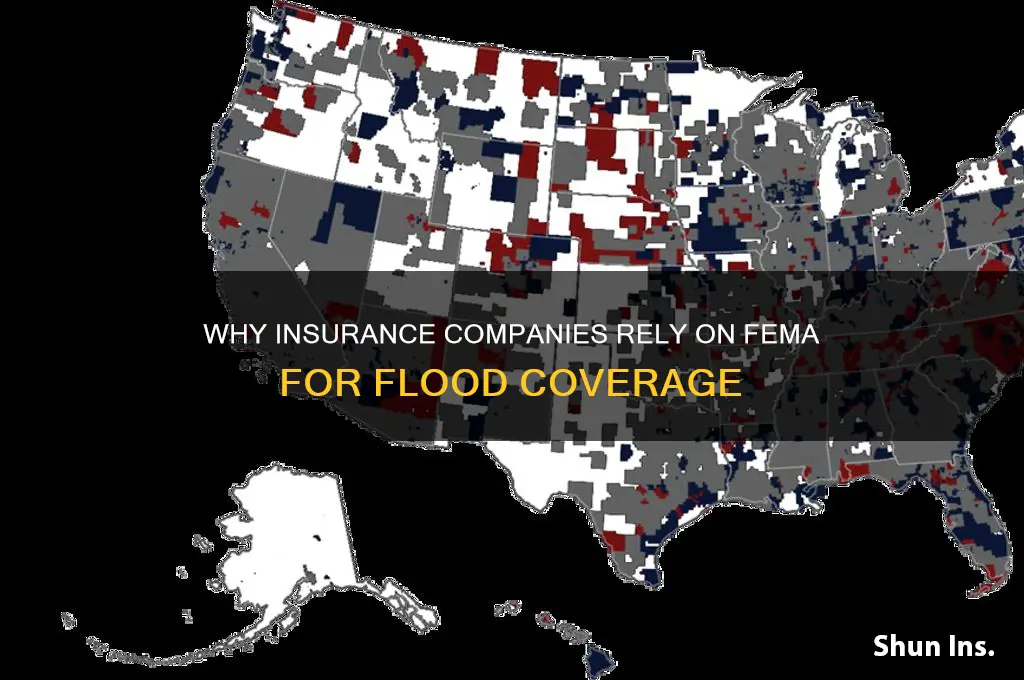

Insurance companies often rely on the Federal Emergency Management Agency (FEMA) for flood-related matters because FEMA administers the National Flood Insurance Program (NFIP), which provides flood insurance to property owners in participating communities. Since standard homeowners’ insurance policies typically exclude flood damage, the NFIP serves as a critical resource for coverage. FEMA’s role includes mapping flood zones, setting insurance rates, and managing claims, ensuring a standardized and federally backed approach to flood risk management. By partnering with FEMA, insurance companies can offer flood insurance policies to their customers while mitigating their own financial exposure to widespread flood events, which are often too costly for private insurers to handle independently. This collaboration also ensures compliance with federal regulations, such as mandatory flood insurance requirements for properties in high-risk flood zones.

| Characteristics | Values |

|---|---|

| Risk Pooling | FEMA's National Flood Insurance Program (NFIP) provides a large, nationwide risk pool, allowing insurance companies to spread flood risk across a broader geographic area, reducing their exposure to catastrophic losses in any single region. |

| Financial Backing | The NFIP is backed by the federal government, providing a financial safety net for insurance companies. This ensures that claims can be paid even in the event of widespread flooding, which might otherwise bankrupt private insurers. |

| Standardized Policies | FEMA sets standardized flood insurance policies, simplifying the underwriting process for insurance companies. This consistency reduces administrative costs and ensures policyholders receive uniform coverage. |

| Mapping and Data | FEMA maintains detailed flood maps (Flood Insurance Rate Maps, FIRMs) and risk assessment data, which insurance companies use to accurately price policies and assess risk in specific areas. |

| Claims Processing Support | FEMA provides infrastructure and guidelines for claims processing, streamlining the handling of flood-related claims and reducing the administrative burden on insurance companies. |

