Health insurance companies often inquire about an individual's income to determine eligibility for certain plans, subsidies, or assistance programs, as well as to assess risk and set premiums. Income plays a significant role in calculating the affordability of coverage, especially under the Affordable Care Act (ACA), which offers premium tax credits and cost-sharing reductions based on household income. Additionally, insurers may use income data to evaluate an individual’s ability to pay for medical services, as higher income levels can correlate with increased healthcare utilization. Understanding this connection helps insurers tailor plans to meet the needs of diverse populations while ensuring compliance with regulatory requirements.

| Characteristics | Values |

|---|---|

| Income-Based Premiums | Insurance companies may use income to determine premium rates, especially in regions where income-based subsidies or surcharges apply. |

| Affordability Assessment | To assess how much an individual can afford to pay for insurance, ensuring plans are tailored to financial capability. |

| Subsidy Eligibility | In some countries (e.g., U.S. ACA), income determines eligibility for premium tax credits or cost-sharing reductions. |

| Risk Stratification | Higher income may correlate with better access to healthcare, influencing risk assessment and pricing models. |

| Compliance with Regulations | Adherence to laws requiring income verification for subsidy programs or tiered pricing structures. |

| Underwriting Practices | Historically, income was used to gauge lifestyle and health risks, though this is less common today due to regulatory changes. |

| Market Segmentation | To target specific income groups with tailored plans or marketing strategies. |

| Financial Assistance Programs | Income verification is required for Medicaid, CHIP, or other government-assisted programs. |

| Preventing Fraud | Ensures accurate reporting of income to prevent misuse of subsidies or assistance programs. |

| Policy Customization | Offers plans with deductibles, copays, or coverage levels aligned with income brackets. |

Explore related products

What You'll Learn

- Income-Based Premiums: Higher earnings often mean higher premiums due to perceived ability to pay more

- Subsidy Eligibility: Lower incomes may qualify for government subsidies, reducing insurance costs

- Risk Assessment: Income can indicate lifestyle factors that influence health risks and claims likelihood

- Payment Plans: Insurers tailor payment options based on income to ensure affordability and retention

- Market Segmentation: Income data helps insurers target specific demographics with tailored plans and pricing

![]()

Income-Based Premiums: Higher earnings often mean higher premiums due to perceived ability to pay more

Health insurance premiums are not one-size-fits-all, and income plays a significant role in determining how much you pay. The concept of income-based premiums is rooted in the idea that individuals with higher earnings have a greater ability to pay for healthcare, and thus, should contribute more. This approach is particularly prevalent in countries with private insurance markets, where insurers aim to balance risk and revenue. For instance, in the United States, some health insurance plans under the Affordable Care Act (ACA) use income as a factor to calculate premiums, especially for those purchasing coverage through the health insurance marketplace.

The Sliding Scale of Premiums

Imagine a sliding scale where your income directly influences your monthly premium. For example, a family of four earning $50,000 annually might pay $400 per month for a mid-tier plan, while a family earning $150,000 could pay $800 for the same coverage. This disparity is justified by insurers as a way to ensure affordability for lower-income households while maintaining profitability. However, it also means that higher earners often subsidize the costs for others, a practice that sparks debate about fairness and equity in healthcare financing.

The Rationale Behind the Model

From an insurer’s perspective, income-based premiums are a pragmatic solution to manage risk and revenue. Higher-income individuals are statistically less likely to default on payments and more likely to afford out-of-pocket costs, making them lower-risk policyholders. Additionally, this model aligns with the principle of progressive taxation, where those with greater financial means contribute proportionally more to the system. For instance, in Switzerland, health insurance premiums are income-adjusted, with subsidies provided to lower-income households to ensure universal access.

Practical Implications for Consumers

If you’re in a higher income bracket, understanding this model is crucial for budgeting and decision-making. For example, if your income increases significantly—say, from $75,000 to $125,000—your premiums could rise by 20-30%. To mitigate this, consider exploring employer-sponsored plans, which often have fixed premiums regardless of income, or look into health savings accounts (HSAs) to offset costs. Conversely, if you’re in a lower income bracket, ensure you’re taking full advantage of subsidies and tax credits available through government programs like the ACA.

Ethical and Economic Considerations

While income-based premiums can make healthcare more accessible for lower-income individuals, they also raise ethical questions. Critics argue that tying premiums to income can penalize high earners who may already face higher taxes and living expenses. Moreover, this model assumes that income directly correlates with ability to pay, which isn’t always the case. For example, a high-income earner with significant debt or dependents may struggle more than a moderate-income earner with fewer financial obligations. Balancing these considerations requires a nuanced approach, one that insurers and policymakers must continually refine to ensure fairness and sustainability.

