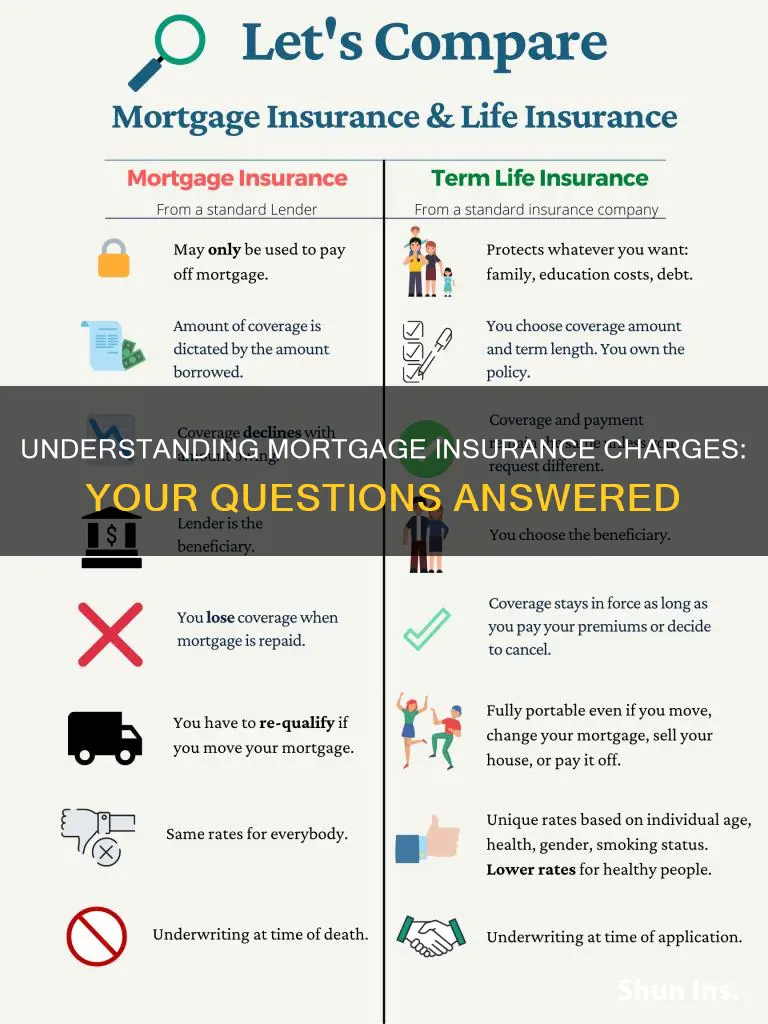

If you're being charged mortgage insurance, it's because you're paying for a type of insurance that protects your lender or titleholder against financial loss if you default on payments, pass away, or are otherwise unable to meet your mortgage obligations. This insurance is called Private Mortgage Insurance (PMI) and is typically required when a borrower makes a low down payment (usually less than 20% of the purchase price of the home). PMI rates vary by down payment amount and credit score but are generally cheaper for borrowers with good credit. It's important to note that PMI protects the lender, not the borrower, and can lead to significant unnecessary costs if not canceled promptly when no longer required.

| Characteristics | Values |

|---|---|

| Who does mortgage insurance protect? | The lender or titleholder |

| Who pays for mortgage insurance? | The borrower |

| When is mortgage insurance required? | When the down payment is less than 20% of the purchase price or loan-to-value (LTV) ratio |

| What is the purpose of mortgage insurance? | To lower the risk to the lender and allow borrowers to qualify for loans they might not otherwise be able to get |

| What types of loans require mortgage insurance? | Federal Housing Administration (FHA) loans, U.S. Department of Agriculture (USDA) loans, conventional loans, and VA-backed loans |

| How is mortgage insurance paid? | Through monthly premiums, upfront premiums paid at closing, or a combination of both |

| Can borrowers choose their mortgage insurance provider? | No, the lender arranges mortgage insurance, but borrowers can choose their hazard insurance provider |

| Can borrowers cancel their mortgage insurance? | Yes, once the outstanding loan amount or principal balance drops below 80% LTV or 78% of the home's original value |

| What happens if borrowers are overcharged or not promptly cancelled? | Overcharging has been a long-standing problem, and borrowers may pay significant amounts of unnecessary premiums |

