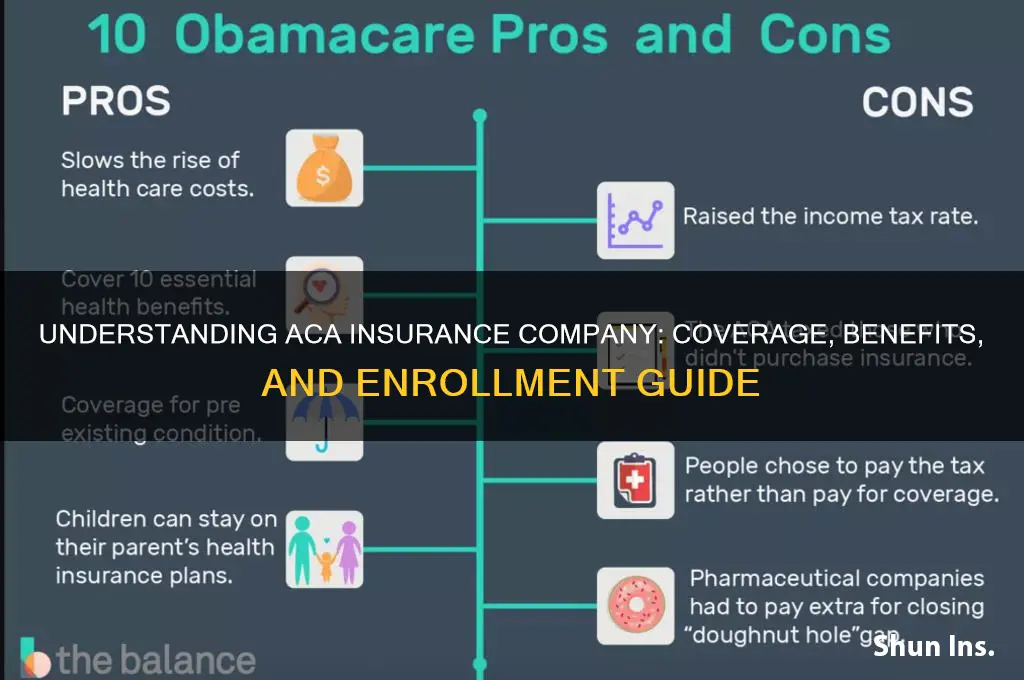

ACA Insurance Company, often associated with the Affordable Care Act (ACA), is a term that can refer to various health insurance providers offering plans compliant with the ACA’s regulations. These companies provide coverage that meets essential health benefit requirements, such as preventive care, prescription drugs, and maternity care, while also adhering to ACA mandates like pre-existing condition coverage and no lifetime limits. While ACA Insurance Company is not a specific entity, it encompasses a wide range of insurers participating in the ACA marketplace, including well-known names like Blue Cross Blue Shield, UnitedHealthcare, and Aetna, among others. These companies play a crucial role in expanding access to affordable healthcare for millions of Americans through ACA-compliant plans.

Explore related products

$36.33 $54.99

What You'll Learn

- History and Founding: Details about Aca Insurance Company's establishment, founders, and early years

- Services Offered: Overview of insurance products and coverage options provided by the company

- Customer Reviews: Insights into client experiences, ratings, and feedback on Aca Insurance

- Financial Strength: Analysis of the company's financial stability and industry rankings

- Contact Information: How to reach Aca Insurance Company for inquiries or support

![]()

History and Founding: Details about Aca Insurance Company's establishment, founders, and early years

The ACA Insurance Company, often referred to in the context of the Affordable Care Act (ACA), is not a single, specific insurance company but rather a term used to describe health insurance providers that comply with the regulations set forth by the ACA, also known as Obamacare. However, if we consider the historical and foundational aspects of health insurance companies that have been significantly influenced by the ACA, we can trace the establishment and evolution of such entities. The ACA, signed into law in 2010, revolutionized the health insurance industry by mandating that all health insurance plans meet certain standards, including covering pre-existing conditions and offering essential health benefits. This legislative framework prompted many existing insurance companies to adapt their policies and services to comply with the new regulations, effectively reshaping the industry.

The roots of health insurance in the United States date back to the early 20th century, with companies like Blue Cross Blue Shield emerging in the 1920s and 1930s. These early insurers laid the groundwork for the modern health insurance industry. However, the ACA marked a pivotal moment in the history of health insurance, as it not only expanded access to healthcare but also standardized the quality of coverage. Companies that were already established had to reevaluate their offerings, while new entrants saw an opportunity to capitalize on the expanded market. The ACA's establishment of health insurance marketplaces, where individuals and small businesses could purchase standardized plans, further democratized access to health insurance.