Affordable Healthcare: Options for the Uninsured

You may want to see also

Explore related products

![]()

Subsidy Eligibility: Lower incomes may qualify for government subsidies, reducing insurance costs

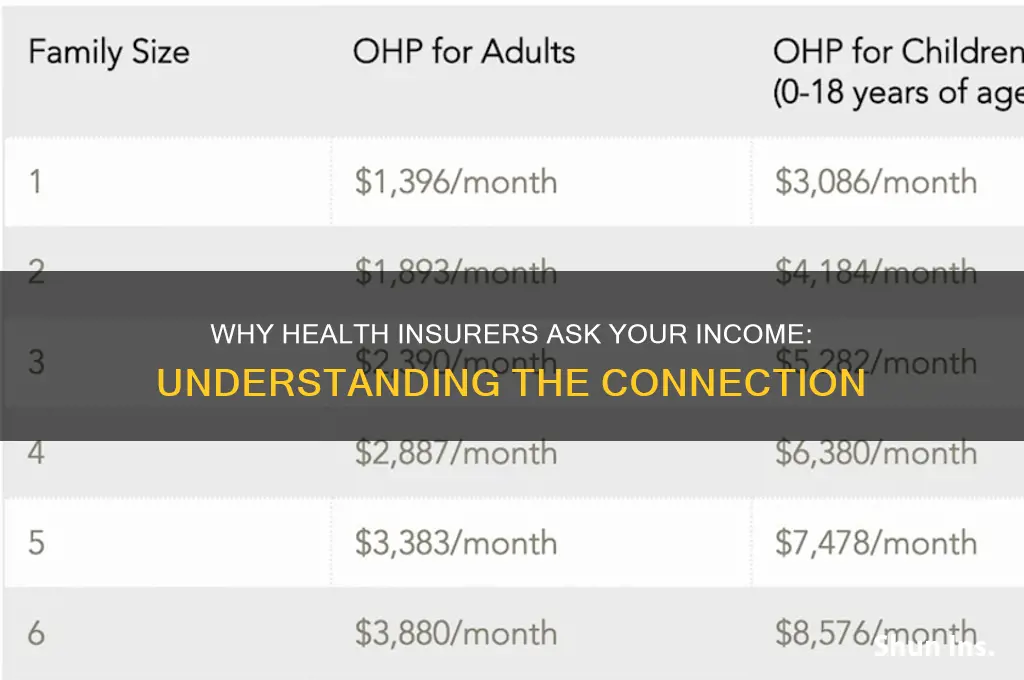

Health insurance companies often inquire about your income to determine eligibility for government subsidies, a critical factor that can significantly reduce your insurance costs. This practice is rooted in the Affordable Care Act (ACA), which established a sliding scale for premium tax credits based on household income relative to the federal poverty level (FPL). For instance, individuals earning between 100% and 400% of the FPL may qualify for subsidies that lower their monthly premiums, making health insurance more affordable. Understanding this connection between income and subsidy eligibility is essential for maximizing your healthcare savings.

To assess your subsidy eligibility, start by calculating your household income as a percentage of the FPL, which varies annually and by family size. For example, in 2023, the FPL for a single individual is $13,590, while for a family of four, it’s $27,750. If your income falls within the 100% to 400% range—$13,590 to $54,360 for an individual or $27,750 to $111,000 for a family of four—you may qualify for premium tax credits. Use the HealthCare.gov subsidy calculator to estimate your potential savings accurately. Remember, even small income fluctuations can impact your eligibility, so annual updates are crucial.

Subsidies aren’t just about lowering premiums; they also reduce out-of-pocket costs through cost-sharing reductions (CSRs) for those earning up to 250% of the FPL. CSRs lower deductibles, copayments, and coinsurance, making healthcare more accessible for lower-income individuals. For example, a Silver plan with CSRs might have a deductible of $200 instead of $4,000 for someone at 200% FPL. To qualify, you must enroll in a Silver-level plan through the Marketplace, as CSRs are only available at this metal tier. This dual benefit of premium tax credits and CSRs underscores why income reporting is a cornerstone of subsidy eligibility.

A common misconception is that subsidies are only for the unemployed or those with extremely low incomes. In reality, many middle-income families benefit from these programs. For instance, a family of three earning $40,000 annually—approximately 144% of the FPL—could save hundreds of dollars monthly on premiums. To ensure you’re not missing out, gather all necessary income documentation, including W-2s, tax returns, and pay stubs, when applying for coverage. Proactive income reporting not only secures potential subsidies but also prevents overpayment penalties if your income is later verified.

