Insurance companies are pushing for quality risk management to enhance operational efficiency, mitigate risks, and deliver superior value to policyholders and stakeholders. By addressing typical quality issues, such as inaccurate underwriting decisions, claims processing delays, fraudulent claims, inadequate risk assessment, and cybersecurity risks, insurers can build trust with customers, manage risks effectively, and maintain a competitive advantage. In an evolving landscape, proactive measures, continuous improvement, and a commitment to ethical conduct and customer-centricity are key for long-term success. With the emergence of gen AI and advancing technology, insurers have the opportunity to transform distribution, enhance decision-making, and provide tailored insurance contracts that meet the needs of their clients. However, managing the risks associated with advanced analytics and gen AI requires skilled personnel and a comprehensive understanding of the evolving risk landscape.

| Characteristics | Values |

|---|---|

| Protecting individuals, businesses, and organizations | Financial losses and liabilities |

| Ensuring quality and reliability | Building trust with customers, managing risks effectively, and maintaining competitive advantage |

| Addressing typical quality issues | Inaccurate underwriting decisions, claims processing delays, fraudulent claims, inadequate risk assessment, regulatory compliance challenges, inefficient customer service, product complexity, lack of pricing transparency, and cybersecurity risks |

| Gen AI | A disrupting force to the traditional business model and a powerful tool for underwriters, claims managers, and distribution leaders |

| Macroeconomic conditions | Regulatory requirements, accounting standards, and competitive landscape |

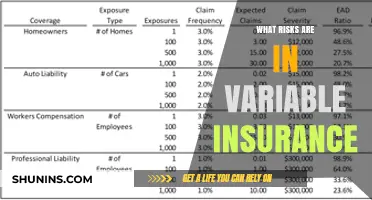

| Cyber risk | System failure, ransomware, and business email compromise |

| Risk management frameworks | NIST's Risk Management Framework, ISACA's COBIT 2019, and the Risk and Insurance Management Society's Risk Maturity Model (RMM) |

| Risk management approach | Transactional vs. transformational, with the former treating risk management as an insurance policy |

| Key concepts of risk management | Risk identification, risk analysis, risk acceptance, and risk communication |

| Benefits of risk-based thinking | Proactivity in managing risks, identification of opportunities for improvement, and a culture of continuous improvement |

Explore related products

What You'll Learn

- To protect individuals, businesses, and organisations from financial losses and liabilities

- To enhance operational efficiency, mitigate risks, and deliver superior value to policyholders and stakeholders

- To build trust with customers and maintain a competitive advantage

- To address unstructured data and improve data quality with gen AI

- To ensure cyber protection and support in the event of a cyber incident

![]()

To protect individuals, businesses, and organisations from financial losses and liabilities

The insurance and risk management industry is crucial for protecting individuals, businesses, and organisations from financial losses and liabilities. However, it is a complex and highly regulated sector, which presents challenges that can impact customer satisfaction, risk mitigation, and business success.

Insurers and risk managers must address typical quality issues to enhance operational efficiency, mitigate risks, and deliver superior value to policyholders and stakeholders. These issues include inaccurate underwriting decisions, claims processing delays, fraudulent claims, inadequate risk assessment, regulatory compliance challenges, inefficient customer service, product complexity, lack of pricing transparency, and cybersecurity risks.

By implementing proactive measures, a commitment to continuous improvement, ethical conduct, and customer-centricity, the industry can navigate these challenges and seize opportunities for long-term success. For example, addressing inaccurate underwriting decisions involves implementing robust underwriting guidelines, leveraging data analytics for risk profiling, providing ongoing training for underwriters, and conducting regular audits.

Additionally, the emergence of Gen AI presents both opportunities and challenges for the insurance industry. Gen AI can help insurers understand client risk profiles in greater depth and produce more tailored insurance contracts. It can also enhance decision-making by summarising documentation, improving policy information, and automating data operations. However, it presents risks related to fairness, intellectual property, privacy, and security that need to be managed effectively.

Ultimately, by addressing quality issues and embracing technological advancements, the insurance and risk management industry can better protect individuals, businesses, and organisations from financial losses and liabilities.

Commercial Insurance: BCBS vs Highmark

You may want to see also

Explore related products

![]()

To enhance operational efficiency, mitigate risks, and deliver superior value to policyholders and stakeholders

The insurance industry plays a crucial role in safeguarding individuals, businesses, and organizations from financial losses, liabilities, and risks. To enhance operational efficiency, mitigate risks, and deliver superior value to policyholders and stakeholders, insurance providers must proactively address typical quality issues.