| Public Awareness and Education | FEMA conducts public awareness campaigns about flood risks and the importance of flood insurance, indirectly supporting insurance companies by increasing demand for their flood insurance products. |

| Regulatory Compliance | Using FEMA's NFIP helps insurance companies comply with federal and state regulations that mandate flood insurance in high-risk areas, ensuring they meet legal requirements. |

| Subsidized Premiums | FEMA offers subsidized premiums for properties in certain areas, making flood insurance more affordable for policyholders and increasing the market for insurance companies. |

| Community Rating System (CRS) | FEMA's CRS program incentivizes communities to reduce flood risk, which can lead to lower premiums for policyholders and reduced claims for insurance companies. |

| Catastrophic Coverage | FEMA provides coverage for catastrophic floods, which are often excluded from standard homeowners' policies, allowing insurance companies to offer comprehensive protection to their customers. |

Explore related products

What You'll Learn

![]()

FEMA's Role in Flood Mapping

Flood risk assessment is a critical component of insurance underwriting, and FEMA's flood maps are the cornerstone of this process. These maps, officially known as Flood Insurance Rate Maps (FIRMs), delineate areas with varying degrees of flood risk, categorized as Special Flood Hazard Areas (SFHAs) and non-SFHAs. Insurance companies rely on these designations to determine the likelihood of flood damage to a property, which directly influences policy premiums and coverage terms. For instance, properties within SFHAs typically require mandatory flood insurance for mortgage holders, while those outside these zones may opt for lower-cost policies with reduced coverage. This standardized risk assessment framework provided by FEMA ensures consistency across the insurance industry, enabling companies to price policies accurately and manage their exposure to flood-related claims effectively.

FEMA's flood mapping process involves a meticulous analysis of topographic, hydrologic, and meteorological data to model potential flood scenarios. These models account for factors such as river flow rates, storm surge probabilities, and historical flood events. For example, in coastal regions, FEMA incorporates sea-level rise projections and hurricane frequency data to assess long-term flood risks. Inland areas, on the other hand, may focus on rainfall intensity and watershed characteristics. Insurance companies leverage this detailed information to evaluate the specific risks associated with individual properties. By aligning their underwriting practices with FEMA's data-driven approach, insurers can avoid the pitfalls of underestimating flood risks, which could lead to significant financial losses during catastrophic events.

One of the most practical applications of FEMA's flood maps for insurance companies is in policyholder education and risk mitigation. Insurers often use these maps to illustrate a property's flood zone designation to clients, helping them understand their exposure and the rationale behind premium calculations. Additionally, FEMA's maps can guide recommendations for flood-resistant construction practices, such as elevating buildings or installing flood barriers. For example, a homeowner in an SFHA might be advised to raise their electrical systems above the Base Flood Elevation (BFE) to minimize potential damage. By integrating FEMA's mapping data into their customer interactions, insurance companies not only enhance transparency but also empower policyholders to take proactive steps to reduce their flood risk.

Despite their utility, FEMA's flood maps are not without limitations, and insurance companies must navigate these challenges carefully. One significant issue is the frequency of map updates, which can lag behind real-world changes in land use, climate patterns, and infrastructure development. For instance, a newly constructed dam or urban expansion might alter local flood dynamics, rendering existing maps outdated. Insurers often supplement FEMA data with proprietary risk models and real-time monitoring tools to address these gaps. Another consideration is the potential for map revisions, which can reclassify properties into higher-risk zones, triggering increased insurance costs for homeowners. Insurance companies must balance reliance on FEMA's maps with ongoing risk assessments to ensure their policies remain both accurate and fair.

In conclusion, FEMA's role in flood mapping is indispensable for insurance companies, providing a standardized, data-driven foundation for flood risk assessment. From underwriting policies to educating clients and promoting mitigation measures, these maps serve as a critical tool in the insurance industry's efforts to manage flood-related risks. However, insurers must remain vigilant about the limitations of FEMA's data, supplementing it with additional resources and analyses to stay ahead of evolving flood risks. By doing so, they can continue to offer effective coverage while fostering resilience in communities vulnerable to flooding.

