Health insurance companies implement deductibles as a fundamental component of their policies to balance costs between the insurer and the policyholder. A deductible is the amount an individual must pay out of pocket for covered services before the insurance company begins to contribute. This mechanism serves multiple purposes: it encourages policyholders to use healthcare services judiciously, reducing unnecessary claims, and it helps insurers manage risk by limiting their financial exposure for minor or frequent medical expenses. Additionally, deductibles allow insurers to offer lower monthly premiums, making plans more affordable for consumers. By sharing the financial responsibility, deductibles ensure the sustainability of health insurance systems while incentivizing individuals to prioritize cost-effective healthcare decisions.

| Characteristics | Values |

|---|---|

| Cost Sharing | Deductibles shift some financial responsibility to policyholders, reducing insurer payouts. |

| Risk Management | They help insurers manage risk by limiting exposure to small, frequent claims. |

| Preventing Overutilization | High deductibles discourage unnecessary medical services, reducing healthcare costs. |

| Premium Control | Lower premiums are offered in exchange for higher deductibles, attracting cost-conscious consumers. |

| Encouraging Price Sensitivity | Policyholders are incentivized to compare prices for medical services. |

| Alignment with HSA/FSA | High-deductible plans often pair with Health Savings Accounts (HSAs) for tax benefits. |

| Predictable Cash Flow | Deductibles provide insurers with predictable revenue streams by limiting immediate payouts. |

| Focus on Catastrophic Coverage | Plans with deductibles often prioritize coverage for major, unexpected medical events. |

| Consumer Behavior Modification | Encourages healthier lifestyles and preventive care to avoid out-of-pocket costs. |

| Market Competition | Insurers use deductibles as a competitive tool to offer varied plan options. |

Explore related products

What You'll Learn

- Cost Sharing: Deductibles shift some healthcare costs to policyholders, reducing insurer financial burden

- Risk Management: They limit insurer liability by requiring members to pay initial expenses

- Prevent Overuse: Encourages policyholders to avoid unnecessary medical services, controlling healthcare costs

- Premium Balance: Higher deductibles often mean lower premiums, offering affordable plan options

- Consumer Responsibility: Promotes awareness of healthcare costs and encourages prudent medical decisions

![]()

Cost Sharing: Deductibles shift some healthcare costs to policyholders, reducing insurer financial burden

Deductibles serve as a cornerstone of cost-sharing in health insurance, fundamentally altering the financial dynamics between insurers and policyholders. By requiring individuals to pay a predetermined amount out-of-pocket before insurance coverage kicks in, deductibles directly shift a portion of healthcare expenses onto the consumer. This mechanism reduces the insurer’s immediate financial liability, as they are no longer responsible for covering every minor or routine medical expense. For example, a policyholder with a $1,000 deductible must pay this amount in full before the insurer begins contributing to costs. This structure incentivizes insurers to offer lower premiums, as they assume less risk for low-cost claims.

Consider the practical implications of this cost-sharing model. A policyholder with a high deductible, such as $5,000, may think twice before scheduling non-urgent medical procedures, effectively reducing the frequency of claims. This behavioral shift aligns with the insurer’s goal of minimizing payouts for avoidable or minor healthcare services. However, this approach also raises ethical questions about access to care, as individuals with limited financial resources may delay necessary treatments to avoid out-of-pocket costs. Insurers must balance cost-sharing benefits with the potential for adverse health outcomes among policyholders.

From a comparative perspective, deductibles contrast sharply with first-dollar coverage models, where insurers pay for all services from the outset. While first-dollar coverage ensures immediate access to care, it often results in higher premiums due to the insurer’s increased financial exposure. Deductibles, on the other hand, distribute risk more evenly, making insurance more affordable for both parties. For instance, a family plan with a $3,000 deductible might have monthly premiums 20-30% lower than a comparable plan with no deductible. This trade-off highlights the strategic role of deductibles in managing healthcare costs across the board.

