When determining which formula best describes the amount an insurance company charges for premiums, it is essential to consider several key factors, including risk assessment, policyholder demographics, and historical claims data. The most commonly used formula is the pure premium model, which calculates the expected cost of claims by multiplying the frequency of losses by their severity. However, insurance companies often refine this with additional components such as loading factors, which account for operational expenses, profit margins, and risk margins to ensure financial stability. Other advanced models, like the Poisson distribution for claim frequency and the Pareto distribution for claim severity, are also employed to provide a more nuanced understanding of risk. Ultimately, the choice of formula depends on the insurer’s specific needs, the type of coverage offered, and the complexity of the risk landscape.

Explore related products

What You'll Learn

![]()

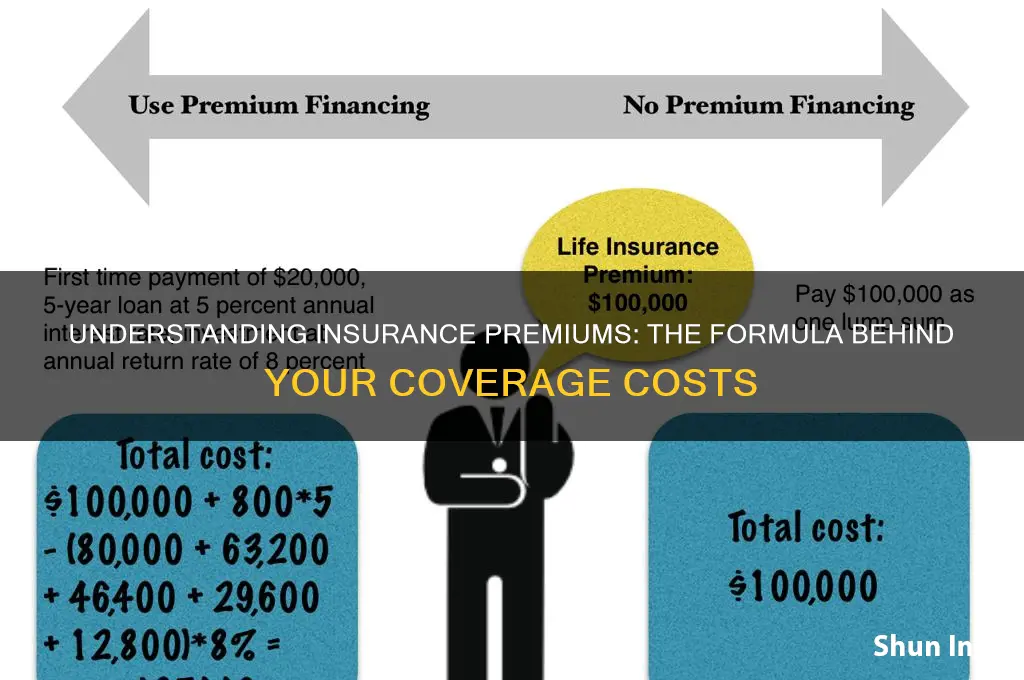

Premium Calculation Formula

Insurance premiums are not arbitrary; they are the result of meticulous calculations designed to balance risk and reward. At the heart of this process lies the Premium Calculation Formula, a critical tool that insurers use to determine how much policyholders should pay. This formula typically incorporates several key variables, including the insured’s risk profile, the coverage amount, and the insurer’s operational costs. For instance, a life insurance premium might be calculated using the formula: *Premium = (Mortality Rate × Sum Assured) + Expenses + Profit Margin*. Here, the mortality rate is derived from actuarial tables based on age, gender, and health, while the sum assured is the payout amount. Understanding this formula helps policyholders grasp why their premiums may differ from others’.

To illustrate, consider auto insurance. The premium calculation often involves a more complex formula: *Premium = (Base Rate × Vehicle Risk Factor) + (Driver Risk Factor × Personal Profile) + Administrative Costs*. The base rate is a starting point set by the insurer, while the vehicle risk factor accounts for the car’s make, model, and safety features. The driver risk factor includes age, driving history, and location. For example, a 25-year-old with a history of traffic violations driving a high-performance car in an urban area will likely pay significantly more than a 45-year-old with a clean record driving a sedan in a rural area. This formula ensures that premiums are tailored to individual risk levels, promoting fairness in pricing.

