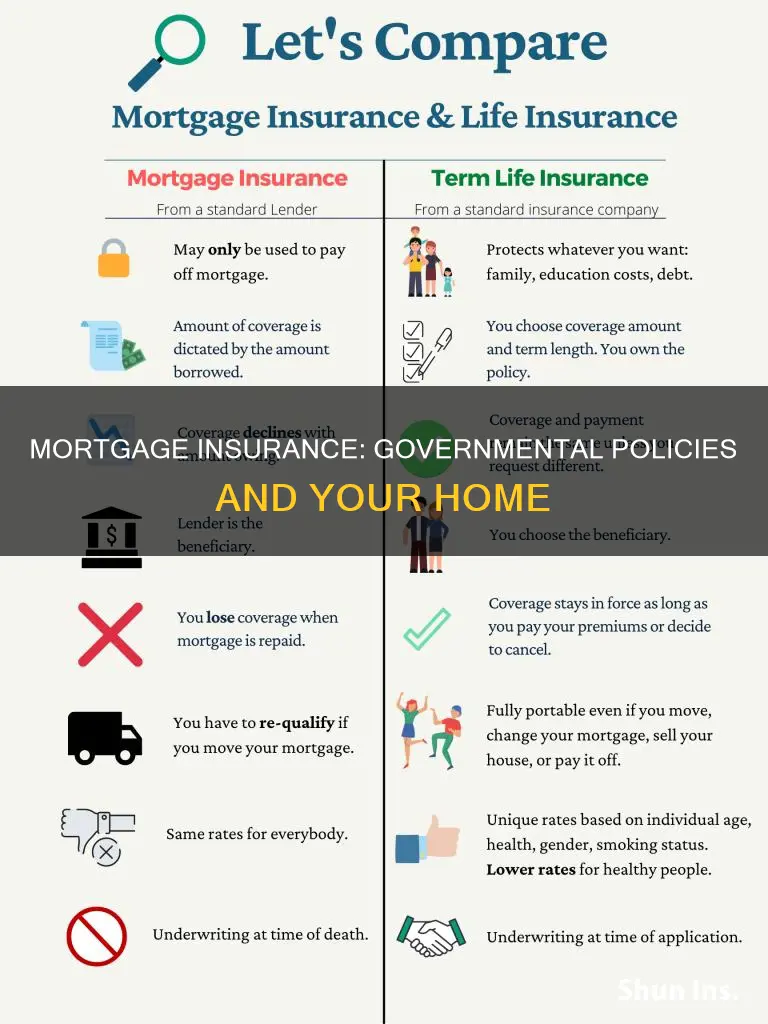

Mortgage insurance is a means of reducing the risk to the lender of issuing a loan to the borrower. Typically, borrowers who make a down payment of less than 20% of the purchase price of the home are required to pay for mortgage insurance. Mortgage insurance is also typically required on Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans. Mortgage insurance does not protect the borrower and increases the cost of the loan.

| Characteristics | Values |

|---|---|

| Who does it protect? | The lender, not the borrower |

| Who needs to pay for it? | Borrowers making a down payment of less than 20% of the purchase price of the home |

| When do you stop paying for it? | When you reach 20% equity in your home |

| How much does it cost? | Typically $30 to $70 per month for each $100,000 borrowed |

| What is included in the cost? | An upfront cost and a monthly cost |

| Can it be cancelled? | Yes, when the borrower has paid their loan balance low enough |

Explore related products

What You'll Learn

- Private mortgage insurance (PMI) is an extra fee for borrowers who make a down payment of less than 20%

- PMI protects the lender, not the borrower, if loan payments are missed

- FHA mortgage insurance is required for all Federal Housing Administration loans

- Mortgage insurance increases the cost of a loan

- Borrowers can request to cancel PMI when their mortgage balance reaches 80% of their home's value

![]()

Private mortgage insurance (PMI) is an extra fee for borrowers who make a down payment of less than 20%

Private mortgage insurance (PMI) is a type of insurance that borrowers may be required to purchase if they take out a conventional loan with a down payment of less than 20% of the purchase price. It is an extra fee that protects the lender in the event that the borrower is unable to make loan payments. This means that PMI does not protect the borrower; they can still lose their home through foreclosure if they fall behind on payments.