Inaccurate underwriting decisions, claims processing delays, fraudulent claims, inadequate risk assessment, regulatory compliance challenges, inefficient customer service, product complexity, lack of pricing transparency, and cybersecurity risks are among the challenges that insurers face. By tackling these issues, insurance companies can improve their operational efficiency and risk management capabilities.

For instance, implementing robust underwriting guidelines, leveraging data analytics and predictive modeling for risk profiling, providing ongoing training for underwriters, and conducting regular audits can enhance decision-making and mitigate risks. Additionally, emerging technologies like Gen AI offer transformative opportunities for the insurance sector. Gen AI can improve data extraction, automate operations, and enable insurers to create tailored insurance contracts that meet the unique needs of their clients.

Furthermore, to deliver superior value to policyholders and stakeholders, insurance companies must continuously improve and adapt to the evolving landscape. This includes addressing challenges related to macroeconomic conditions, regulatory requirements, accounting standards, and the competitive landscape. By proactively managing risks and embracing innovation, insurance providers can enhance their operational efficiency and better serve their customers.

In summary, by addressing quality issues, embracing technological advancements, and adapting to changing market conditions, insurance companies can enhance their operational efficiency, mitigate risks, and deliver superior value to both policyholders and stakeholders.

Commercial Building Insurance: A Shopping Guide

You may want to see also

Explore related products

![]()

To build trust with customers and maintain a competitive advantage

Quality and reliability are paramount for insurance companies to build trust with customers and maintain a competitive advantage. The insurance and risk management industry plays a vital role in protecting individuals, businesses, and organizations from financial losses and liabilities. Ensuring quality in this complex and highly regulated sector is challenging, and issues such as inaccurate underwriting decisions, claims processing delays, fraudulent claims, inadequate risk assessment, and inefficient customer service can impact customer satisfaction and business success.

By addressing these quality issues, insurers can enhance operational efficiency and deliver superior value to policyholders. This involves implementing robust underwriting guidelines, leveraging data analytics for risk profiling, and providing ongoing training to improve decision-making skills. With the emergence of Gen AI, insurers can now utilize this technology to understand their clients' in-depth risk profiles and produce more tailored insurance contracts. Gen AI can also enhance decision-making by summarizing documentation, improving policy information, and automating data extraction.

In addition to technological advancements, insurance companies must also adapt to changing macroeconomic conditions, regulatory requirements, and evolving risks. For example, cyber risk is a top exposure for companies of all sizes, and insurers must work closely with their clients to meet their needs in this dynamic landscape. By integrating risk management into their quality management systems, insurance companies can identify opportunities for improvement and drive towards excellence.

Ultimately, by prioritizing quality risk management, insurance companies can build trust with their customers by demonstrating their ability to manage risks effectively and adapt to changing conditions. This trust forms the foundation of a competitive advantage, setting them apart from competitors and solidifying their position in the market.

Lounge Act Singer in Progressive Insurance Ad

You may want to see also

Explore related products

![Compliance [Blu-ray]](https://m.media-amazon.com/images/I/712fZO6aOlL._AC_UY218_.jpg)

![]()

To address unstructured data and improve data quality with gen AI

The insurance industry is facing a range of challenges, including regulatory changes, emerging risks, and increasing demand for coverage. Insurers are also under pressure to improve operational efficiency, enhance customer satisfaction, and maintain their competitive advantage. As a result, they are turning to quality risk management practices to address these issues and ensure long-term success.

Quality risk management in insurance involves addressing typical issues such as inaccurate underwriting decisions, claims processing delays, fraudulent claims, inadequate risk assessment, and inefficient customer service. By improving these areas, insurers can mitigate risks and provide superior value to their customers and stakeholders.

Gen AI has emerged as a potential solution to transform the insurance industry, particularly in addressing unstructured data and improving data quality. Unstructured data, such as emails, contracts, recordings, and other forms of proprietary content, can be effectively utilized by gen AI to gain distinctive insights and improve decision-making.

- Define clear objectives: Before implementing gen AI, insurance companies should define their core business problems and goals. Whether it's improving customer experience, optimizing processes, or generating new insights, having clear objectives guides the effective use of gen AI.

- Invest in data quality solutions: Insurance companies can utilize tools like AI4DQ Unstructured, which offers correction strategies and actionable insights to improve the quality of unstructured data. This enhances the accuracy and consistency of gen AI results.

- Automate data management: Manually cleaning and organizing data is time-consuming and prone to errors. Automation tools, such as Shelf's unstructured data management platform, can identify inconsistencies, flag duplicates, and ensure data meets quality standards, improving the reliability of gen AI outputs.

- Expand data collection: Gen AI thrives on a diverse and extensive range of high-quality data. Insurance companies should evaluate their data sources and expand their data collection efforts to capture a comprehensive view of their customers, operations, and business environment.