While the formulas may seem straightforward, their application requires precision and transparency. Insurers must strike a balance between profitability and affordability, ensuring premiums are neither too high to deter customers nor too low to jeopardize financial stability. One practical tip for policyholders is to review their risk factors annually. For health insurance, maintaining a healthy lifestyle can lower premiums over time, as insurers often adjust rates based on updated medical assessments. Similarly, bundling policies or increasing deductibles can reduce overall costs. However, caution is advised when opting for lower premiums through reduced coverage, as this may lead to insufficient protection in the event of a claim.

Comparatively, the premium calculation formula in property insurance often includes additional variables such as location-specific risks (e.g., flood zones or crime rates) and the property’s age and construction materials. For instance, a home in a hurricane-prone area will have a higher premium due to the increased likelihood of damage. Insurers may use a formula like: *Premium = (Base Rate × Risk of Perils) + (Property Value × Coverage Percentage) + Operational Costs*. This highlights the importance of understanding regional risks and investing in mitigation measures, such as storm shutters or reinforced roofing, which can lower premiums over time.

In conclusion, the Premium Calculation Formula is a dynamic and essential tool in the insurance industry, reflecting both individual risk and broader market conditions. By demystifying this formula, policyholders can make informed decisions, optimize their coverage, and potentially reduce costs. Whether for life, auto, health, or property insurance, understanding the variables at play empowers consumers to navigate the complex landscape of insurance premiums with confidence.

Understanding UCC Insurance for Medical Professionals

You may want to see also

Explore related products

![Compound Interest; as Exemplified in the Calculation of Annuities, Immediate and Deferred, Present Values and Amounts, Insurance Premiums, Repayment of Loans, Capitalisation of 1897 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Risk Assessment Factors

Insurance companies rely heavily on risk assessment factors to determine premiums, coverage limits, and policy terms. These factors are the backbone of their pricing models, ensuring that the cost of insurance aligns with the likelihood and potential severity of claims. By analyzing these variables, insurers can predict future losses and maintain financial stability. Understanding these factors empowers consumers to make informed decisions and potentially lower their insurance costs.

Consider age, a universally significant risk factor. For auto insurance, drivers under 25 and over 65 face higher premiums due to statistically elevated accident rates. Similarly, in life insurance, younger individuals typically pay less because they present a lower mortality risk. However, age is just one piece of the puzzle. Insurers also examine driving records, health history, and lifestyle choices. For instance, a 40-year-old with a history of traffic violations may pay more for car insurance than a 22-year-old with a clean record. Practical tip: Maintaining a safe driving history or adopting healthier habits can significantly reduce premiums over time.

Geographic location is another critical factor, often influencing both property and auto insurance rates. Areas prone to natural disasters, such as hurricanes or wildfires, carry higher risks, leading to increased premiums. Similarly, urban areas with higher crime rates or traffic congestion may result in costlier policies. For example, a homeowner in Florida might pay more for property insurance than one in Ohio due to hurricane risks. Analysis reveals that insurers use sophisticated models to assess regional risks, often down to the ZIP code level. Takeaway: When relocating, consider how your new location could impact insurance costs.

Occupation and income level also play a role, particularly in life and disability insurance. High-risk jobs, such as construction or firefighting, often result in higher premiums due to increased injury or fatality risks. Conversely, desk jobs in low-stress environments may qualify for lower rates. Income level affects coverage amounts, as insurers typically recommend policies that replace a percentage of earnings. For instance, a high-income earner might need a larger life insurance policy to protect their family’s financial stability. Caution: Overlooking occupational risks can lead to inadequate coverage or unexpectedly high costs.

Finally, insurers analyze behavioral and lifestyle factors, especially in health and life insurance. Smoking, excessive alcohol consumption, and obesity are red flags that can double or triple premiums. For example, a smoker in their 30s might pay the same life insurance rate as a non-smoker in their 50s. Similarly, participation in high-risk activities like skydiving or scuba diving can increase costs. Comparative analysis shows that insurers often reward healthy behaviors with discounts or lower rates. Conclusion: Small lifestyle changes, such as quitting smoking or improving diet, can yield substantial long-term savings on insurance premiums.

