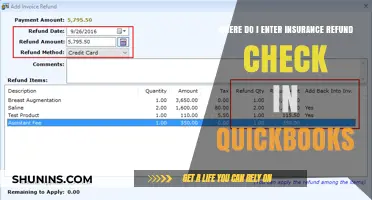

When receiving an insurance check, it is important to understand how to record it. One way is to create an Insurance Reimbursement Account and record repair bills as transfers from your checking or credit card account to the reimbursement account. Another method is to record the insurance reimbursements as credits in the expense category being used for the incident, which will then show the net cost.

Explore related products

What You'll Learn

![]()

Recording insurance claim payments

When recording insurance claim payments, it is important to match the insurance reimbursement with the costs incurred to fix or replace the property. This ensures that the payment is correctly categorised as a "reimbursement" rather than "income".

For example, reimbursements for automobile-related losses should be posted to the automobile "asset" account. If the vehicle is a total loss, and you buy a new one, the payment should be posted to the automobile "asset" account. If you buy a salvaged title, the payment should be posted to the same account/category that you used when you posted the repairs payment.

Similarly, reimbursements for property damage, such as a roof replacement, should be posted to the account/category that you used when you recorded the payment for fixing the roof.

To record a payment from an insurance company, you will need the name of the insurance company, the account you will use to pay for the repairs, and a description of the claim. You should also record the amount of the payment.

If you are using Quicken, one possibility is to create an "Insurance Reimbursement Account" (offline Asset or Checking account). You can then record any repair bills as a transfer from your Checking or Credit Card account to the Reimbursement account. Any insurance payments you receive can also be recorded into your Checking account as a transfer to the Reimbursement account.

Another option is to record the insurance reimbursements as credits in the expense category you are using for the incident.

Aetna Federal Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Creating an Insurance Reimbursement Account

An insurance reimbursement account is a type of financial account that allows you to manage and track insurance reimbursements for specific purposes, such as property damage repairs or medical expenses. This account is separate from your regular bank account and is dedicated solely to receiving and disbursing insurance funds. Here's a step-by-step guide on creating an insurance reimbursement account:

Step 1: Identify the Purpose

Start by identifying the specific purpose of the insurance reimbursement account. Are you creating it to manage reimbursements for property damage repairs, medical expenses, or something else? This will help you tailor the account to your specific needs and ensure that the funds are used appropriately.

Step 2: Choose the Type of Account

Different types of reimbursement accounts are available, such as Health Reimbursement Arrangements (HRAs) for medical expenses or property damage repair accounts. HRAs, for example, are employer-funded accounts that allow employees to reimburse themselves for certain medical, dental, or vision expenses. Choose the type of account that aligns with your purpose.

Step 3: Determine Funding Sources

Insurance reimbursement accounts can be funded through insurance payouts, employer contributions, or a combination of both. If you're creating an account for property damage repairs, you'll likely be receiving funds from insurance claims. For medical expense reimbursement, your employer may fund the account, offering defined non-taxed reimbursements for qualified medical expenses.

Step 4: Set Up the Account

Work with your financial institution or insurance provider to set up the reimbursement account. Provide them with the necessary details, such as the purpose of the account, the expected sources of funding, and any specific requirements or restrictions you need in place. They will guide you through the process of establishing the account.

Step 5: Define Eligible Expenses

Clearly define the types of expenses that can be reimbursed through this account. For example, if it's a medical reimbursement account, eligible expenses might include monthly premiums, copayments, deductibles, and other out-of-pocket costs. If it's for property damage repairs, eligible expenses could include repair or replacement costs.

Step 6: Establish Reimbursement Procedures

Determine the process for reimbursing expenses. Typically, you'll pay for expenses upfront and then request reimbursement by submitting receipts, invoices, or other supporting documentation. Some accounts may also allow for direct reimbursement to service providers, such as doctors or contractors, without requiring upfront payment from you.

Step 7: Understand Tax Implications

Insurance reimbursement accounts may have tax advantages or considerations. For example, reimbursements for eligible medical expenses are generally not considered taxable income. However, it's important to consult with a tax professional to understand the specific tax implications for your situation.

By following these steps, you can create an insurance reimbursement account that suits your specific needs. This dedicated account will help you effectively manage and track insurance funds, ensuring that they are used for their intended purposes. Remember to carefully review the terms and conditions of your account and seek professional advice as needed to maximize the benefits of your insurance reimbursement account.

Check Cash Finance & Insurance: What Type of Business?

You may want to see also

Explore related products

![]()

Matching the insurance reimbursement with the costs incurred

When you receive an insurance reimbursement check, it's important to understand how to match it with the costs incurred to fix or replace your property. This process ensures that you properly account for the funds and use them for their intended purpose. Here's a guide to help you navigate this process:

Understanding the Concept of Matching Insurance Reimbursement with Costs Incurred:

The fundamental principle behind matching insurance reimbursement with costs incurred is to allocate the funds received from the insurance company to cover the specific expenses related to the insured loss or damage. This means that you should try to align the reimbursement with the repairs or replacements needed to restore your property to its previous condition.

