If you're wondering where to put medical insurance payments on your W-2 form, you should know that you only need to enter the amount you paid for health insurance premiums if you are a self-insured or self-funded employer. In this case, you will need to fill out Form 1095. Additionally, you can only deduct the amount you paid for medical care insurance if it exceeds your standard deduction. This information can be found in Box 12 of your W-2 form, with a specific code that indicates the type of medical insurance payment being reported.

| Characteristics | Values |

|---|---|

| Health insurance costs on W2 | Not listed automatically |

| Health insurance costs on W2 box 12 | Not listed automatically |

| Health insurance premiums paid | Not deductible automatically |

| Health care contributions on W2 | Include only the amount paid in the relevant year |

| Health care contributions on W2 for state | Same as above |

| Self-insured employers | Pay for medical claims directly instead of paying premiums to an insurance provider |

| Self-insured employers filing requirements | No need to file. The insurer files forms and provides statements to employees |

| Small businesses | Defined as those with fewer than 50 full-time employees |

| Minimum essential health coverage | Must be offered to at least 95% of full-time employees and their dependents |

Explore related products

![[50 Pack] LH Test Strips #MT-W2-S](https://m.media-amazon.com/images/I/71J9OkFOjyL._AC_UL320_.jpg)

![[100 Pack] LH Test Strips #MT-W2-S](https://m.media-amazon.com/images/I/71w09S23RyL._AC_UL320_.jpg)

![[75 Pack] LH Test Strips #MT-W2-S](https://m.media-amazon.com/images/I/71+rsQQs8uL._AC_UL320_.jpg)

What You'll Learn

![]()

Health insurance costs on W2

Health insurance costs are not listed on W2 forms. However, employers with 50 or more full-time employees or full-time equivalent employees (FTEs) must report health coverage information to the IRS and furnish statements to employees annually. This is done through the 1095 forms, which include 1095-B and 1095-C. Small employers that sponsor self-funded health plans are also required to report.

If you are an employee, you should only enter the amount that you paid for health insurance contributions in the previous year. Do not include any amounts that were covered by insurance or that are still outstanding. You can find this information by going to Federal > Deductions and Credits > Medical > Medical Expenses.

It is important to note that regular medical expenses are only deductible if you itemize them. Additionally, health insurance premiums paid are not automatically deductible. However, you may be able to subtract some of the cost of your medical care insurance. For example, if you are using FreeTaxUSA, there is a page about "Wisconsin Medical Care Insurance Subtraction" where you can enter the qualifying amount you paid for medical care insurance.

Employers may face penalties if they do not offer minimum essential health coverage to at least 95% of their full-time employees and their dependents. A second type of penalty may be triggered if the minimum essential coverage is offered but is not affordable or does not provide minimum value. To determine if the coverage is affordable, the premium for the lowest-cost, self-only minimum value coverage should be less than 9.02% of an employee's gross household income. There are three safe harbor tests to determine affordability: the Form W-2 Safe Harbor, the Rate of Pay Safe Harbor, and the Federal Poverty Line Safe Harbor.

Medical Insurance and Cyst Removal: What's Covered?

You may want to see also

Explore related products

![]()

W2 box requirements

W-2 forms are used by the Internal Revenue Service (IRS) for US tax filing. They are used to report an employee's income and wages for federal tax purposes. There are a number of boxes and codes on the form, which can be tricky to interpret.

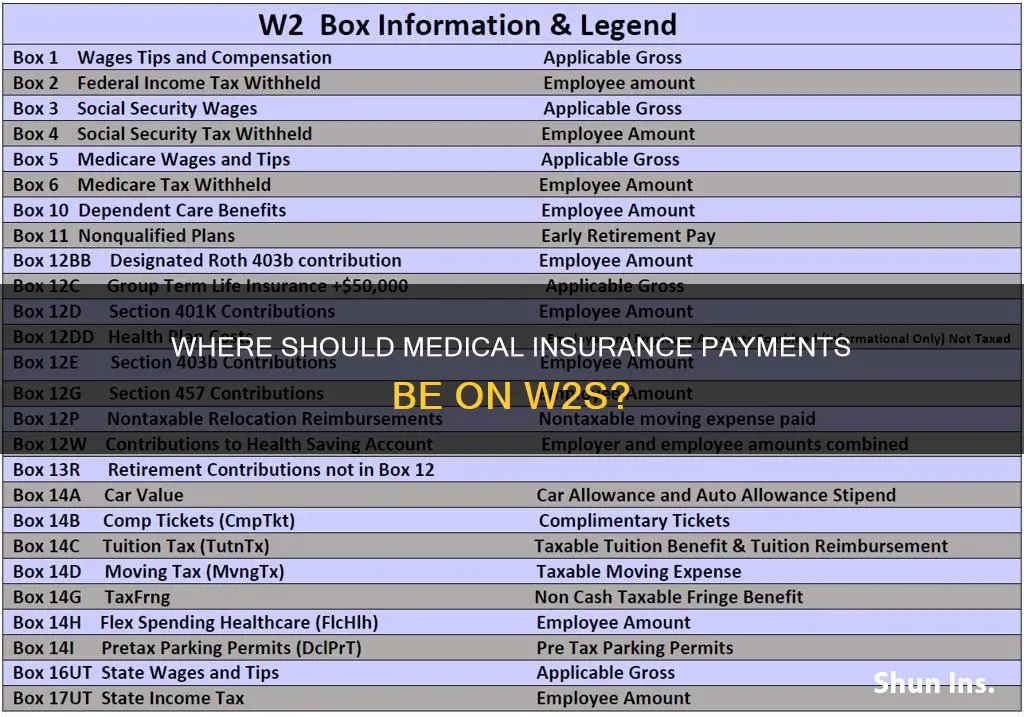

Box 12 is the one that often generates questions. It has a number of sub-categories, ranging from A to II, with 30 sub-boxes in total. The codes in this box provide more information to the IRS and determine if the amount is taxable income. For example, box 12 details important information like earnings, retirement plan contributions, employer contributions to health insurance, and other benefits like group term life insurance contributions.