Seeking Medical Care: Options Without Insurance

You may want to see also

Explore related products

![]()

Claims Payout Equation

The Claims Payout Equation is a critical tool for insurance companies to determine the amount they owe policyholders after a claim is filed. At its core, this equation balances the insured’s coverage limits, the actual loss incurred, and any applicable deductibles or policy exclusions. For instance, if a homeowner files a claim for $50,000 in property damage and their policy has a $1,000 deductible, the payout would be $49,000, assuming the loss is fully covered. This straightforward calculation ensures fairness and adherence to the policy terms, but it’s just the starting point for understanding how insurers assess claims.

Analyzing the equation reveals its complexity beyond simple arithmetic. Insurers often factor in depreciation, especially for property claims, reducing the payout based on the item’s age and condition. For example, a 10-year-old roof might be depreciated by 40%, meaning the payout would reflect its current value rather than the cost of a new one. Additionally, policy limits act as a ceiling; if a claim exceeds the coverage amount, the insurer is not obligated to pay beyond that threshold. This highlights the importance of policyholders understanding their coverage details to avoid unexpected shortfalls.

From a practical standpoint, policyholders can maximize their claims payout by documenting losses thoroughly and filing claims promptly. For health insurance, keeping detailed medical records and receipts ensures accurate reimbursement, especially for out-of-pocket expenses. In auto insurance, providing clear evidence of vehicle damage and repair estimates can prevent disputes over payout amounts. Proactive steps like these not only expedite the claims process but also reduce the likelihood of underpayment.

Comparatively, the Claims Payout Equation differs across insurance types. In life insurance, the payout is typically a fixed amount specified in the policy, whereas in liability insurance, it’s tied to the damages awarded in a lawsuit, up to the policy limit. Health insurance often involves co-pays and coinsurance, further complicating the payout calculation. Understanding these nuances is essential for both insurers and policyholders to navigate the claims process effectively.

Ultimately, the Claims Payout Equation is more than a formula—it’s a framework for fairness and financial protection. For insurers, it ensures payouts align with policy terms and risk assessments. For policyholders, it underscores the importance of selecting adequate coverage and understanding policy details. By demystifying this equation, both parties can approach claims with clarity and confidence, fostering trust in the insurance system.

Trip Interruption Insurance: When Does it Apply?

You may want to see also

Explore related products

![]()

Policy Cost Determinants

Insurance premiums are not arbitrary; they are meticulously calculated based on a multitude of factors that assess risk and potential liability. At the heart of this calculation are Policy Cost Determinants, which serve as the backbone of pricing models. These determinants include age, health status, occupation, location, and lifestyle choices. For instance, a 45-year-old smoker with a high-risk job in an urban area will pay significantly more for life insurance than a 25-year-old non-smoker working a desk job in a rural setting. Understanding these variables is crucial for both insurers and policyholders, as they directly influence the cost of coverage.

One of the most influential determinants is age, which correlates strongly with health risks and life expectancy. Insurers often use actuarial tables to predict the likelihood of claims based on age groups. For example, auto insurance premiums for teenagers can be up to three times higher than those for drivers in their 30s due to higher accident rates. Similarly, health insurance costs tend to rise sharply after age 50, reflecting increased medical needs. To mitigate costs, individuals can take proactive steps like enrolling in wellness programs or maintaining a healthy lifestyle, which may qualify them for discounts.

Another critical factor is location, which impacts risk levels across different insurance types. In property insurance, homes in flood-prone or high-crime areas will have higher premiums due to increased likelihood of claims. Similarly, auto insurance rates vary by ZIP code, with urban drivers paying more due to higher traffic density and theft rates. Policyholders can reduce costs by installing security systems, opting for higher deductibles, or relocating to safer neighborhoods. Insurers use geospatial data and historical claims trends to fine-tune these calculations, ensuring premiums align with localized risks.

Occupation and lifestyle also play a significant role in determining policy costs. Jobs with higher physical risk, such as construction or firefighting, often result in elevated life and disability insurance premiums. Similarly, hobbies like skydiving or racing can increase rates due to perceived danger. Even daily habits, such as smoking or excessive alcohol consumption, can lead to higher health insurance costs. Insurers may require medical exams or lifestyle questionnaires to assess these risks accurately. Policyholders can lower premiums by choosing safer professions, quitting harmful habits, or providing evidence of risk-reducing behaviors.