Explore related products

What You'll Learn

- Private mortgage insurance (PMI) protects the lender, not the borrower

- PMI is required for down payments of less than 20%

- PMI is usually paid monthly, but can be included in upfront costs

- PMI cancellation is required when the borrower has paid off 80% of the loan

- Overcharging for PMI has been a long-standing issue, despite Congress passing the Homeowners Protection Act in 1998

![]()

Private mortgage insurance (PMI) protects the lender, not the borrower

Private mortgage insurance (PMI) is a type of insurance that you may be required to buy if you take out a conventional loan with a down payment of less than 20% of the purchase price or loan amount. It is meant to protect the lender, not the borrower, from losses if the borrower defaults on their loan. The borrower can request their lender to cancel the PMI once they have built up at least 20% equity in their home or when the outstanding loan amount drops below 80% of the home's value.

PMI is typically required for conventional loans with a low down payment because borrowers who make smaller down payments historically default on mortgages at higher rates. By requiring PMI, the lender can reduce their risk and qualify for a loan that they might not have otherwise gotten. However, it is important to note that PMI does not protect the borrower; if they fall behind on their payments, they can still lose their home through foreclosure.

The cost of PMI can vary depending on factors such as the loan amount, credit score, and type of PMI. Borrower-paid PMI is the most common type, where the premiums are part of the monthly mortgage payment. Lender-paid PMI, on the other hand, is paid by the lender but results in a higher interest rate on the loan. There is also split-premium PMI, where the borrower pays a larger upfront fee and the remainder with their monthly payment.

While PMI can help borrowers qualify for loans, it is not without its controversies. There have been instances of borrowers being overcharged or unfairly charged for PMI, with some companies continuing to collect premiums even after the policy should have been canceled. To address this issue, the Homeowners Protection Act was passed in 1998, and the Consumer Financial Protection Bureau has issued bulletins reminding mortgage insurers and servicers to comply with the law.

Deceased Home Insurance: What to Do?

You may want to see also

Explore related products

![]()

PMI is required for down payments of less than 20%

Private Mortgage Insurance (PMI) is a type of insurance that protects lenders against loss if a borrower defaults. It is typically required for borrowers who make a down payment of less than 20% of the purchase price of the home. This is because borrowers who make smaller down payments have historically defaulted on mortgages at higher rates. By requiring PMI, lenders can lower their risk and qualify borrowers for loans that they might not otherwise be able to get.

PMI rates vary by down payment amount and credit score but are generally cheaper for borrowers with good credit. It can be paid through an upfront premium (which can be financed into the loan) and then monthly payments, or through both upfront and monthly premiums. The upfront premium is shown on the Loan Estimate and Closing Disclosure, while the monthly premium is included in the monthly mortgage payment.

Borrowers can request their lender to cancel PMI monthly payments once the outstanding loan amount drops below 80% of the home's value. This typically requires a professional appraisal to support the request. It's important to note that PMI does not protect borrowers, and they can still lose their home through foreclosure if they fall behind on payments.

While PMI can help borrowers qualify for loans, it increases the overall cost of the loan. Overcharging for PMI has been a long-standing issue, and consumers should be aware of their rights to avoid being billed for unnecessary insurance. The Homeowners Protection Act passed by Congress in 1998 forbids the practice of charging PMI after the date when a policy should be automatically canceled.

Roadside Rescue: Exploring Farmers Insurance's Roadside Assistance Offerings

You may want to see also

Explore related products

![]()

PMI is usually paid monthly, but can be included in upfront costs

Private Mortgage Insurance (PMI) is an insurance policy that protects the lender or title holder in the event of the borrower defaulting on payments, dying, or being unable to meet their mortgage obligations. It is usually required by the lender if the loan amount is more than 80% of the property's selling price. PMI is typically paid monthly, but there is usually also an upfront premium that can be financed into the loan. The upfront premium is shown on the Loan Estimate and Closing Disclosure, and the monthly premium is shown in the Projected Payments section.

The monthly PMI premiums are added to your mortgage payment. Your insurance company should cancel them automatically when your principal balance is scheduled to fall below 78% of the home's original value. If PMI is not cancelled automatically, you can request to have it cancelled in writing. You can also request cancellation if you have made extra payments that bring the balance to 80% early.