PMI is typically included in the borrower's monthly mortgage payment and can cost $30 to $70 per month for every $100,000 borrowed. The exact amount depends on the loan and down payment size, the type of interest rate, and the borrower's credit score. There are different types of PMI, including borrower-paid, single-premium, lender-paid, split-premium, and federal home loan premium. The borrower may be able to choose from a few different PMI options offered by the lender.

PMI can help borrowers qualify for a loan that they might not otherwise be eligible for. However, it increases the cost of the loan. Borrowers can avoid paying PMI by making a 20% down payment, although this can be challenging for many buyers to save for. Another option is a piggyback loan, which combines two loans: one for 80% of the home's price and the other for 10%.

Once the borrower reaches 20% equity in their home, they no longer need to pay PMI, and lenders are required to cancel it when the mortgage balance drops to 78% of the home's original value or halfway through the loan term, whichever comes first.

Calculating Mortgage Insurance: Excel Formula Guide

You may want to see also

Explore related products

![]()

PMI protects the lender, not the borrower, if loan payments are missed

Private mortgage insurance (PMI) is a type of insurance that borrowers are typically required to pay when they take out a conventional loan with a down payment of less than 20% of the purchase price of the home. PMI is arranged by the lender and provided by private insurance companies. It protects the lender against losses caused by borrowers failing to make loan payments.

PMI does not protect borrowers if they fall behind on their mortgage payments. In such cases, the borrower can still lose their home through foreclosure. Additionally, PMI does not make mortgage payments for borrowers if they are unemployed or unable to pay for any other reason. It is important to note that PMI is not the same as "mortgage insurance", which is sometimes sold by mortgage companies and does cover payments under certain circumstances.

PMI can help borrowers qualify for a loan that they might not otherwise be eligible for due to the lower down payment. However, it increases the cost of the loan. The monthly premium for PMI is typically added to the borrower's monthly mortgage payment. The premium amount is based on factors such as the down payment amount, credit score, and type of mortgage.

Borrowers can explore options to reduce or eliminate PMI costs. For example, some lenders may offer conventional loans with higher interest rates instead of PMI, which can be more or less expensive than PMI depending on individual circumstances. Additionally, once the borrower has paid down 20% or more of the home's value, they may be eligible to cancel PMI. However, specific requirements must be met, and cancellation policies vary depending on the loan type.

Insuring a House in Trust: What You Need to Know

You may want to see also

Explore related products

![]()

FHA mortgage insurance is required for all Federal Housing Administration loans

FHA loans are designed to help low- to moderate-income families attain homeownership, and they are particularly popular with first-time homebuyers. FHA loans require a lower minimum down payment than many conventional loans, and applicants may have lower credit scores than what is usually required. The FHA has a maximum loan amount that it will insure, which is known as the FHA lending limit. This limit varies by county and increases annually for many counties in the United States.

FHA borrowers must pay two types of mortgage insurance premiums (MIPs)—one upfront and the other monthly. The upfront cost is paid as part of the closing costs, while the monthly cost is included in the monthly payment. If borrowers cannot pay the upfront fee out of pocket, they are allowed to roll the fee into their mortgage, although this increases the loan amount and overall cost. FHA mortgage insurance costs the same regardless of the borrower's credit score, with only a slight increase in price for down payments of less than five percent.

Mortgage insurance, in general, lowers the risk to the lender of making a loan. This insurance protects the lender—not the borrower—in the event that the borrower falls behind on their payments. It also enables borrowers to qualify for a loan that they might not otherwise be able to get, although it increases the cost of the loan.

