Homeowners in Texas are facing a challenging situation due to the steep rise in insurance rates, which have soared to more than triple the national average in some cases. This trend has been attributed to various factors, including the state's vulnerability to weather-related disasters, such as hurricanes, hail storms, and tornadoes, which result in costly property damage. Additionally, escalating construction costs, labour shortages, stricter building codes, and increased material expenses contribute to higher rebuilding costs, impacting insurance premiums. Texas also experiences high property crime rates, influencing insurance rates. The state's insurance regulatory system has been criticized as weak, allowing insurance companies to implement frequent and substantial rate increases. These rising costs are affecting the housing market and the ability of Texans to secure affordable coverage, with some fearing homeowners may be driven out of the state.

| Characteristics | Values |

|---|---|

| Susceptibility to weather-related natural disasters | Hurricanes, tornadoes, hail storms, wind storms, and wildfires |

| Property crime rates | Theft, vandalism, and home invasion |

| Construction costs | Rising costs of materials and labor |

| Regulatory system | "File and use" system |

| Insurance companies | Ability to absorb losses and make profits |

| Population | Booming population, especially in high-risk areas |

| Inflation | Impact on insurance premiums |

| Claims activity | Frequency and severity of claims |

Explore related products

$10.75 $13.97

What You'll Learn

![]()

Texas weather patterns

Texas is susceptible to weather-related natural disasters due to its unique geographical location. The state's lengthy coastal border is exposed to hurricane threats, and it is also situated in Tornado Alley, where it encounters an average of 132 tornadoes each year. Certain areas, such as counties in East and Southeast Texas, including Houston, are particularly vulnerable to these weather events.

The state experiences a diverse range of weather patterns and climatic conditions. The region of South Texas includes the semi-arid ranch country and the wetter Rio Grande Valley. The coastal areas enjoy warm temperatures year-round due to the currents of the Gulf of Mexico, with hot and humid summers. The wettest months in the western areas are April and May, while September becomes the wettest month closer to the Gulf Coast due to the threat of tropical weather systems, including hurricanes.

Texas is no stranger to extreme weather events. The state experienced a record-breaking cold snap in February 2021, with temperatures remaining at or below freezing for extended periods in cities like Austin and Abilene. The state is also prone to significant flooding, with a history of tropical cyclones and stalled weather fronts causing substantial impacts. The Northern Plains of Texas have a semi-arid climate, making it susceptible to droughts, and it experiences a significant range of temperatures, with winter nights often dropping below freezing.

The diverse and often extreme weather patterns in Texas contribute to the high homeowners insurance rates in the state. The frequency and severity of weather-related disasters, including hurricanes, hail storms, and tornadoes, increase the risk of property damage and drive up insurance costs. The potential for catastrophic loss and the subsequent increase in rebuilding costs significantly influence the insurance premiums that Texas homeowners have to bear.

Homeowners Insurance: Wind-Damaged Roof Coverage

You may want to see also

Explore related products

$15.95 $15.95

$19.99

![]()

Construction costs

Texas is prone to destructive weather events, including hurricanes, hail storms, and tornadoes, which cause significant property damage and subsequently increase insurance costs. However, one of the key factors contributing to high homeowners insurance rates in Texas is the escalating construction costs in the state.

Labor shortages in Texas have led to increased labor costs, affecting the overall construction process and driving up the price of rebuilding homes. This, in turn, influences insurance companies to raise their premiums to cover these higher expenses.

In addition to labor costs, the price of construction materials has soared, further exacerbating the challenge of rebuilding homes after natural disasters. The combination of higher labor costs and material expenses results in more expensive insurance claims, which insurance companies then pass on to homeowners through elevated premiums.

Stricter building codes in Texas also play a role in the rising construction costs. These codes mandate the use of additional construction measures and higher-quality materials, leading to increased rebuilding expenses. As a result, insurance companies adjust their rates to account for the higher costs associated with adhering to these stricter standards.

To mitigate the financial burden on homeowners, Texas lawmakers are considering legislative actions, such as transitioning to an approval process similar to California's, which would grant the state more control over rate increases. Additionally, bills are being proposed to address the cost of constructing more resilient homes that can withstand severe weather events, potentially reducing insurance costs.

Hospital Indemnity Insurance: A Smart Move for Pregnancy?

You may want to see also

Explore related products

![]()

Crime rates

Texas has some of the highest homeowners insurance rates in the country. While there are several factors contributing to this, property crime rates in Texas also play a role in shaping homeowners insurance premiums. Insurance companies take into account the heightened risk of theft, vandalism, and home invasion when determining premiums. Vandalism, in particular, can significantly impact property crime rates, resulting in elevated insurance premiums for homes susceptible to this type of crime. The frequency of insurance claims contributes to the state’s high housing insurance costs. These aspects lead to increased costs for insurance companies, which are then passed on to homeowners through higher premiums.

The legal system in Texas, along with the frequency of insurance claims and lawsuits, has led to Texas gaining a reputation that directly affects annual premiums. Texas homeowners can qualify for discounts on home insurance by installing safety measures such as home security systems, fire extinguishers, and smoke detectors. Implementing these measures can help reduce the risk of property crimes and lower insurance premiums.