The upfront premium for PMI can be paid at closing, but if you don't have enough cash to pay it upfront, you can roll it into your mortgage. This will increase your loan amount and overall costs. With VA-backed loans, for example, there is no monthly PMI premium, but there is an upfront "funding fee" that can be rolled into the mortgage. Similarly, FHA and USDA loans require an upfront cost that can be paid as part of closing costs or rolled into the loan balance, increasing the overall cost of the loan.

PMI is required when the down payment on a home is less than 20%. This is because borrowers who make smaller down payments have higher rates of defaulting on mortgages. By paying PMI, borrowers can qualify for loans that they may not otherwise be eligible for. However, PMI increases the cost of the loan and only protects the lender, not the borrower.

Updating Escrowed Insurance: A Guide for Mortgage Holders

You may want to see also

Explore related products

![]()

PMI cancellation is required when the borrower has paid off 80% of the loan

Private Mortgage Insurance (PMI) is a type of insurance that protects lenders against loss if a borrower defaults on their loan. It is usually required by the lender if the borrower's loan amount is more than 80% of the loan-to-value amount. This means that borrowers who make a down payment of less than 20% of the purchase price of the home are typically required to buy PMI. This is because borrowers who make smaller down payments have higher rates of defaulting on their mortgages.

PMI cancellation is required when the borrower has paid off enough of the loan to reach 20% equity in their home, or when the outstanding loan amount drops below 80% of the loan-to-value amount. The date when the borrower is expected to reach this threshold should be listed on their PMI disclosure form or in their loan's amortization table. If the borrower pays off more than 80% of the loan ahead of schedule, they can request to cancel PMI sooner.

It is important to note that PMI cancellation requests must be made in writing, and borrowers should be prepared to provide documentation and meet specific requirements. These may include proving that their home has gained value through a home appraisal or broker price opinion (BPO). Additionally, borrowers should be current on their loan payments and have a history of on-time payments to ensure a smooth exit from PMI.

Failing to cancel PMI when the borrower has reached the required threshold can lead to significant unnecessary costs for the borrower. It is the borrower's responsibility to be aware of their rights and request PMI cancellation when eligible, as some PMI companies or mortgage service firms may continue to collect premiums even after the policy should be canceled.

Insurance, Mortgage, and Economy: What You Need to Know

You may want to see also

Explore related products

![]()

Overcharging for PMI has been a long-standing issue, despite Congress passing the Homeowners Protection Act in 1998

Private mortgage insurance (PMI) is a type of insurance that protects lenders against loss if a borrower defaults. It is usually required by the lender if the loan amount is more than 80% of the loan-to-value amount. The borrower can request the lender to cancel the PMI once the outstanding loan amount is below 80% of the loan-to-value amount.

Overcharging for PMI has been a long-standing issue. In 1998, Congress passed the Homeowners Protection Act (HPA), also known as the PMI Cancellation Act, to address this issue. The HPA established guidelines for the mandatory termination of PMI when the principal balance reaches 80% of the original value of the property securing the mortgage loan. It also requires the return of unearned premiums and prescribes disclosure requirements for PMI amortization schedules.

Despite the HPA, overcharging for PMI has continued to be a problem. Since 2013, the Consumer Financial Protection Bureau (CFPB) has issued several bulletins reminding mortgage insurers and servicers to stop collecting premiums after borrowers' obligations are paid. However, some companies have still failed to comply with the law, resulting in homeowners paying unnecessary PMI premiums.

The CFPB has attributed the problem to industry confusion and has issued guidance to servicers to comply with the law. Paying for unnecessary PMI is a serious burden for homeowners, and it is essential that borrowers are aware of their rights and protections under the HPA to avoid being overcharged for PMI.

Mortgage Insurance: Is It a Must-Have?

You may want to see also

Frequently asked questions

Private mortgage insurance (PMI) is a type of insurance that you may be required to buy if you take out a conventional loan with a down payment of less than 20% of the purchase price. PMI protects the lender, not the borrower, against loss if the borrower defaults on payments.

Mortgage insurance may come with a typical monthly premium payment or be paid as a lump sum at the time of mortgage origination. The monthly PMI premiums are added to your mortgage payment.

You can request to have your PMI cancelled if your outstanding loan amount drops below 80% of the home's original value. You'll need to be up-to-date on your home payments and make the request to cancel PMI in writing.