The founders of the companies that became ACA-compliant were often visionaries in the healthcare and insurance sectors, recognizing the need for comprehensive and affordable coverage. For instance, executives from longstanding insurance companies like UnitedHealth Group, Aetna, and Cigna played crucial roles in adapting their organizations to meet ACA requirements. These leaders understood that compliance with the ACA was not just a legal obligation but also a business opportunity to reach millions of previously uninsured Americans. Their strategic decisions during the early years of the ACA's implementation were instrumental in shaping the current landscape of health insurance.

In the early years following the ACA's passage, insurance companies faced significant challenges, including technological hurdles in setting up online marketplaces, educating consumers about the new options, and managing the financial risks associated with covering a broader population. Despite these challenges, many companies successfully navigated the transition, thanks to the leadership of their founders and executives. The period also saw the rise of new players in the market, such as Oscar Health, which was founded in 2012 with a focus on leveraging technology to provide user-friendly, ACA-compliant health insurance plans. These early years were marked by innovation, adaptation, and a commitment to expanding healthcare access.

The establishment and growth of ACA-compliant insurance companies reflect a broader trend in the healthcare industry toward greater inclusivity and standardization. The founders and leaders of these companies played a critical role in ensuring that the vision of the ACA was realized, providing millions of Americans with access to quality healthcare. Their efforts during the early years of the ACA's implementation laid the foundation for a more equitable and comprehensive health insurance system. As the industry continues to evolve, the history and founding of these companies remain a testament to the transformative power of policy and leadership in shaping public health outcomes.

Penalties for Not Enrolling in Medicare Part D

You may want to see also

Explore related products

$64.95 $64.95

![]()

Services Offered: Overview of insurance products and coverage options provided by the company

ACA Insurance Company, also known as Affordable Care Act Insurance, primarily focuses on providing health insurance plans that comply with the regulations set forth by the Affordable Care Act (ACA). The company offers a range of health insurance products designed to cater to individuals, families, and small businesses, ensuring that policyholders have access to essential health benefits as mandated by the ACA. These plans typically include coverage for doctor visits, hospital stays, emergency care, prescription drugs, maternity and newborn care, mental health services, and preventive care without additional costs.

One of the key services offered by ACA Insurance Company is the provision of Metal Tier Plans, which are categorized as Bronze, Silver, Gold, and Platinum. Each tier represents a different balance between monthly premiums and out-of-pocket costs. Bronze plans generally have lower monthly premiums but higher out-of-pocket costs, while Platinum plans offer the highest level of coverage with lower out-of-pocket expenses but higher premiums. This tiered system allows customers to choose a plan that best fits their budget and healthcare needs.

In addition to the Metal Tier Plans, ACA Insurance Company provides Catastrophic Health Plans for individuals under 30 or those who qualify for a hardship exemption. These plans are designed to protect against high medical costs in the event of a severe illness or accident, offering a safety net with lower premiums but higher deductibles. While they cover essential health benefits, they typically require policyholders to pay for most routine medical expenses out of pocket until the deductible is met.

For small businesses, ACA Insurance Company offers Small Group Health Insurance Plans that comply with ACA requirements. These plans provide employers with options to offer health coverage to their employees, often with the flexibility to choose from various coverage levels and provider networks. The company also assists businesses in navigating the complexities of ACA compliance, including reporting requirements and employee eligibility criteria.

Furthermore, ACA Insurance Company extends Subsidized Health Insurance Plans for eligible individuals and families with lower incomes. Through the Health Insurance Marketplace, policyholders may qualify for premium tax credits or cost-sharing reductions, making health insurance more affordable. The company’s representatives guide customers through the application process to determine their eligibility for these subsidies, ensuring they receive the maximum financial assistance available.

Lastly, ACA Insurance Company emphasizes Preventive Care and Wellness Programs as part of its coverage options. These programs focus on early detection and prevention of illnesses, offering services such as vaccinations, screenings, and wellness visits at no additional cost. By promoting proactive healthcare, the company aims to improve overall health outcomes while reducing long-term healthcare expenses for its policyholders.

Understanding HSA Enrollment with Medical Insurance

You may want to see also

Explore related products

![]()

Customer Reviews: Insights into client experiences, ratings, and feedback on Aca Insurance

ACA Insurance, also known as Affordable Care Act Insurance, is a term often associated with health insurance plans provided under the Affordable Care Act (ACA), commonly referred to as Obamacare. These plans are offered by various private insurance companies that comply with ACA regulations, ensuring coverage for essential health benefits, pre-existing conditions, and preventive services. When exploring customer reviews and feedback on ACA Insurance, it’s important to note that experiences can vary widely depending on the specific insurer, plan, and individual circumstances. However, common themes emerge from client insights that provide valuable perspectives for prospective policyholders.