To maximize the benefits of deductibles, policyholders should adopt proactive financial planning. Setting aside funds in a health savings account (HSA) can help cover deductible expenses without straining household budgets. For example, contributing $200 monthly to an HSA over the course of a year would accumulate $2,400—sufficient to cover a significant portion of a $3,000 deductible. Additionally, individuals should carefully review their healthcare needs and select a deductible amount that aligns with their risk tolerance and financial capacity. High deductibles may suit healthy individuals with low healthcare utilization, while lower deductibles are more appropriate for those with chronic conditions or frequent medical needs.

In conclusion, deductibles are a strategic tool for insurers to mitigate financial risk by transferring a portion of healthcare costs to policyholders. While this cost-sharing model reduces insurer burden and lowers premiums, it also demands careful consideration from consumers. By understanding the mechanics of deductibles and planning accordingly, policyholders can navigate this system effectively, ensuring financial stability without compromising access to necessary care.

Selling Major Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Risk Management: They limit insurer liability by requiring members to pay initial expenses

Health insurance deductibles serve as a critical tool in risk management, primarily by shifting a portion of the financial burden from the insurer to the policyholder. This mechanism is not arbitrary; it’s a calculated strategy to mitigate the insurer’s exposure to frequent, low-cost claims. For instance, consider a policy with a $1,000 deductible. If a member incurs $1,500 in medical expenses, they pay the first $1,000, and the insurer covers the remaining $500. This structure ensures that insurers are not liable for every minor expense, allowing them to focus resources on more significant, high-cost claims. By doing so, insurers stabilize their financial risk and maintain solvency, even in volatile healthcare markets.

To understand the practical implications, imagine a scenario where deductibles did not exist. Insurers would face a deluge of small claims—think routine check-ups, minor injuries, or prescription refills—that could quickly erode their reserves. For example, a family of four with no deductible might file 10–15 claims annually for common ailments like colds or allergies, each costing $50–$200. Over thousands of policyholders, these expenses compound exponentially. Deductibles act as a filter, discouraging members from submitting claims for trivial issues while ensuring that insurers remain financially viable to cover catastrophic events, such as surgeries or chronic disease management.

From a policyholder’s perspective, deductibles incentivize cost-conscious behavior. When individuals know they must pay out-of-pocket for the first $500 or $1,000 of care, they are more likely to weigh the necessity of services. For example, a patient might opt for a generic medication over a brand-name version or choose a telehealth consultation instead of an in-person visit for minor symptoms. This behavioral shift not only reduces insurer liability but also promotes efficiency in healthcare utilization, aligning with broader risk management goals.

However, this system is not without trade-offs. High deductibles can deter individuals from seeking necessary care, particularly in lower-income brackets. A 2020 study found that 44% of adults with deductibles over $1,000 delayed or avoided care due to cost concerns. Insurers must balance risk management with accessibility, often pairing high-deductible plans with health savings accounts (HSAs) or preventive care exemptions. For instance, many plans waive deductibles for annual physicals, vaccinations, or screenings, ensuring members prioritize preventive measures without financial barriers.

In conclusion, deductibles are a strategic risk management tool that limits insurer liability by requiring members to cover initial expenses. This approach not only safeguards insurers from the cumulative impact of small claims but also encourages policyholders to engage with healthcare costs thoughtfully. While challenges exist, particularly regarding affordability, the system’s design reflects a delicate equilibrium between financial sustainability and consumer protection. By understanding this mechanism, both insurers and members can navigate the complexities of health insurance more effectively.

Soldier Delivery Personnel: Are They Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

Prevent Overuse: Encourages policyholders to avoid unnecessary medical services, controlling healthcare costs

Health insurance deductibles serve as a financial threshold that policyholders must meet before their insurance coverage kicks in. One of the primary reasons for this design is to prevent overuse of medical services, a critical factor in controlling skyrocketing healthcare costs. When individuals face out-of-pocket expenses for every doctor’s visit or test, they are more likely to weigh the necessity of that service. For example, a policyholder with a $1,000 deductible might reconsider a $200 imaging scan for a minor ailment, opting instead for home remedies or a less expensive consultation. This behavioral shift reduces unnecessary healthcare utilization, easing the burden on both insurers and the broader healthcare system.