Finally, coverage limits and deductibles are adjustable determinants that policyholders can control. Higher coverage limits mean greater financial protection but also higher premiums. Conversely, opting for a higher deductible—the amount paid out-of-pocket before insurance kicks in—can significantly reduce annual costs. For example, increasing a car insurance deductible from $500 to $1,000 could lower premiums by 10–20%. However, this strategy requires careful consideration of one’s ability to cover the deductible in case of a claim. Balancing these factors allows individuals to customize policies to their budget and risk tolerance.

In summary, Policy Cost Determinants are a complex interplay of personal, environmental, and behavioral factors that insurers use to calculate premiums. By understanding and, where possible, modifying these variables, policyholders can take control of their insurance costs. Whether through lifestyle changes, strategic policy adjustments, or informed location choices, the power to influence premiums lies in recognizing and addressing these determinants.

Medical Insurance in NYC: Where to Apply

You may want to see also

Explore related products

![]()

Underwriting Formula Basics

Insurance companies rely on underwriting formulas to determine the premium amount for policyholders. These formulas are complex and multifaceted, taking into account various factors such as age, health status, occupation, and lifestyle habits. For instance, a 35-year-old non-smoker with a sedentary job and no pre-existing medical conditions will likely pay a lower premium for life insurance compared to a 55-year-old smoker with a high-risk occupation and a history of heart disease. The underwriting formula used by insurance companies typically includes a base rate, which is adjusted based on individual risk factors.

To illustrate the underwriting process, consider a simplified formula: Premium = Base Rate × (1 + Risk Factor 1 + Risk Factor 2 +... + Risk Factor n). In this formula, the base rate represents the average premium for a standard policyholder, while the risk factors account for individual variations. For example, a life insurance policy might have a base rate of $500, with additional risk factors such as age (+$10 per year), smoking status (+$200 for smokers), and occupation (+$50 for high-risk jobs). A 40-year-old non-smoker with a low-risk job would pay $500 + ($10 × 40) + $0 + $0 = $900 annually.

When designing underwriting formulas, actuaries must balance accuracy with simplicity. Overly complex formulas can lead to confusion and errors, while overly simplistic formulas may fail to capture important risk factors. For example, using a single age-based multiplier might be easy to calculate but could unfairly penalize older individuals who maintain a healthy lifestyle. A more nuanced approach might involve separate multipliers for age, health status, and lifestyle habits, allowing for a more precise assessment of risk. Insurance companies often use proprietary algorithms and data analytics tools to refine their underwriting formulas, incorporating large datasets and machine learning techniques to improve accuracy.

A critical aspect of underwriting formulas is their ability to adapt to changing circumstances. As medical research advances and societal trends evolve, insurance companies must update their formulas to reflect new risk factors and mitigation strategies. For instance, the emergence of wearable fitness devices has enabled insurers to offer discounted premiums to policyholders who maintain a certain level of physical activity. Similarly, advancements in genetic testing have raised questions about the ethical use of such data in underwriting formulas. Insurers must navigate these complexities while ensuring their formulas remain fair, transparent, and compliant with regulatory requirements.

In practice, policyholders can take proactive steps to optimize their premiums by understanding the underwriting formula used by their insurance company. This might involve adopting healthier habits, such as quitting smoking or increasing physical activity, to reduce risk factors and lower premiums. Additionally, individuals can shop around for insurance providers that offer more favorable underwriting terms or specialize in serving specific demographics. For example, some insurers cater to seniors or individuals with pre-existing conditions, using underwriting formulas that are more lenient in these areas. By demystifying the underwriting process and taking control of their risk profile, policyholders can make informed decisions to secure the best possible coverage at the most affordable price.

California's IEHP: Understanding Medicaid Insurance and Its Benefits

You may want to see also

Frequently asked questions

The formula that best describes the amount an insurance company charges for a policy is Premium = (Expected Claims + Expenses + Profit) / Number of Policies. This formula accounts for the expected costs of claims, operational expenses, and the desired profit margin, spread across all policyholders.

The amount an insurance company pays out in claims is best described by the formula Claims Payout = Sum of (Claim Amount × Probability of Claim Occurrence). This formula calculates the expected total claims by multiplying the potential claim amounts by their respective probabilities and summing them up.

The amount an insurance company retains as profit is best described by the formula Profit = Total Premiums Collected − (Total Claims Paid + Expenses). This formula subtracts the total claims paid and operational expenses from the total premiums collected to determine the net profit.