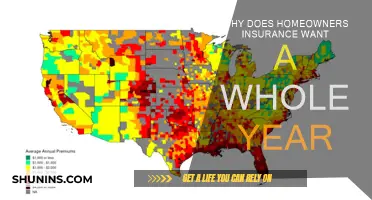

The state's susceptibility to weather-related natural disasters, such as hurricanes, hail storms, and tornadoes, also contributes to higher insurance rates. The potential for severe damage from these events increases the cost of rebuilding homes, impacting insurance costs. The Houston metropolitan area, for example, has the highest average premiums in the state, with communities closest to the coast paying nearly three times the national average for home insurance.

The combination of property crime rates, the legal system, and natural disasters creates a challenging environment for homeowners in Texas, resulting in higher insurance premiums. Homeowners can explore various strategies, such as maximizing discounts and deductibles, to mitigate the impact of high insurance rates.

Private Mortgage Insurance: Good or Bad for You?

You may want to see also

Explore related products

![]()

Insurance companies' profits

Texas homeowners insurance rates have been steadily increasing, with some homeowners reporting that their insurance premiums have tripled in a year. This has been attributed to a variety of factors, including the state's susceptibility to weather-related natural disasters, escalating construction costs, and property crime rates. While these factors have undoubtedly contributed to the high cost of insurance in Texas, it is also important to consider the role of insurance companies' profits in driving up premiums.

Insurance companies in Texas have been operating at a loss for several years due to the high frequency and severity of weather-related disasters. Texas is prone to hurricanes, hail storms, tornadoes, and wildfires, which can cause extensive property damage and lead to costly insurance claims. From 2018 to 2022, the five-year average loss ratio for Texas home insurance companies was 102%, indicating that insurers paid out more in claims than they received in premiums. This has led to concerns about insurance companies passing on their costs to consumers through higher premiums.

In 2023, insurance companies in Texas requested double-digit rate increases more than 150 times, with one company asking for an increase of 73%. The number of double-digit rate increase requests has increased by 560% since 2014. While insurance companies argue that these increases are necessary to cover their losses, consumer advocates argue that the current regulatory system in Texas is weak and oriented towards insurance companies, allowing them to charge excessive rates.

The "file and use" system in Texas allows insurance companies to implement newly proposed rates without prior approval from the state. Consumer advocates, such as Texas Watch, have called for an end to this system and the adoption of a "prior approval" process, which would require the insurance commission to approve rate increases before they take effect. They argue that the current system leads to excessive profits for insurance companies and unaffordable premiums for consumers.

While insurance companies do need to make profits to remain in operation, the impact of continuously rising insurance rates on Texas homeowners cannot be ignored. The high cost of insurance is not only a financial burden but also a factor in the state's housing market and affordability. As insurance rates continue to climb, some homeowners may be driven out of the state or struggle to find coverage, as insurance companies may become more selective in the policies they offer.

Natural Disasters and Farmers: Navigating the Complex World of Agricultural Insurance

You may want to see also

Explore related products

![]()

Population growth

Texas has experienced a population boom in recent years, which has contributed to rising homeowners' insurance rates in the state. As more people move to Texas, the demand for housing increases, leading to a surge in property values. This, in turn, raises the cost of insuring homes and businesses, as insurance companies take into account the higher property values when determining premiums.

The population growth in Texas has also led to an increase in the number of people living in areas prone to severe weather events, such as hurricanes, hail storms, and tornadoes. Texas is particularly susceptible to these natural disasters due to its geographical location, including its lengthy coastal border and its position within Tornado Alley. The frequency and intensity of storms and other weather events have also been intensified by climate change, resulting in more frequent and costly property damage claims.

The combination of population growth and the increased frequency and severity of natural disasters has put pressure on the insurance market in Texas. Insurance companies have responded by raising premiums to cover the cost of expected losses. Additionally, the high population growth in Texas has led to labour shortages and increased material expenses, which contribute to higher rebuilding costs after disasters. These factors have further driven up the cost of homeowners' insurance in the state.

Furthermore, the growing population in Texas has resulted in an increase in property crime rates, including theft, vandalism, and home invasions. Insurance companies consider the heightened risk of these crimes when setting premiums, leading to higher insurance rates for homeowners. The legal system in Texas and the frequency of insurance claims and lawsuits have also contributed to the state's reputation, which directly affects annual insurance premiums.

While the population boom in Texas is a significant factor in the increase in homeowners' insurance rates, it is not the only reason. The frequency and severity of weather events, labour and construction costs, and property crime rates are also contributing factors. The insurance regulatory system in Texas, known as "file and use," allows insurance companies to change rates with minimal scrutiny, which has led to concerns about excessive profit-making by insurance companies. However, some argue that the current system enables a competitive market, which benefits consumers. Overall, the combination of these factors has resulted in Texas homeowners facing some of the highest insurance premiums in the country.

Home Insurance: What Views Are Protected?

You may want to see also

Frequently asked questions

Texas is susceptible to weather-related natural disasters, including hurricanes, hail storms, and tornadoes, which increase the risk of property damage. The frequency and severity of storms and weather events have increased, contributing to higher insurance rates.

The high frequency of storms and weather events leads to a higher number of insurance claims, which is the main factor for increasing home insurance costs in Texas. The cost of rebuilding homes after disasters has also increased due to escalating construction costs, labor shortages, and increased material expenses.

Yes, property crime rates, including theft, vandalism, and home invasion, are also considered when determining insurance premiums in Texas. Additionally, the state's legal system and the frequency of lawsuits have contributed to higher insurance rates.

Homeowners can maximize discounts and deductibles, such as installing security measures and combining policies. Shopping around for the lowest rates and avoiding minor insurance claims can also help lower insurance premiums. Texas lawmakers are also working on addressing the rising costs of homeowners insurance.