Finally, subsidy eligibility isn’t static; life changes like job loss, marriage, or the birth of a child can alter your income and qualification status. Special enrollment periods allow you to update your information and adjust subsidies mid-year if your income drops. Conversely, if your income rises, you may need to repay some subsidies at tax time. Regularly reviewing and updating your income information ensures you receive the correct subsidy amount and avoid financial surprises. By understanding and leveraging subsidy eligibility, you can transform your income disclosure from a mere formality into a powerful tool for affordable healthcare.

Cigna Medical Insurance: Illinois to Texas Coverage?

You may want to see also

Explore related products

![]()

Risk Assessment: Income can indicate lifestyle factors that influence health risks and claims likelihood

Health insurance companies often inquire about income because it serves as a proxy for lifestyle factors that significantly influence health risks and the likelihood of filing claims. Higher income typically correlates with access to better nutrition, regular exercise, and preventive healthcare, all of which reduce the risk of chronic conditions like diabetes, heart disease, and obesity. Conversely, lower income may limit access to healthy food options, safe recreational spaces, and routine medical check-ups, increasing the probability of health issues that require costly interventions. By assessing income, insurers can estimate the potential frequency and severity of claims, allowing them to set premiums that reflect the policyholder’s risk profile.

Consider the impact of income on smoking rates, a critical health risk factor. Studies show that individuals in lower income brackets are twice as likely to smoke compared to their higher-earning counterparts. Smoking not only increases the risk of lung cancer and respiratory diseases but also elevates the likelihood of cardiovascular problems, all of which drive up healthcare costs. Insurers use income data to identify populations more prone to such behaviors, factoring these risks into their underwriting models. For instance, a 40-year-old smoker earning $30,000 annually might face premiums 20-30% higher than a nonsmoker in the same age group earning $80,000, reflecting the heightened health risks associated with both smoking and lower income.

Income also influences mental health, another key determinant of claims likelihood. Financial stress, more prevalent in lower-income households, is linked to higher rates of anxiety, depression, and substance abuse. These conditions often require long-term treatment, including therapy and medication, which can be costly for insurers. For example, a policyholder earning below the poverty line is three times more likely to file claims related to mental health compared to someone in the highest income bracket. By incorporating income data, insurers can anticipate these risks and allocate resources accordingly, ensuring they remain financially viable while providing adequate coverage.

However, relying solely on income as a risk indicator has limitations. It oversimplifies the complex interplay of socioeconomic factors and individual behaviors. For instance, a high-income earner with a sedentary job and poor dietary habits may face health risks comparable to those of a lower-income individual who maintains an active lifestyle. Insurers must balance income-based assessments with other data points, such as medical history and lifestyle surveys, to create a more accurate risk profile. This nuanced approach ensures fairness while aligning premiums with actual health risks, rather than income alone.

In practical terms, policyholders can take steps to mitigate the impact of income-related risk assessments. For lower-income individuals, leveraging community health programs, employer-sponsored wellness initiatives, and government subsidies can improve access to preventive care and reduce long-term health risks. Higher-income earners should focus on maintaining healthy habits despite busy schedules, such as incorporating 30 minutes of daily exercise and prioritizing regular health screenings. Regardless of income, transparency with insurers about lifestyle choices and health improvements can lead to more accurate premium calculations, ensuring coverage reflects true risk rather than assumptions based on earnings.

Becoming a Medical Insurance Biller: Steps to Take

You may want to see also

Explore related products

![]()

Payment Plans: Insurers tailor payment options based on income to ensure affordability and retention

Health insurance companies often inquire about your income to design payment plans that align with your financial capabilities. This practice is rooted in the understanding that affordability directly impacts policy retention. By tailoring payment options based on income, insurers aim to reduce financial strain on policyholders, ensuring they remain insured without compromising their economic stability. For instance, a family earning $50,000 annually might be offered a monthly premium of $300, while a higher-income household could manage a $600 plan with additional benefits. This income-based approach not only fosters trust but also minimizes the risk of policy lapses due to non-payment.

Consider the mechanics of these payment plans. Insurers use income data to segment customers into tiers, each with distinct payment structures. For low-income individuals, options might include reduced premiums, extended payment periods, or subsidies. Middle-income earners may receive moderate discounts or flexible payment schedules. High-income policyholders, while less likely to default, are offered premium plans with added perks to justify higher costs. This stratification ensures that no demographic is priced out of coverage, balancing accessibility with profitability. For example, a single parent earning $30,000 might qualify for a $150 monthly plan with a 12-month payment extension during financial hardship.