Documenting and Organizing Expenses:

To effectively match insurance reimbursement with costs incurred, it's crucial to maintain detailed records of all expenses related to the repair or replacement process. Keep all invoices, receipts, and bills associated with the work done. Categorize these expenses based on the nature of the repairs, such as roofing, plumbing, or automotive repairs. This documentation will help you accurately track your spending and facilitate the matching process.

Matching Reimbursement with Costs:

Once you have received the reimbursement check from the insurance company, you can start matching it to the costs incurred. Compare the amount of the check with the total expenses you have documented. If possible, try to allocate the reimbursement funds to specific repair categories. For example, if you received a check for $5,000 and spent $4,000 on a new vehicle after a total loss, you would match that $4,000 with the cost of the replacement vehicle. Any remaining funds can then be allocated to other relevant categories, such as repairs or temporary accommodations.

Handling Surplus or Deficit Scenarios:

In some cases, the reimbursement amount may not exactly match the total costs incurred. There could be a surplus if the reimbursement exceeds your expenses, or a deficit if your expenses are higher than the reimbursement. In the case of a surplus, you may need to return the excess funds to your mortgage lender, especially if they are listed on the check. Consult your lender or insurance company for guidance on handling surplus funds. If you encounter a deficit, review your policy to understand your coverage limits and deductibles. You may need to cover the remaining costs out of pocket or explore alternative funding options to make up for the difference.

Seeking Professional Guidance:

Matching insurance reimbursement with costs incurred can be complex, especially in situations involving substantial losses or multiple categories of repairs. Consider seeking guidance from a qualified accountant or financial advisor, especially if you have concerns about accurately allocating funds. They can help you navigate the process, ensure compliance with any lender requirements, and maximize the benefit of your reimbursement.

Verify Builders Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Labelling insurance claim payments as other income

When a business suffers a loss that is covered by an insurance policy, it recognises a gain in the amount of the insurance proceeds received. This gain is considered non-operational and is typically recorded in a separate account labelled "Gain from Insurance Claims". This separate accounting treatment ensures that the financial statements accurately reflect the economic impact of the loss or damage.

In the context of property damage claims, the initial step is to assess the extent of the damage and estimate the repair or replacement costs. The company should then record an insurance receivable for the expected claim amount. Upon receiving the payment, the business debits the cash account and credits the insurance receivable account. If the insurance proceeds exceed the book value of the damaged asset, the excess is recorded as a gain and labelled as "other income". Conversely, if the proceeds are less than the book value, the shortfall is recognised as a loss.

For individuals, insurance claim payments are typically reimbursements for losses or damages. These reimbursements should be matched, to the extent possible, with the costs incurred to fix or replace the property. For example, if a vehicle is totalled and a reimbursement is received, it should be posted to the automobile "asset" account. Similarly, if repairs are made to a vandalised vehicle, the reimbursement should be posted to the same account or category that was used to record the repair payment.

It is important to note that insurance claim income is generally not taxable. However, if the funds were designated for something else, such as reimbursement for lost income, it may need to be included as taxable income.

Capital One CDs: Are They Safe and Federally Insured?

You may want to see also

Explore related products

![]()

Categorising insurance claim payments

When it comes to categorising insurance claim payments, there are a few key things to keep in mind. Firstly, it's important to understand that insurance claim payments are typically made to reimburse you for a loss. This could be related to property damage, additional living expenses, or other insured events.

In the context of property damage, such as a roof replacement or vehicle repairs, it is generally recommended to match the insurance reimbursement with the costs incurred to fix or replace the property. For example, if you receive a payment for a totalled vehicle and use that money to purchase a new one, you would categorise it under an automobile "asset" account. Similarly, if you receive a payment for a vandalised vehicle and use it towards repairs, you would post it to the same account or category that you used for the original repairs.

In cases where there are multiple inspections and repairs are done in stages, lenders may disburse funds in instalments rather than all at once. It's important to keep this in mind when categorising insurance claim payments. Additionally, depending on the nature and cost of repairs, your insurance premiums may increase after a claim, so be prepared for this possibility.

When it comes to additional living expenses (ALE), such as hotel stays, car rentals, and meals while your home is being repaired, ensure that these checks are made out to you directly and not to your lender. ALE is separate from repair costs and covers the expenses incurred due to being unable to live in your home temporarily.

Finally, remember that if you have a mortgage on your house, the check for repairs will typically be made out to both you and your mortgage lender. Lenders usually require that they are named in the homeowners' policy and included in any insurance payments related to the structure. In some cases, a financial backer or co-insured may need to endorse the claims payment check before you can cash it.

Verify Vehicle Insurance: Quick and Easy Methods

You may want to see also