Health insurance companies have increasingly dropped CVS as a preferred pharmacy provider due to escalating disputes over reimbursement rates and concerns about the cost of prescription drugs. As CVS, one of the largest pharmacy chains in the United States, has expanded its services and negotiated higher fees, insurers have sought to control rising healthcare expenses by steering patients toward lower-cost alternatives. These tensions have been exacerbated by CVS's acquisition of Aetna, a major insurer, which has created conflicts of interest and further strained relationships with competing insurance providers. As a result, many insurers have removed CVS from their networks, leaving consumers to face higher out-of-pocket costs or seek alternative pharmacies to maintain coverage. This shift highlights the broader challenges in the healthcare industry, where balancing affordability and access remains a persistent issue.

| Characteristics | Values |

|---|---|

| Reason for Dropping CVS | CVS Health's acquisition of Aetna (a major health insurer) in 2018 created a conflict of interest. |

| Conflict of Interest | CVS now owned both a pharmacy benefit manager (PBM) and a health insurer, raising concerns about potential bias in drug pricing and coverage decisions. |

| Antitrust Concerns | The merger faced scrutiny from regulators and competitors who argued it would reduce competition and lead to higher healthcare costs. |

| Network Exclusions | Some health insurance companies, like Blue Cross Blue Shield in certain regions, removed CVS pharmacies from their networks, forcing members to use other pharmacies. |

| Alternative Pharmacy Networks | Insurers pushed members towards their own mail-order pharmacies or preferred retail pharmacy chains to reduce costs. |

| Negotiation Tactics | CVS's aggressive negotiation tactics with insurers over reimbursement rates may have contributed to the rift. |

| Impact on Consumers | Consumers faced inconvenience and potential higher costs if their insurer dropped CVS and they had to switch pharmacies. |

| Current Status | As of 2023, some insurers have reinstated CVS in their networks after renegotiating contracts, while others remain excluded. The situation varies by region and insurer. |

Explore related products

What You'll Learn

- Rising Prescription Drug Costs: CVS pharmacy prices led to unsustainable expenses for health insurance providers

- PBM Business Model Conflicts: CVS Caremark's PBM practices created financial risks for insurers

- Alternative Pharmacy Networks: Insurers shifted to cheaper, non-CVS pharmacy options for cost savings

- Negotiation Failures: Failed contract talks over reimbursement rates caused insurers to drop CVS

- Market Competition: Insurers prioritized partnerships with competitors like Walgreens over CVS

![]()

Rising Prescription Drug Costs: CVS pharmacy prices led to unsustainable expenses for health insurance providers

The surge in prescription drug costs has placed immense financial strain on health insurance providers, with CVS pharmacy prices emerging as a significant contributor. A 2022 analysis by the Kaiser Family Foundation revealed that CVS Health, one of the largest pharmacy benefit managers (PBMs), marked up drug prices by an average of 25% above the national average wholesale price. For insurers, this meant higher reimbursement rates for medications, even for generic drugs. For example, a 30-day supply of metformin, a common diabetes medication, cost insurers $15 through CVS, compared to $10 through independent pharmacies. Over time, these incremental increases translated into millions in additional expenses for insurers, making CVS an unsustainable partner.

Consider the case of a mid-sized health insurance company covering 500,000 members. If 10% of its members filled prescriptions for a high-cost specialty drug like Humira (adalimumab) through CVS, the insurer could face an annual bill of $50 million, given CVS’s markup. In contrast, negotiating directly with manufacturers or using alternative pharmacies could reduce this cost by up to 15%. Insurers are increasingly recognizing that CVS’s pricing model, which prioritizes profit margins over affordability, is incompatible with their goal of providing cost-effective care. This realization has prompted many to sever ties with CVS in favor of more transparent and affordable alternatives.

From a strategic standpoint, health insurance companies must weigh the short-term convenience of CVS’s extensive network against the long-term financial viability of their plans. CVS’s dominance in the pharmacy market allows it to dictate prices, often leaving insurers with little negotiating power. For instance, CVS’s acquisition of Aetna in 2018 further blurred the lines between insurer and pharmacy, creating conflicts of interest that often disadvantaged plan sponsors. Insurers dropping CVS are not just reacting to high prices but also reclaiming control over their drug formularies and negotiating leverage. By partnering with smaller PBMs or adopting value-based pricing models, they can align drug costs with patient outcomes rather than CVS’s profit targets.

Practical steps for insurers include conducting a cost-benefit analysis of CVS contracts, exploring alternative pharmacy networks, and investing in technology to track drug pricing trends. For instance, using data analytics to identify high-cost medications and negotiate better rates with manufacturers can yield significant savings. Additionally, insurers can educate members about lower-cost pharmacy options, such as mail-order services or independent pharmacies, to reduce reliance on CVS. While transitioning away from CVS may require upfront effort, the long-term savings and improved plan sustainability make it a worthwhile endeavor. As prescription drug costs continue to rise, insurers must prioritize partnerships that align with their financial and ethical responsibilities to their members.