Customer Experiences: A Mixed Bag of Satisfaction and Challenges

Many customers praise ACA Insurance for its accessibility and affordability, particularly for individuals and families who previously struggled to secure health coverage. Reviews often highlight the peace of mind that comes with knowing essential health services are covered, including maternity care, mental health services, and prescription drugs. For instance, a significant number of policyholders appreciate the subsidies and tax credits available through the ACA marketplace, which make premiums more manageable. However, some clients report challenges with high deductibles and out-of-pocket costs, which can offset the perceived affordability of the plans. These mixed experiences underscore the importance of carefully reviewing plan details before enrollment.

Ratings: Consistency in Coverage, Variability in Service

ACA Insurance plans generally receive positive ratings for their comprehensive coverage, with many customers feeling adequately protected against unforeseen medical expenses. According to reviews on platforms like HealthCare.gov and third-party rating sites, plans often score well in categories such as coverage breadth and adherence to ACA standards. However, ratings for customer service and claims processing are more variable. Some clients report seamless interactions with their insurers, while others express frustration with long wait times, confusing billing processes, and difficulties reaching representatives. This disparity suggests that while the core insurance product is reliable, the overall experience can be heavily influenced by the insurer’s operational efficiency.

Feedback: Praise for Inclusivity, Criticism for Complexity

A recurring theme in customer feedback is the inclusivity of ACA Insurance, particularly for individuals with pre-existing conditions who were previously denied coverage. Many reviewers commend the ACA for eliminating discriminatory practices and ensuring equal access to healthcare. However, the complexity of navigating the marketplace and understanding plan specifics is a common point of criticism. Customers often mention feeling overwhelmed by the multitude of options and the technical jargon used in plan descriptions. Additionally, some express frustration with the annual open enrollment period, which limits flexibility in changing plans outside of specific windows.

Insights for Prospective Clients: What to Consider

For those considering ACA Insurance, customer reviews offer valuable insights into what to expect. Prospective policyholders should prioritize researching insurers’ reputations for customer service and claims handling, as these factors significantly impact the overall experience. Additionally, understanding the trade-offs between premiums, deductibles, and coverage limits is crucial for selecting a plan that aligns with individual needs and budget. Reading detailed reviews and seeking recommendations from trusted sources can help navigate the complexities of the marketplace. Ultimately, while ACA Insurance has transformed access to healthcare for millions, maximizing its benefits requires informed decision-making and proactive engagement with the available resources.

Emergency Surgery: Claiming Medical Insurance for Unexpected Operations

You may want to see also

Explore related products

![]()

Financial Strength: Analysis of the company's financial stability and industry rankings

ACA Insurance Company, also known as American Continental Assurance Company, is a subsidiary of ACA Financial Guaranty Corporation, which is a monoline bond insurer. To assess the financial strength and stability of ACA Insurance Company, it is essential to examine its financial ratings, industry rankings, and overall performance in the insurance sector. Financial strength is a critical factor for insurance companies, as it reflects their ability to meet policyholder obligations and withstand financial challenges.

One of the primary indicators of ACA Insurance Company's financial stability is its credit ratings from reputable agencies such as A.M. Best, Standard & Poor's (S&P), Moody's, and Fitch Ratings. These agencies evaluate the company's financial health, risk management practices, and ability to fulfill its financial commitments. Historically, ACA has maintained strong ratings, although specific ratings may vary over time due to market conditions and strategic decisions. For instance, A.M. Best, a leading insurance rating agency, assesses companies based on their balance sheet strength, operating performance, business profile, and enterprise risk management. A high rating from A.M. Best, such as "A" or better, indicates superior financial stability and a strong ability to meet policyholder obligations.

In addition to credit ratings, ACA Insurance Company's financial strength can be analyzed through its risk-based capital (RBC) ratios and solvency margins. The RBC ratio measures the amount of capital an insurance company holds relative to the minimum capital required by regulators to cover potential losses. A higher RBC ratio signifies greater financial stability and a stronger ability to absorb shocks. ACA's RBC ratios have consistently met or exceeded regulatory requirements, reflecting its prudent capital management practices. Furthermore, the company's solvency margin, which compares available assets to liabilities, provides additional insight into its financial health and ability to remain solvent in adverse scenarios.

Industry rankings also play a crucial role in assessing ACA Insurance Company's financial strength. ACA operates within the bond insurance sector, where it competes with other monoline insurers and financial guarantors. Its market share, premium growth, and claims-paying ability are key metrics used in industry comparisons. ACA has established itself as a reliable player in the bond insurance market, particularly in guaranteeing municipal bonds and structured finance products. Its ability to maintain a competitive position in a niche market underscores its financial resilience and strategic focus.