Consider the economic incentives at play. Without deductibles, the cost of healthcare services becomes abstract to the consumer, often leading to overconsumption. A study by the National Bureau of Economic Research found that individuals with no-deductible plans consumed 20% more healthcare services than those with high-deductible plans. This overuse not only inflates premiums but also strains healthcare resources, leading to longer wait times and reduced access for those with urgent needs. By introducing deductibles, insurers create a system where policyholders become more cost-conscious, aligning their decisions with the actual value of the services they seek.

However, caution must be exercised to ensure that deductibles do not deter necessary care. For instance, a 55-year-old with a chronic condition like diabetes might delay critical blood tests or medication refills to avoid out-of-pocket costs, potentially exacerbating their health issues. To mitigate this, insurers often exempt preventive services—such as annual check-ups, vaccinations, and screenings—from deductibles. This ensures that policyholders still prioritize essential care while discouraging frivolous use. Practical tips for policyholders include understanding their plan’s deductible structure, budgeting for potential out-of-pocket costs, and discussing cost-effective treatment options with healthcare providers.

From a comparative perspective, countries with universal healthcare systems often employ copayments or coinsurance to achieve similar goals. For instance, in Germany, patients pay a small fee for each doctor’s visit, fostering responsible healthcare consumption without the high deductibles common in the U.S. While the mechanisms differ, the underlying principle remains: introducing financial accountability reduces overuse. In the U.S., where healthcare costs are among the highest globally, deductibles play a pivotal role in balancing access and affordability.

Ultimately, deductibles are a double-edged sword. While they effectively curb overuse and control costs, they must be designed thoughtfully to avoid compromising patient health. Insurers and policymakers should continually evaluate deductible levels, ensuring they are high enough to discourage unnecessary care but low enough to remain accessible. For policyholders, the key takeaway is to view deductibles not as a barrier but as a tool for making informed healthcare decisions. By doing so, they contribute to a more sustainable healthcare system for all.

Medical Insurance in America: Understanding the Cost

You may want to see also

Explore related products

![]()

Premium Balance: Higher deductibles often mean lower premiums, offering affordable plan options

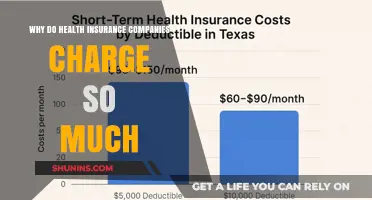

Health insurance deductibles are not arbitrary fees but strategic tools designed to balance cost and risk. A deductible is the amount you pay out of pocket before insurance coverage kicks in. Higher deductibles shift more financial responsibility to the policyholder, which might seem burdensome at first glance. However, this shift often results in lower monthly premiums, making health insurance more accessible for individuals and families on tight budgets. For example, a plan with a $1,000 deductible might have a monthly premium of $200, while a plan with a $5,000 deductible could drop the premium to $100. This trade-off allows consumers to choose a plan that aligns with their financial priorities and health needs.

Consider the case of a 30-year-old professional with no chronic conditions. Statistically, this individual is less likely to require frequent medical care beyond routine check-ups. Opting for a high-deductible plan could save them hundreds of dollars annually in premiums, which they can allocate to other financial goals, such as retirement savings or emergency funds. Conversely, a family with young children or a history of frequent medical visits might find a lower-deductible plan more cost-effective, despite higher premiums, to avoid unexpected out-of-pocket expenses. The key is to assess your health risk profile and financial flexibility before making a decision.

From a persuasive standpoint, high-deductible plans paired with Health Savings Accounts (HSAs) offer a compelling advantage. HSAs allow you to save pre-tax dollars for medical expenses, effectively reducing your taxable income while preparing for potential healthcare costs. For instance, contributing $3,000 annually to an HSA can cover a high deductible while growing tax-free over time. This dual benefit of lower premiums and tax savings makes high-deductible plans an attractive option for those who prioritize long-term financial planning.

However, this premium-deductible balance is not without caution. High-deductible plans can deter individuals from seeking necessary care due to cost concerns, potentially leading to more serious health issues down the line. A 2021 study found that 44% of Americans delayed or skipped medical care due to cost, highlighting the need for careful consideration. To mitigate this risk, ensure your plan covers preventive services at no cost, as mandated by the Affordable Care Act. Additionally, keep a small emergency fund to cover unexpected expenses until you meet your deductible.