The benefits of income-tailored payment plans extend beyond individual affordability. From a societal perspective, such models contribute to broader health insurance coverage, reducing the burden on public health systems. For insurers, retaining policyholders through flexible payment options translates to stable revenue streams and lower administrative costs associated with churn. A study by the Kaiser Family Foundation found that income-based plans increased retention rates by 25% among low-income households. This data underscores the mutual advantages of aligning payment structures with policyholders’ financial realities.

However, implementing income-based payment plans is not without challenges. Insurers must navigate the fine line between offering affordable options and maintaining profitability. Overly generous plans can strain resources, while overly restrictive ones defeat the purpose. Additionally, collecting and verifying income data requires robust systems to prevent fraud and ensure fairness. Policyholders may also feel uneasy about disclosing financial information, necessitating transparent communication about how this data is used. For instance, insurers could emphasize that income data is solely for structuring payments, not for denying coverage.

In practice, policyholders can maximize the benefits of income-tailored plans by proactively engaging with their insurers. Request a detailed breakdown of payment options and inquire about eligibility for subsidies or discounts. For example, a self-employed individual with fluctuating income might benefit from a plan that adjusts premiums quarterly based on earnings. Similarly, families anticipating income changes, such as retirement or job loss, should discuss flexible payment arrangements in advance. By understanding and leveraging these options, policyholders can secure coverage that evolves with their financial circumstances, ensuring long-term affordability and peace of mind.

Navigating Medical Insurance During Maternity Leave

You may want to see also

Explore related products

![]()

Market Segmentation: Income data helps insurers target specific demographics with tailored plans and pricing

Health insurance companies often inquire about income to refine their market segmentation strategies, a practice rooted in the need to align product offerings with consumer affordability and demand. By categorizing individuals based on income levels, insurers can design plans that resonate with specific financial capabilities. For instance, high-income earners might be targeted with premium plans offering extensive coverage and additional perks like wellness programs or reduced copays. Conversely, lower-income groups may receive options with lower monthly premiums but higher deductibles, catering to tighter budgets. This approach ensures that insurance products are not one-size-fits-all but rather tailored to meet the diverse needs of various income brackets.

Analyzing income data allows insurers to predict consumer behavior more accurately, enabling them to price plans competitively while maintaining profitability. For example, middle-income families often seek a balance between cost and coverage, prompting insurers to offer mid-tier plans with moderate premiums and reasonable out-of-pocket costs. This segmentation also helps insurers identify untapped markets, such as young professionals with disposable income who may be willing to invest in comprehensive health plans. By understanding income distribution, insurers can allocate marketing resources more effectively, targeting specific demographics with personalized campaigns that highlight the benefits most relevant to their financial situations.

A persuasive argument for this practice lies in its ability to enhance consumer satisfaction and retention. When individuals feel that their insurance plan aligns with their financial reality, they are more likely to perceive value in the product. For instance, a family earning $50,000 annually might prioritize a plan with low monthly premiums and access to a broad network of providers, while a single professional earning $150,000 might opt for a plan with lower deductibles and additional services like telemedicine. Tailoring plans to income levels fosters a sense of fairness and accessibility, encouraging long-term loyalty and reducing churn rates.

However, this strategy is not without challenges. Insurers must navigate ethical considerations, ensuring that income-based segmentation does not lead to discriminatory practices or exclude vulnerable populations. For example, low-income individuals may face limited options if insurers prioritize profitability over accessibility. To mitigate this, many companies collaborate with government programs like Medicaid or offer subsidized plans to ensure coverage for all income levels. Striking this balance requires transparency and a commitment to equitable practices, ensuring that income data is used to empower consumers rather than exploit them.

In conclusion, income data serves as a critical tool for insurers to implement effective market segmentation, enabling them to offer tailored plans that meet the financial and health needs of diverse demographics. By understanding income levels, insurers can optimize pricing, enhance consumer satisfaction, and identify growth opportunities. While ethical considerations must be addressed, the strategic use of income data ultimately benefits both insurers and policyholders, creating a more responsive and inclusive health insurance market.

Cook Insurance: Annual Salary Requirements Explored

You may want to see also

Frequently asked questions

Health insurance companies ask about your income to determine eligibility for subsidies, discounts, or government-assisted programs like Medicaid or the Affordable Care Act (ACA) marketplace plans.

Yes, your income can impact your premiums, especially if you qualify for subsidies or cost-sharing reductions under the ACA. Lower incomes may result in lower premiums.

No, health insurance companies cannot deny you coverage based on your income. However, they may offer different plans or pricing tiers depending on your financial situation.

Your income information is typically kept confidential and used solely for determining eligibility for assistance programs. It is protected under privacy laws like HIPAA.