Best Medical Insurance for National Coverage: Who's the Winner?

You may want to see also

Explore related products

![]()

PBM Business Model Conflicts: CVS Caremark's PBM practices created financial risks for insurers

CVS Caremark's pharmacy benefit manager (PBM) practices have long been a double-edged sword for health insurance companies. While PBMs are intended to negotiate lower drug prices and manage prescription benefits, CVS Caremark’s model introduced financial risks that insurers could no longer ignore. One key issue was the lack of transparency in drug pricing. CVS Caremark often retained rebates and discounts from pharmaceutical manufacturers instead of passing them directly to insurers, inflating costs and reducing plan predictability. This opacity made it difficult for insurers to budget effectively, as they were left footing the bill for higher-than-expected drug expenditures.

Consider the example of specialty medications, which account for nearly 50% of drug spending despite representing only 2% of prescriptions. CVS Caremark’s PBM model frequently steered patients toward higher-cost specialty drugs, even when lower-cost alternatives were available. For instance, a patient with rheumatoid arthritis might be prescribed a $50,000-per-year biologic drug instead of a $1,000-per-year generic DMARD (disease-modifying antirheumatic drug). Insurers were forced to cover these costs, eroding their financial stability. This practice not only increased premiums for consumers but also strained insurer-PBM relationships, as insurers felt CVS Caremark prioritized its own profits over cost containment.

To mitigate these risks, insurers began scrutinizing CVS Caremark’s formulary decisions and rebate structures. They discovered that the PBM’s incentives were misaligned with their own. For example, CVS Caremark often excluded lower-cost drugs from formularies to maximize rebates from manufacturers, leaving insurers with higher claims costs. A 2020 analysis found that insurers paid up to 25% more for certain medications when using CVS Caremark compared to alternative PBMs. This financial strain, coupled with growing regulatory pressure to lower healthcare costs, prompted insurers to seek PBM partners with more transparent and cost-effective models.

The takeaway for insurers is clear: PBM partnerships must prioritize cost transparency and alignment of incentives. Insurers should demand pass-through pricing models, where rebates are directly applied to reduce plan costs, rather than retained by the PBM. Additionally, insurers should leverage data analytics to monitor formulary decisions and ensure patients are prescribed the most cost-effective treatments. For example, a 65-year-old diabetic patient could save $1,200 annually by switching from a brand-name insulin to a biosimilar, provided the PBM includes it on the formulary. By reevaluating PBM relationships and demanding greater accountability, insurers can protect their financial health and better serve their members.

Ultimately, the conflicts in CVS Caremark’s PBM business model exposed the fragility of insurer-PBM partnerships built on misaligned incentives. Insurers’ decisions to drop CVS Caremark were not arbitrary but a strategic response to unsustainable financial risks. As the healthcare landscape evolves, insurers must remain vigilant in selecting PBM partners that prioritize cost transparency, patient outcomes, and shared financial responsibility. This shift not only safeguards insurer profitability but also paves the way for a more sustainable healthcare system.

Medications and Insurance: What Your Bill Reveals

You may want to see also

Explore related products

![]()

Alternative Pharmacy Networks: Insurers shifted to cheaper, non-CVS pharmacy options for cost savings

Health insurance companies have increasingly turned to alternative pharmacy networks as a strategic move to curb rising prescription drug costs. By shifting away from CVS, insurers aim to leverage lower-cost providers, often regional or independent pharmacies, that offer competitive pricing without compromising service quality. This transition is not merely a cost-cutting measure but a reevaluation of how pharmacy benefits are structured to maximize value for both insurers and their members.

Consider the mechanics of this shift: alternative pharmacy networks typically negotiate lower reimbursement rates with insurers, passing savings onto consumers through reduced copays or out-of-pocket expenses. For instance, a 30-day supply of a common hypertension medication like lisinopril might cost $10 at a non-CVS pharmacy compared to $20 at CVS, depending on the plan. Insurers also benefit from these networks by avoiding the higher administrative fees often associated with larger chains. This dual advantage—lower costs for patients and insurers—makes alternative networks an attractive option.

However, implementing such a shift requires careful planning. Insurers must ensure that alternative networks maintain accessibility, especially for rural or underserved populations. For example, a network might include mail-order pharmacies that deliver medications directly to patients, eliminating the need for frequent trips to a physical location. Additionally, insurers should provide clear guidance to members, such as updating formularies to highlight covered medications and offering tools like mobile apps to locate in-network pharmacies.