If you are looking for medical insurance payments, you may find them in box 12 with the code DD. However, it is important to note that health insurance premiums paid are not automatically deductible. If the box is blank, it may be because the premiums are not taxable, rather than deductible.

Other boxes on the W-2 form include those for federal taxable wages, state and local taxes withheld, and Social Security and Medicare wages.

Medical Insurance Premium Deductions: What New Jersey Residents Should Know

You may want to see also

Explore related products

![]()

Employer-sponsored coverage

Employers with at least 50 full-time employees or full-time equivalents are mandated to provide health coverage to their workers. Applicable large employers (ALEs) that do not sponsor the required coverage may be penalised. Companies that sponsor employee coverage are required to report the cost of that coverage on W-2 forms.

Under the Affordable Care Act, most Americans must maintain a basic level of health insurance, referred to as minimum essential coverage. The Act requires employers to report the cost of coverage under an employer-sponsored group health plan on an employee's Form W-2, Wage and Tax Statement, in Box 12, using Code DD.

The amount reported includes both the employer and employee contributions. However, it does not affect tax liability, as the value of the employer's contribution is excludable from an employee's income and is not taxable. This information is included on the W-2 form to help employees understand the value of their coverage.

Although the Affordable Care Act requires reporting employer-sponsored coverage on W-2 forms, certain employers are eligible for transition relief from this requirement. This relief applies to the 2015 tax year and beyond until the IRS publishes additional guidance. Employers can refer to the "Optional Reporting" column in the IRS chart to determine if they are eligible for transition relief.

Medical Tourism Insurance: Protecting Your Health Abroad

You may want to see also

Explore related products

![]()

Self-insured employers

For self-insured employers, the reporting requirements for health insurance costs on an employee's W-2 depend on several factors, including the size of the company and the specific type of coverage provided. Here is some information on what self-insured employers need to know about reporting health insurance payments on their employees' W-2 forms:

Firstly, it's important to understand what constitutes employer-sponsored coverage. This includes any group health plan, including a self-insured plan, that is provided and funded in whole or in part by an employer or employee organization. It covers not only current employees but also former employees, the employer themselves, and their families. On-site medical clinics are also considered part of employer-sponsored coverage.

When it comes to reporting costs, self-insured employers have a few options. One method is the "premium charged" approach, which applies only to fully-insured plans and represents the actual premium charged by the insurer. Another method is the "modified COBRA premium" approach, where the employer subsidizes the cost of COBRA. If the actual premium charged by the employer is equal to the prior year's COBRA premium, the employer may use that amount as the reportable cost for the current year. Additionally, there is the "composite rate" method, where premiums are the same dollar amount regardless of the type of coverage elected by the employee.

It's worth noting that certain costs are exempt from reporting, such as those for on-site medical clinics, separate policies for dental or vision care, and coverage under a multi-employer plan. Additionally, if an employee works for more than one employer in a year, each employer is generally responsible for reporting their prorated cost of coverage on the employee's W-2.

In terms of deductibles and tax implications, health insurance premiums paid by employees are not automatically deductible. However, employees may be able to subtract some of these costs, depending on their specific circumstances and the applicable tax laws.

Texas Medical Insurance: What's Covered and What's Not?

You may want to see also

Explore related products

![]()

Healthcare coverage reporting requirements

The Affordable Care Act (ACA) requires employers to report the aggregate cost of employer-sponsored group health plan coverage on their employees' Forms W-2. This reporting requirement is applicable to employers that provide "'applicable employer-sponsored coverage'. This includes government entities, churches, and religious organizations, but does not include Indian tribal governments or tribally chartered corporations wholly owned by an Indian tribal government.

The purpose of this reporting requirement is to provide employees with information about how much their health coverage costs. It is important to note that the reporting of healthcare coverage on Form W-2 does not mean that the coverage is taxable. The value of the employer's contribution remains excludable from an employee's income and is not subject to tax.

The reporting requirement came into effect for the 2011 tax year, with the IRS making it optional for all employers for that year. From 2012 onwards, large employers (those filing 250 or more Forms W-2) were mandated to comply with the requirement, while small employers (filing fewer than 250 Forms W-2) were given the option to opt out. This distinction between large and small employers remains in place until further guidance is issued by the IRS.

The cost of healthcare coverage must be reported in Box 12 of Form W-2, using Code DD. However, it is important to note that individuals (employees) do not have to report the cost of coverage under an employer-sponsored group health plan. Additionally, contributions to Health Savings Arrangements (HSAs) are not reported in Box 12, Code DD, but certain HSA contributions are reported in Box 12, Code W.

Medical Insurance and Nursing Homes: What's Covered?

You may want to see also

Frequently asked questions

You should only enter the amount that you paid in the year prior—do not include any amounts that were covered by insurance or that are still outstanding.

If your employer is subject to the Affordable Care Act (ACA) reporting requirements, they must report health coverage information to the IRS and furnish statements to employees annually.

If your employer doesn't offer minimum essential health coverage to at least 95% of full-time employees and their dependents, they may be penalized.

Medical insurance premiums paid are not automatically deductible. However, you may be able to subtract some of the cost of your medical care insurance.

Regular medical expenses are only allowed if you itemize, but you may be able to deduct the premiums themselves that you paid.