Lastly, ACA Insurance Company's financial stability is further reinforced by its parent company, ACA Financial Guaranty Corporation, and its strategic partnerships. The parent company's financial resources and support contribute to ACA's overall strength, enabling it to navigate economic uncertainties and market volatility. Additionally, ACA's adherence to regulatory standards and its commitment to transparency enhance its credibility and financial standing in the industry. By consistently meeting regulatory requirements and maintaining strong financial metrics, ACA Insurance Company demonstrates its ability to provide long-term value to policyholders and stakeholders.

In conclusion, the financial strength of ACA Insurance Company is evident through its strong credit ratings, robust risk-based capital ratios, and competitive industry rankings. These factors collectively highlight the company's financial stability, risk management capabilities, and ability to fulfill its obligations. As the insurance landscape continues to evolve, ACA's commitment to maintaining a solid financial foundation positions it as a reliable and trustworthy entity in the bond insurance market.

Obamacare's Impact: Millions Gain Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Contact Information: How to reach Aca Insurance Company for inquiries or support

ACA Insurance Company, also known as Affordable Care Act Insurance Company, is a term often associated with health insurance providers participating in the Health Insurance Marketplace established by the Affordable Care Act (ACA). Since ACA itself is not a specific insurance company but rather a law that regulates health insurance, individuals seeking contact information for inquiries or support should reach out to the specific insurance provider they are enrolled with or the official ACA resources. Below are detailed ways to contact relevant entities for assistance.

Contacting Your ACA-Compliant Insurance Provider: If you have purchased a health insurance plan through the ACA Marketplace, your first point of contact should be the insurance company that issued your policy. Most ACA-compliant insurance companies provide multiple channels for customer support, including phone, email, and online portals. To find the contact information, check your insurance card, policy documents, or the insurer’s official website. For example, companies like Blue Cross Blue Shield, UnitedHealthcare, or Aetna have dedicated customer service lines and online chat options for policyholders.

Using the Health Insurance Marketplace for Support: For general inquiries about ACA plans, enrollment, or subsidies, you can contact the Health Insurance Marketplace directly. The Marketplace offers a toll-free call center at 1-800-318-2596 (TTY: 1-855-889-4325), available 24/7. Representatives can assist with questions about plan options, eligibility, and application status. Additionally, you can log in to your Healthcare.gov account to access live chat support or submit inquiries through their online messaging system.

Reaching Out to State-Based Marketplaces: Some states operate their own health insurance marketplaces instead of using Healthcare.gov. If you reside in a state with a state-based marketplace, such as California (Covered California) or New York (NY State of Health), visit their official website for contact information. These platforms typically provide phone numbers, email addresses, and in-person assistance options tailored to residents of that state.

Utilizing Social Media and Online Resources: Many insurance companies and ACA-related organizations maintain active social media profiles on platforms like Facebook, Twitter, and LinkedIn. You can send direct messages or post inquiries on their pages for assistance. Additionally, Healthcare.gov and state marketplace websites offer extensive FAQs, guides, and tutorials to address common questions without needing direct contact.

Local Assistance Through Navigators or Brokers: If you prefer in-person or localized support, ACA Navigators and certified insurance brokers are available in many communities. These professionals can help with plan comparisons, enrollment, and troubleshooting. To find a Navigator or broker near you, use the "Find Local Help" tool on Healthcare.gov or contact your state’s marketplace for a list of authorized agents. Their contact details are typically provided on the marketplace’s website or through their helpline.

By utilizing these channels, you can efficiently reach out to the appropriate entities for inquiries or support related to ACA-compliant insurance plans. Always ensure you are using official resources to avoid scams or misinformation.

Understanding Deductible Medical Insurance: Who Reaches Their Limit?

You may want to see also

Frequently asked questions

ACA Insurance Company, also known as Affordable Care Act Insurance Company, refers to insurers that provide health insurance plans compliant with the Affordable Care Act (ACA). These plans are often sold on the Health Insurance Marketplace.

A: No, ACA Insurance Company is not a government entity. It refers to private insurance companies that offer ACA-compliant health plans, regulated under the Affordable Care Act.

ACA Insurance Company plans cover essential health benefits, including doctor visits, hospitalization, prescription drugs, preventive care, and mental health services, as mandated by the ACA.

You can enroll in an ACA Insurance Company plan through the Health Insurance Marketplace (Healthcare.gov) during the annual Open Enrollment Period or during a Special Enrollment Period if you qualify.

Yes, ACA Insurance Company plans are the same as Obamacare plans. "Obamacare" is another term for health insurance plans that comply with the Affordable Care Act (ACA).