Critics argue that dropping CVS could limit patient choice, particularly for those accustomed to its convenience and services like immunization clinics or minute clinics. Yet, data suggests that alternative networks often include a mix of local, regional, and specialty pharmacies, preserving access to essential services. Insurers can further mitigate concerns by partnering with pharmacies that offer additional benefits, such as medication therapy management for seniors or discounted over-the-counter products for families.

In conclusion, the shift to alternative pharmacy networks represents a pragmatic solution to the escalating costs of prescription drugs. By prioritizing affordability without sacrificing accessibility, insurers can create a more sustainable healthcare ecosystem. Patients, too, stand to benefit from lower costs and a broader range of pharmacy options, provided they are well-informed and supported throughout the transition. This strategic realignment underscores the evolving dynamics of healthcare delivery, where cost-effectiveness and patient-centric care go hand in hand.

The High Cost of Medical Insurance: Why So Expensive?

You may want to see also

Explore related products

![]()

Negotiation Failures: Failed contract talks over reimbursement rates caused insurers to drop CVS

Reimbursement rates are the lifeblood of any pharmacy-insurer relationship. When negotiations over these rates break down, the consequences can be severe, as evidenced by the recent trend of health insurance companies dropping CVS from their networks. At the heart of these failures are disagreements over how much insurers should pay CVS for prescription drugs and pharmacy services. Insurers argue that CVS’s reimbursement demands are unsustainable, driving up costs for both insurers and consumers. CVS, on the other hand, contends that its rates reflect the value of its services, including patient care programs and convenient access to medications. This stalemate has led to a series of high-profile contract terminations, leaving patients scrambling for alternatives.

Consider the practical implications for a 65-year-old Medicare beneficiary who relies on CVS for monthly prescriptions, including a statin (20 mg daily) and a blood pressure medication (10 mg daily). When their insurer drops CVS, they must either switch pharmacies, potentially disrupting their medication routine, or pay out-of-pocket costs that may be prohibitively expensive. For insurers, the decision to drop CVS is not taken lightly. It involves a delicate balance between controlling costs and maintaining network adequacy. However, when negotiations fail, insurers often prioritize financial sustainability, even if it means inconveniencing their members.

A comparative analysis reveals that these negotiation failures are not unique to CVS. Similar disputes have occurred between insurers and other major pharmacy chains, such as Walgreens and Rite Aid. What sets CVS apart is its scale—with over 9,900 locations nationwide, its absence from an insurer’s network can significantly impact patient access. Insurers must weigh the benefits of lower reimbursement rates against the risk of member dissatisfaction and potential churn. For CVS, the loss of insurer contracts translates to reduced foot traffic and revenue, forcing the company to reevaluate its negotiating strategies.

To avoid such disruptions, both parties could adopt a more collaborative approach. Insurers might consider tiered reimbursement models that reward CVS for outcomes-based care, such as improved medication adherence or reduced hospital readmissions. CVS, in turn, could offer discounted rates for high-volume prescriptions or generic medications. Practical tips for patients caught in the crossfire include checking their insurer’s pharmacy network annually during open enrollment and exploring mail-order pharmacy options, which often provide 90-day supplies at lower costs. Ultimately, failed contract talks over reimbursement rates are a symptom of a broader issue: the need for a more sustainable healthcare pricing model that balances affordability with accessibility.

Why Insurance Companies Can't Transform Golfers: Unraveling the Limitations

You may want to see also

Explore related products

![VENA vCommute for iPhone 15 Pro Wallet Case, [Military Grade Drop Protection] Flip Leather Cover Slot Card Holder with Kickstand - Black Slate](https://m.media-amazon.com/images/I/8150uqOJTvL._AC_UL320_.jpg)

![Magnetic for iPhone 13 Case & iPhone 14 Case [Compatible with MagSafe][10FT Military Grade Drop Tested] Protective Shockproof Slim Translucent Matte Back Phone Case for iPhone 14/13, Green](https://m.media-amazon.com/images/I/61XL3CA1IbL._AC_UL320_.jpg)

![]()

