In the United States, health insurance has traditionally been regulated by individual State Insurance Commissioners, resulting in varying regulations and premium rates across states. While some have advocated for allowing insurance sales across state lines to increase competition and drive down prices, others argue that it is unlikely to lower costs or improve choice. Critics highlight potential unintended consequences, such as market segmentation and adverse selection, which could threaten the viability of insurers and compromise the ability of high-risk individuals to obtain coverage. To sell across state lines, insurers must also navigate provider networks and establish reimbursement agreements, potentially impacting their ability to offer lower prices in adjacent states. While Republican health reform proposals often include selling insurance across state lines, the reality of its impact on the complex US healthcare system remains uncertain.

| Characteristics | Values |

|---|---|

| Who is in favor of selling insurance across state lines | Republicans, Trump Administration, Biden-Harris Administration |

| Who is against it | The Commonwealth Fund, American Academy of Actuaries |

| Why in favor | To increase consumer choice, promote competition and drive down prices in the health insurance market |

| Why against | It is unlikely to lower costs or increase competition, may threaten the viability of insurers licensed in states with strict benefit coverage, may compromise the ability of high-risk individuals to obtain coverage |

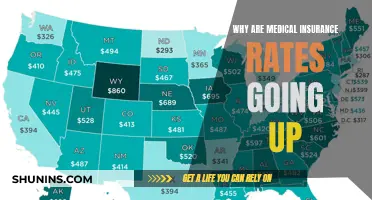

| Current status | Six states—Georgia, Kentucky, Maine, Rhode Island, Washington, and Wyoming—have passed laws permitting cross-state insurance sales, but no states have joined them, and no insurers have expressed interest |

Explore related products

What You'll Learn

- Interstate sales of health insurance may not lower costs or increase competition

- Insurers selling across state lines may not comply with the regulations of each state

- Selling insurance across state lines may threaten the viability of insurers in some states

- Health insurance has historically been regulated by individual State Insurance Commissioners

- Selling insurance across state lines may eliminate the ability of insurance regulators to assist consumers

![]()

Interstate sales of health insurance may not lower costs or increase competition

If insurers were allowed to sell health insurance across state lines, they would have to comply with the regulations of each state they sold in, which could be costly and time-consuming. This could also lead to a situation where insurers only sell in states with favourable regulations, reducing competition and choice for consumers.

Furthermore, the ACA created a more uniform system of rules for health insurers, requiring them to offer a plan to anyone who applies and prohibiting them from excluding coverage of pre-existing health conditions. It also placed limits on what people can be charged based on their health, gender, or age and required that every plan offer a set of "essential benefits," such as preventive services and maternity care. These protections would be at risk if insurers were allowed to sell across state lines, as they could choose to only comply with the regulations of one state, which may have weaker consumer protections.

In addition, there is a risk that if the ACA’s insurance reforms are repealed, and Congress enacts legislation to mandate cross-state sales, it could lead to adverse selection in many states. Without a federal minimum standard of protections, some multistate insurers with national or regional networks could take advantage of exemptions from state standards for benefit design, premium rating, and other consumer protections. This would enable them to attract younger and healthier enrollees, threatening the long-term viability of local insurers, increasing premiums, and reducing consumers’ choices.

Finally, insurers have not expressed interest in selling health insurance plans across state lines. This may be because the current regulatory framework does not make it financially viable for them to do so. Therefore, allowing the interstate sale of health insurance may not result in lower costs or increased competition, as there may not be enough insurers participating to drive down prices and provide more choices for consumers.

Get Medical Insurance in Maryland: Eligibility and Timing

You may want to see also

Explore related products

![]()

Insurers selling across state lines may not comply with the regulations of each state

In the United States, health insurance has historically been regulated by individual State Insurance Commissioners. Prior to the Affordable Care Act (ACA), there was significant variation between states in terms of how insurance companies were regulated and how premium rates were determined to be reasonable. Mandated benefits, medical underwriting requirements, and rating rules differed from state to state. Some states, for instance, required minimum loss ratios to be measured over a year, while others required minimum loss ratios over the policy's lifetime.

