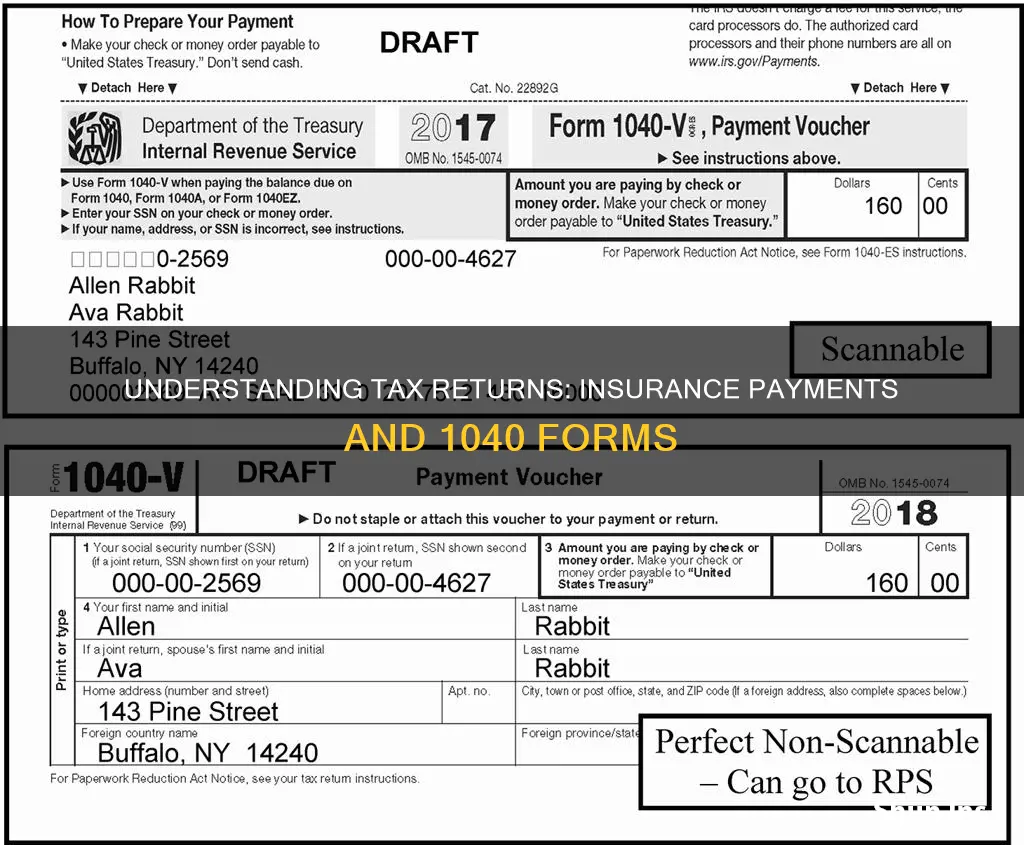

When it comes to reporting insurance payments on your taxes, you may need to fill out Form 1040, U.S. Individual Income Tax Return. This form allows you to report various sources of income and deductions. While insurance payments may not always be taxable, it's important to understand the specific circumstances and seek appropriate tax advice to ensure accurate reporting and compliance with tax laws.

Secondary Insurance: Back-up Coverage

You may want to see also

Explore related products

![]()

If you have insurance through the Marketplace, reporting premiums involves additional steps

If you have insurance through the Health Insurance Marketplace, you should receive a Form 1095-A, Health Insurance Marketplace Statement, at the beginning of the tax-filing season. Form 1095-A will tell you the dates of coverage, the total amount of your monthly premiums, the second lowest cost silver plan premium that you may use to determine the amount of your premium tax credit, and the amounts of advance payments of the premium tax credit.

If you chose to have advance payments of the premium tax credit paid directly to your insurance company, you must complete Form 8962, Premium Tax Credit, and file a federal income tax return, even if you are otherwise not required to file. You are required to reconcile these payments with the premium tax credit you'll compute for your tax return. Even if you did not choose to receive advance payments, you must file a federal income tax return to claim the premium tax credit.

If you received more than one Form 1095-A from the same Marketplace that reports coverage for different months, you will enter the information for the corresponding month on Form 8962. If you received more than one Form 1095-A that reports coverage for the same month, refer to the instructions for Form 8962 for more information. You do not have to send your Form 1095-A to the IRS with your tax return when you file and claim the premium tax credit. However, using the information on your Form 1095-A, you must complete and file Form 8962, Premium Tax Credit.

If you enrolled in insurance coverage through the Marketplace, you should report any changes in your circumstances — like changes to your household income or family size — to the Marketplace when they happen. Changes in circumstances may affect your advance payments of the premium tax credit. When you report a change in circumstances, you may become eligible for a special enrollment period, which allows you to purchase health care insurance through the Marketplace outside of the open enrollment period.

Insurance Fraud: Jail Time and Consequences

You may want to see also

Frequently asked questions

Money received as part of an insurance claim or settlement is usually not taxed. However, income from certain types of claims may be taxable. For example, if you receive a payout from a lawsuit, you will likely need to pay taxes on punitive damages.

If you receive taxable payments from a lawsuit, you will likely receive a 1099 form to help you file your taxes. You will need to report these payments as earnings when filing.

Insurance premiums can be reported on Schedule A of Form 1040 as part of your medical expenses. You must itemize deductions and meet certain criteria to do this. Alternatively, if you are self-employed, you can deduct health insurance premiums directly from your taxable income.

If you purchased health insurance through the Marketplace, you will receive Form 1095-A, which provides information about your coverage and any advance payments of the premium tax credit. You will then need to report any applicable amounts from Form 8962 on Schedule A.

If you receive sick pay from your employer, you must report this on Form 1040. You can generally exclude from income payments received from qualified long-term care insurance contracts as reimbursement for medical expenses.