Insuring Your Acreage: What You Need to Know

You may want to see also

Explore related products

$4.99 $14.99

![]()

Mortgage insurance increases the cost of a loan

Mortgage insurance, despite lowering the risk to the lender and helping borrowers qualify for a loan, increases the cost of a loan. This is because the cost of mortgage insurance is included in the borrower's total monthly payment to the lender, the costs at closing, or both.

Private mortgage insurance (PMI) is a type of mortgage insurance that borrowers are typically required to pay when they take out a conventional loan with a down payment of less than 20% of the purchase price of the home. PMI rates vary by down payment amount and credit score but are generally cheaper for borrowers with good credit. Most PMI is paid monthly, with little to no initial payment required at closing. However, some lenders may offer lender-paid mortgage insurance, where the cost of PMI is included in the borrower's monthly payment until they achieve 20% equity in their home, in exchange for a higher interest rate.

Federal Housing Administration (FHA) loans also require mortgage insurance premiums, which are paid to the FHA. FHA mortgage insurance includes an upfront cost, paid as part of the closing costs, and a monthly cost included in the monthly payment. If the borrower chooses to roll the upfront fee into their mortgage instead of paying it out of pocket, their loan amount and overall cost increase.

Similarly, the US Department of Agriculture (USDA) loan program follows a similar structure to the FHA, but is typically cheaper. The Department of Veterans' Affairs (VA)-backed loans function similarly, with the VA guarantee replacing mortgage insurance. While there is no monthly mortgage insurance premium, borrowers pay an upfront "funding fee", the amount of which varies.

Bumper-to-Bumper Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Borrowers can request to cancel PMI when their mortgage balance reaches 80% of their home's value

Private mortgage insurance (PMI) is a type of insurance that borrowers are typically required to pay when they take out a conventional loan with a down payment of less than 20% of the purchase price of the home. PMI protects the lender in the event that the borrower is unable to make loan payments. It is important to note that PMI does not provide any protection for the borrower, and they can still lose their home through foreclosure if they fall behind on their payments.

It is worth noting that there are alternative options to PMI. Some lenders may offer a "piggyback" second mortgage, which may be marketed as a cheaper alternative. Additionally, lenders sometimes offer conventional loans with smaller down payments that do not require PMI, but these loans usually come with a higher interest rate. Borrowers should carefully consider the different options and compare the total costs to make an informed decision.

Furthermore, there are instances where borrowers may be able to get rid of PMI earlier. For example, if the increased value of the home is due to improvements made to the property, such as renovations, lenders may waive the standard requirements for PMI cancellation. Additionally, if interest rates have dropped since the borrower took out the mortgage, refinancing may provide an opportunity to save money and get rid of PMI if the new loan balance is less than 80% of the home's value.

In conclusion, while PMI can be beneficial for borrowers seeking to qualify for a loan with a low down payment, it is an additional cost. Borrowers can request to cancel PMI when their mortgage balance reaches 80% of their home's value, and there may be alternative options or opportunities to cancel PMI earlier depending on individual circumstances. It is important for borrowers to stay informed about their PMI cancellation schedule and lender requirements to make the best financial decisions.

Farmers Insurance: Unraveling the Rental Coverage Conundrum

You may want to see also

Frequently asked questions

Governmental mortgage insurance is insurance provided by the government that lowers the risk to the lender of making a loan to you, so you can qualify for a loan that you might not otherwise be able to get.

Governmental mortgage insurance is typically required on Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans. It is also required when the down payment is less than 20% of the purchase price of the home.

The cost of governmental mortgage insurance depends on the loan and down payment size, the type of mortgage, and your credit score. Generally, it ranges from 0.58% to 1.86% annually of the mortgage loan amount.

Governmental mortgage insurance is typically paid as part of your monthly mortgage payment, but some lenders allow a one-time upfront payment at closing or a combination of upfront and monthly payments.