The ACA created a more uniform system of rules for health insurers, standardizing regulations and minimizing differences between states. However, the regulation of health products and premium rates is still largely managed by individual states and their respective insurance departments.

Under some Republican health reform proposals, insurance companies would be able to sell their policies across state lines. As long as a health plan complied with any one state's regulations, it could then be sold nationwide without necessarily complying with the regulations of each state. This could result in insurers attracting healthier residents from other states, while states with more comprehensive benefit requirements would attract less healthy enrollees. Consequently, premiums for insurance in states with more comprehensive requirements would increase, threatening the viability of insurers in those states. As a result, individuals with health problems could find it more challenging to obtain coverage.

Allowing insurers to sell coverage across state lines may lead to unintended consequences, such as market segmentation and adverse selection, threatening the ability of high-risk individuals to obtain insurance. While it is argued that selling insurance across state lines could lower costs by creating a competitive national marketplace, this theory assumes that insurance companies would lower their prices in states with higher rates. In reality, premium rates are based on the cost of care in the service area, and any savings from differences in benefit coverage requirements between states may be negligible compared to savings achieved through strong provider contracts.

Delta Therapy: Understanding Medical Insurance Coverage

You may want to see also

Explore related products

$34.95 $34.95

$9.99 $19.99

![]()

Selling insurance across state lines may threaten the viability of insurers in some states

Allowing insurers to sell coverage across state lines could result in unintended consequences, threatening the viability of insurers in some states. This is because insurers licensed in states with more comprehensive benefit requirements would attract less-healthy enrollees, while those in states with less restrictive rules would attract younger and healthier enrollees. As a result, premiums for insurance licensed in states with more comprehensive benefit requirements would increase, threatening the viability of those insurers. Consequently, individuals with health problems could find it more challenging to obtain coverage, and market segmentation could occur.

Prior to the Affordable Care Act (ACA), state insurance regulations varied significantly. States differed in the extent of medical underwriting they allowed, their "guaranteed issue" requirements regarding people with pre-existing conditions, and their rules on coverage denials for specific medical conditions. Insurers had to comply with each state's insurance regulations to sell policies in multiple states. The ACA created a more uniform system of rules for health insurers, standardizing regulations, and minimizing differences between states.

Some proponents of cross-state insurance sales argue that insurers could lower prices in adjacent states with higher rates, benefiting consumers. However, this assumes that insurance companies will pass on any cost savings to consumers, which may not always be the case. Additionally, while cross-state sales might increase competition and lower premiums, they are unlikely to improve consumers' choices significantly. Furthermore, selling insurance across state lines could eliminate the ability of insurance regulators to assist consumers with issues related to their health insurance purchases.

Currently, the ACA allows insurers to sell policies across state lines in states that have joined "health care choice compacts." Six states have passed laws permitting such compacts, but no states have joined them, and no insurers have expressed interest in selling plans under this arrangement. While Republican health reform proposals aim to eliminate most of the ACA's national regulations to make it easier for insurers to sell across state lines, it is unclear if this will fulfill the promise of encouraging health insurance sales across state lines and improving consumer choices or lowering premiums.

Medicaid QMB: Insurance Copays and What They Mean for You

You may want to see also

Explore related products

![]()

Health insurance has historically been regulated by individual State Insurance Commissioners

Health insurance in the US has traditionally been regulated by individual State Insurance Commissioners. Before the Affordable Care Act (ACA) was passed in 2010, state insurance regulations varied widely. The states differed in the extent of medical underwriting they allowed, in their "guaranteed issue" requirements regarding people with pre-existing conditions, and in permitting or preventing coverage denials for certain medical conditions. To sell policies in multiple states, insurers had to comply with each state's insurance regulations.

The ACA created a more uniform system of rules for health insurers. It provided a regulatory floor for health plans sold to individuals across all 50 states by requiring insurers to offer a plan to anyone who applies, prohibiting insurers from excluding coverage of pre-existing health conditions, placing limits on what people can be charged based on their health, gender, or age, and requiring that every plan offer a set of "essential benefits," such as preventive services and maternity care. The ACA also limited the extent to which premiums could vary by age.