In conclusion, the premium balance achieved through higher deductibles offers a practical solution for those seeking affordable health insurance. By understanding your health needs, financial situation, and available tools like HSAs, you can make an informed decision that maximizes value without compromising coverage. It’s not just about paying less upfront—it’s about aligning your insurance plan with your lifestyle and long-term goals.

The Dark Side of Health Insurance: Profits Over People

You may want to see also

Explore related products

![]()

Consumer Responsibility: Promotes awareness of healthcare costs and encourages prudent medical decisions

Health insurance deductibles serve as a financial threshold, requiring policyholders to pay a certain amount out of pocket before insurance coverage kicks in. This mechanism is not merely a cost-shifting strategy for insurers; it is a deliberate tool to foster consumer responsibility. By bearing a portion of healthcare expenses, individuals become more attuned to the costs associated with medical services, which in turn influences their decision-making. For instance, a patient might reconsider whether a $200 diagnostic test is truly necessary for a minor ailment, knowing they must cover the expense upfront. This heightened awareness discourages overuse of healthcare services and promotes a more thoughtful approach to medical care.

Consider the analogy of a grocery budget: when consumers pay for their own food, they are more likely to compare prices, avoid unnecessary purchases, and prioritize value. Similarly, deductibles incentivize patients to evaluate the necessity and cost-effectiveness of medical procedures. A study by the National Bureau of Economic Research found that higher deductibles reduced healthcare spending by 10–15%, largely due to decreased use of low-value services. For example, a 35-year-old with a $1,500 deductible might opt for a generic medication instead of a brand-name version, saving both themselves and the healthcare system money. This behavior not only reduces individual expenses but also alleviates the strain on collective healthcare resources.

However, fostering consumer responsibility through deductibles requires a delicate balance. While they encourage prudent decisions, excessively high deductibles can deter necessary care, particularly among low-income individuals. A Kaiser Family Foundation report revealed that 44% of insured adults with deductibles of $1,500 or more delayed or skipped care due to cost concerns. To mitigate this, insurers and policymakers must ensure that preventive services—such as annual check-ups, vaccinations, and screenings—are exempt from deductibles. This approach aligns with the principle of consumer responsibility by encouraging proactive health management while safeguarding access to essential care.

Practical strategies can further enhance the effectiveness of deductibles in promoting responsible healthcare decisions. Health savings accounts (HSAs), paired with high-deductible plans, empower individuals to save pre-tax dollars for medical expenses, fostering financial preparedness. Additionally, transparent pricing tools and cost estimators enable patients to compare prices for procedures like MRIs or blood tests, much like shopping for a car or appliance. For example, a 50-year-old planning a knee surgery could save thousands by choosing an outpatient facility over a hospital. By equipping consumers with information and resources, deductibles transform from a financial burden into a catalyst for informed, cost-conscious healthcare choices.

Ultimately, deductibles are not just a financial tool but a behavioral one, designed to align the interests of consumers with the sustainability of the healthcare system. They challenge individuals to weigh the benefits and costs of medical interventions, fostering a culture of accountability. While the system is not without flaws, its potential to reduce waste and improve efficiency is undeniable. By embracing consumer responsibility, patients become active participants in their healthcare journey, making decisions that benefit both their wallets and their well-being.

Aetna Insurance: Accepted at Hershey Medical Center?

You may want to see also

Frequently asked questions

Health insurance companies use deductibles to share the financial risk with policyholders, ensuring that individuals pay a portion of their healthcare costs before insurance coverage kicks in.

Deductibles reduce the number of small claims filed by policyholders, lowering administrative costs for insurance companies and encouraging individuals to use healthcare services more responsibly.

Yes, deductibles incentivize consumers to compare prices and seek cost-effective care, which can help control overall healthcare spending and prevent overuse of medical services.

No, deductibles vary widely depending on the type of plan (e.g., HMO, PPO) and coverage level (e.g., Bronze, Silver, Gold), with higher deductible plans typically having lower monthly premiums.