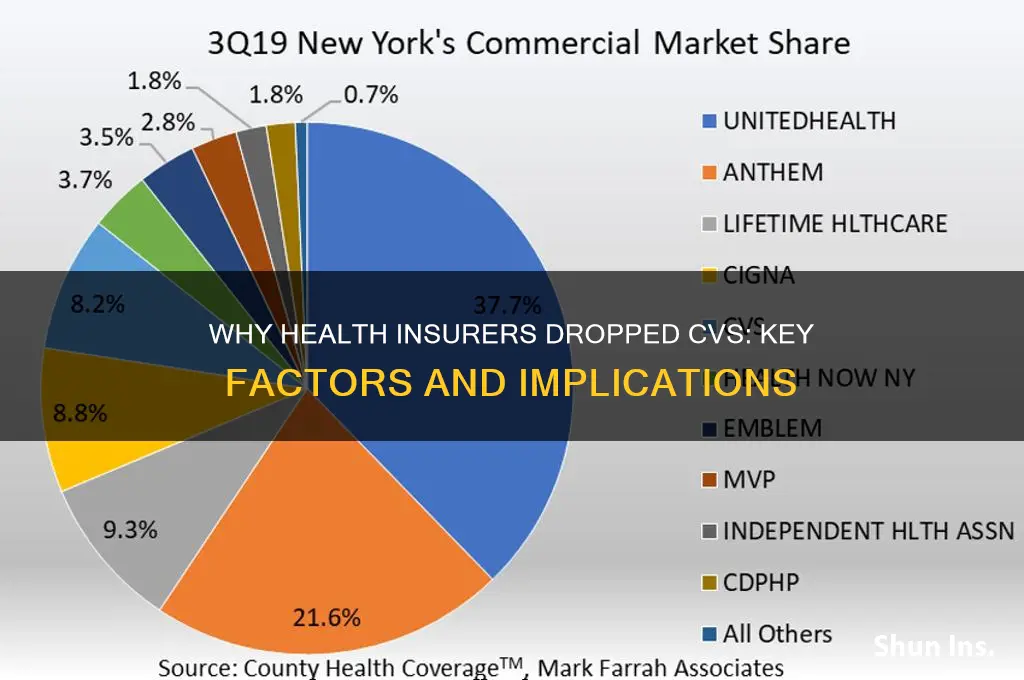

Market Competition: Insurers prioritized partnerships with competitors like Walgreens over CVS

In the fiercely competitive healthcare market, insurers often pivot alliances to maximize profitability and customer reach. One notable shift occurred when several health insurance companies opted to drop CVS in favor of partnerships with competitors like Walgreens. This strategic move wasn’t arbitrary; it was driven by a combination of market dynamics, cost considerations, and consumer behavior. Walgreens, for instance, offered insurers access to a broader network of pharmacies, including rural and underserved areas, which CVS struggled to match in certain regions. This geographic advantage allowed insurers to provide more comprehensive coverage to their policyholders, a critical factor in retaining and attracting customers.

Consider the economics of prescription drug pricing, a major pain point for insurers. Walgreens negotiated more aggressive rebates and discounts on medications, particularly for high-cost specialty drugs, which insurers could then pass on to their members. CVS, despite its Caremark pharmacy benefit manager (PBM) division, faced challenges in competing on price due to its narrower supplier agreements and higher operational costs. For example, a study found that Walgreens’ partnerships reduced insurer spending on diabetes medications by up to 15% compared to CVS, a significant savings for plans covering large populations of patients aged 45 and older, a demographic with high diabetes prevalence.

From a consumer perspective, Walgreens’ integration with insurer platforms offered a seamless experience. Their loyalty programs, like Balance Rewards, provided additional value through discounts on health and wellness products, incentivizing members to fill prescriptions at their locations. CVS’ ExtraCare program, while popular, lacked the same level of insurer integration, reducing its appeal to cost-conscious policyholders. Insurers recognized this gap and prioritized partnerships that enhanced member satisfaction and adherence to treatment plans, particularly for chronic conditions requiring consistent medication use.

However, this shift wasn’t without risks. Insurers had to balance the benefits of Walgreens’ offerings with the potential backlash from CVS’ loyal customer base. To mitigate this, many insurers adopted a phased approach, gradually transitioning members to Walgreens while offering temporary CVS access during the adjustment period. Practical tips for insurers include leveraging data analytics to identify high-risk populations and tailoring communication strategies to address concerns, such as providing personalized medication cost comparisons between the two chains.

In conclusion, the decision to prioritize Walgreens over CVS was a calculated response to market pressures, driven by cost savings, network reach, and consumer preferences. Insurers who successfully navigated this transition gained a competitive edge, demonstrating the importance of adaptability in the ever-evolving healthcare landscape. For those considering similar shifts, a data-driven, member-centric approach is key to ensuring a smooth transition and long-term success.

Understanding Medical Payments Coverage in Your Home Insurance Policy

You may want to see also

Frequently asked questions

Health insurance companies often drop CVS from their networks due to disagreements over reimbursement rates, contract terms, or strategic business decisions to reduce costs.

Yes, CVS’s merger with Aetna created conflicts of interest for some insurers, leading them to exclude CVS to avoid funneling business to a competitor.

In some cases, yes. Insurers with their own PBMs may drop CVS to steer customers toward their in-house pharmacies and services.

Yes, CVS’s pricing strategies, including high drug costs or disputes over profit-sharing, have led some insurers to remove them from their networks.

Yes, but using CVS would likely result in higher out-of-pocket costs since it would no longer be an in-network pharmacy for their insurance plan.