Despite the ACA, the regulation of health products and premium rates is still built around individual State Insurance Departments and their respective Insurance Commissioners. The ACA allows insurers to sell policies across state lines in states that have joined "health care choice compacts." Six states—Georgia, Kentucky, Maine, Rhode Island, Washington, and Wyoming—have passed laws permitting such compacts, but no states have joined them, and no insurers have expressed interest in selling plans in such an arrangement.

Proponents of cross-state sales argue that if an insurance company sells across state lines and follows the rules of its originating state, it could offer lower prices in the adjacent state. This would provide a significant benefit to the public. However, allowing insurers to sell coverage across state lines could result in unintended consequences such as market segmentation, threatening the viability of insurers licensed in states with strict benefit coverage, issue, or rating rules. Interstate sale of health insurance is unlikely to lower costs or increase competition.

Botox Certification and Insurance: What's the Real Cost?

You may want to see also

Explore related products

![]()

Selling insurance across state lines may eliminate the ability of insurance regulators to assist consumers

Historically, US health insurance has been regulated by individual State Insurance Commissioners. Before the Affordable Care Act (ACA), there was significant variation between states in terms of insurance company regulations and how premium rates were determined to be reasonable. Mandated benefits, medical underwriting requirements, and minimum loss ratio calculations all varied from state to state. The ACA created a more uniform system of rules for health insurers, standardizing many of the differences between states. However, the regulation of health products and premium rates is still largely managed by individual states and their respective insurance commissioners.

If insurers were allowed to sell across state lines, it could result in unintended consequences such as market segmentation. Insurers licensed in states with less restrictive rules would attract younger and healthier enrollees, while states with more comprehensive benefit requirements and stricter regulations would attract older and less healthy enrollees. This could lead to increased premiums and compromised coverage access for high-risk individuals. The ability for insurance regulators to assist consumers with concerns and problems about their health insurance products may be eliminated if insurance is sold across state lines.

Proponents of cross-state insurance sales argue that insurers abiding by the rules of their originating state could lower prices in adjacent states. This theory suggests that a carrier operating in a state with lower rates could offer those price advantages to another state with higher rates. However, premium rates are based on the cost of care in the service area, and potential premium savings would be minimal as premiums reflect local healthcare costs.

While selling insurance across state lines may increase consumer choice, it is unlikely to lower costs or improve competition. In fact, premiums for insurance licensed in states with more comprehensive benefit requirements would likely increase, threatening the viability of those insurers and making it more difficult for individuals with health problems to obtain coverage. To sell policies in multiple states, insurers must comply with each state's insurance regulations, and bare-bones catastrophic plans with low premiums and high out-of-pocket costs may proliferate.

Understanding Your Health Net Medical Insurance Card

You may want to see also

Frequently asked questions

While insurers can sell insurance across state lines, it is subject to specific conditions. Before the Affordable Care Act (ACA), state insurance regulations varied, and insurers had to comply with each state's insurance regulations to sell policies in multiple states. The ACA created a more uniform system, and now insurers can sell policies across state lines in states that have joined "health care choice compacts". However, no states have joined such compacts, and no insurers have expressed interest in selling plans in this arrangement.

Proponents of cross-state sales argue that it would increase competition and drive down prices in the health insurance market. They suggest that insurers abiding by the rules of their originating state could lower prices in adjacent states with higher rates.

Critics argue that cross-state sales would not lower costs or increase competition. If widespread, it could lead to a race to the bottom, with insurance companies relocating to states with the most insurer-friendly regulatory environments. This could result in the proliferation of bare-bones catastrophic plans with low premiums and high out-of-pocket costs, making it harder for older and sicker adults to obtain adequate, affordable coverage.

The Trump Administration has made expanding choice and affordability in the health insurance market a priority. President Trump's Executive Order "Promoting Healthcare Choice and Competition Across the United States" aims to provide Americans with relief from rising premiums by increasing consumer choice and competition. The Centers for Medicare & Medicaid Services (CMS) have sought recommendations to eliminate regulatory, operational, and financial barriers to enhance issuers' ability to sell health insurance across state lines.