- Leverage natural language processing (NLP): NLP tools enable gen AI to understand and extract insights from human language in unstructured data sources. By leveraging NLP, insurance companies can transform raw text into useful data, enhancing the AI's understanding of their business and improving the accuracy of results.

- Maintain data consistency: Ensuring data consistency across systems is crucial. Insurance companies should standardize and update customer records to prevent confusion and enable their gen AI to provide accurate and useful insights.

- Prioritize ongoing data management: Data management is an ongoing process. Insurance companies should maintain data quality, break down data silos, and ensure privacy to adapt to evolving business needs and stay competitive.

By addressing unstructured data and improving data quality with gen AI, insurance companies can enhance their risk management practices, make more informed decisions, and ultimately provide better services to their customers.

Commercial Insurance Brokers: Are They All Equal?

You may want to see also

Explore related products

![]()

To ensure cyber protection and support in the event of a cyber incident

The insurance industry plays a critical role in protecting individuals, businesses, and organizations from financial losses and liabilities. With the rise of cyber risks, insurance companies are increasingly focused on providing cyber protection and support to their customers in the event of a cyber incident.

Cyber risk management is an ongoing process of identifying, analyzing, evaluating, and addressing cybersecurity threats. It involves developing robust policies and tools to assess and mitigate vendor risk, identifying internal weaknesses, and ensuring regulatory compliance. By implementing effective cyber risk management practices, insurance companies can enhance their decision-making capabilities and better protect their customers from cyber threats.

In today's interconnected world, organizations face diverse and sophisticated cyber threats that have far-reaching impacts. With the increasing utilization of technology, remote work, and reliance on cloud sharing and video conferencing tools, the opportunities for system failure and cyberattacks have multiplied. As such, insurance companies must stay ahead of the curve by adopting proactive measures and staying committed to ethical conduct and customer-centricity.

To ensure cyber protection and provide support in the event of a cyber incident, insurance companies can take several key actions. Firstly, they can implement robust underwriting guidelines and risk assessment criteria. This involves leveraging data analytics and predictive modeling to thoroughly understand the risk profiles of their clients and create tailored insurance contracts that suit their specific needs. By conducting comprehensive risk assessments, insurance companies can identify potential vulnerabilities and implement targeted security measures to strengthen their cyber defenses.

Additionally, insurance companies can provide ongoing training and support to their customers to enhance their cyber resilience. This may include educating customers about cybersecurity best practices, raising awareness about common cyber threats, and offering guidance on how to respond to and recover from a cyber incident. By empowering their customers with knowledge and resources, insurance companies can help them become active participants in managing their cyber risks.

Furthermore, insurance companies can forge partnerships with specialized cyber security vendors and experts. By leveraging the expertise of these vendors, insurance companies can enhance their cyber protection capabilities and offer more comprehensive support to their customers in the event of a cyber incident. These partnerships can provide access to advanced cyber security tools, incident response protocols, and forensic investigation services, ensuring a more robust response to cyber threats.

In conclusion, insurance companies are pushing for quality risk management to build trust with their customers and maintain their competitive advantage. By prioritizing cyber protection and support, they can effectively safeguard their customers from the financial and operational repercussions of cyber incidents. Through a combination of comprehensive risk assessments, tailored insurance contracts, customer education initiatives, and strategic partnerships, insurance companies can fortify their cyber defenses and offer invaluable support to their customers in navigating the evolving landscape of cyber risks.

Burnie Burns' Surprising Appearance in a General Insurance Ad

You may want to see also

Frequently asked questions

Quality risk management is essential for insurance companies to build trust with their customers, manage risks effectively, and maintain a competitive advantage. By addressing typical quality issues such as inaccurate underwriting decisions, claims processing delays, fraudulent claims, inadequate risk assessment, and cybersecurity risks, insurance companies can enhance operational efficiency and deliver superior value to their policyholders.

Risk management enables insurance companies to identify, analyze, and assess risks systematically. By understanding the likelihood and potential impact of risks, insurance companies can implement preventive actions, make informed decisions, and protect themselves and their customers from financial losses and liabilities.

Integrating risk management into a QMS promotes a proactive approach to managing risks. It helps identify opportunities for improvement, drives a culture of continuous improvement, and enables insurance companies to achieve quality excellence. By considering risks throughout their processes, insurance companies can prevent or mitigate issues rather than simply reacting to them.

![Law of Governance, Risk Management and Compliance: [Connected Ebook] (Aspen Casebook)](https://m.media-amazon.com/images/I/616gNHR5shL._AC_UY218_.jpg)