Unveiling the Re-Insurers Behind Insurance Company of the West

You may want to see also

Explore related products

![]()

National Flood Insurance Program (NFIP) Partnership

Insurance companies often partner with the Federal Emergency Management Agency (FEMA) through the National Flood Insurance Program (NFIP) to manage the financial risks associated with flood events. Flooding is the most common and costly natural disaster in the United States, causing billions in damages annually. Unlike other natural disasters, flood damage is typically excluded from standard homeowners’ insurance policies, leaving a significant gap in coverage. The NFIP partnership allows private insurers to offer flood insurance policies backed by the federal government, ensuring that homeowners and businesses have access to affordable coverage while mitigating the insurers’ exposure to catastrophic losses.

Consider the mechanics of this partnership: private insurance companies act as intermediaries, selling and administering NFIP policies on FEMA’s behalf. In exchange, FEMA provides the financial backing and sets the terms, rates, and coverage limits. This arrangement benefits insurers by allowing them to expand their product offerings without assuming the full risk of flood claims, which can be unpredictable and devastating. For example, after Hurricane Harvey in 2017, NFIP paid out over $8 billion in claims, a burden that would have been insurmountable for most private insurers operating independently. By partnering with FEMA, insurers can participate in the flood insurance market while relying on the federal government’s resources to cover extreme losses.

However, this partnership is not without challenges. Critics argue that the NFIP’s reliance on outdated flood maps and subsidized rates for high-risk properties distorts the true cost of flood insurance, encouraging development in flood-prone areas. Insurers must navigate these complexities while ensuring compliance with FEMA’s regulations. To address this, some companies invest in advanced flood modeling technologies to supplement FEMA’s data, providing more accurate risk assessments for their clients. For instance, insurers like Allstate and USAA use proprietary tools to help policyholders understand their flood risk beyond the NFIP’s standard maps, fostering better-informed decisions about coverage.

For homeowners and businesses, the NFIP partnership translates to practical benefits. Policies are standardized, with coverage limits of up to $250,000 for residential structures and $100,000 for personal property. While these limits may not cover high-value properties, they provide essential protection for most homeowners. Additionally, the partnership ensures that flood insurance is widely available, even in high-risk areas where private insurers might otherwise refuse coverage. To maximize this benefit, property owners should purchase both building and contents coverage, as well as consider excess flood insurance if their assets exceed NFIP limits.

In conclusion, the NFIP partnership between insurance companies and FEMA is a strategic alliance that addresses the unique challenges of flood insurance. It enables insurers to offer critical coverage while managing risk, provides homeowners with accessible protection, and leverages federal resources to address a pervasive national issue. While the program has its limitations, ongoing innovations by insurers and potential reforms to the NFIP could further enhance its effectiveness. For those in flood-prone areas, understanding this partnership is key to securing adequate protection against one of nature’s most destructive forces.

Insurance Industry Layoffs: Economic Shifts and Automation's Impact Explained

You may want to see also

Explore related products

![]()

Risk Assessment and Data Sharing

Insurance companies rely on FEMA for flood risk assessment and data sharing because FEMA’s National Flood Insurance Program (NFIP) provides standardized, geographically precise flood maps that are legally recognized and regularly updated. These Flood Insurance Rate Maps (FIRMs) delineate Special Flood Hazard Areas (SFHAs), where properties face a 1% annual flood risk, enabling insurers to underwrite policies with consistent, federally backed data. Without FEMA’s framework, insurers would face prohibitive costs and inconsistencies in assessing flood risks across diverse regions.

Consider the process of risk assessment: FEMA’s data includes historical flood events, topography, and hydrological models, which insurers use to calculate premiums and coverage limits. For instance, a property in an SFHA may require a higher premium due to elevated risk, while one in a lower-risk zone might qualify for discounted rates. FEMA’s data sharing ensures insurers don’t rely on fragmented or outdated information, reducing the likelihood of underpricing risk or denying coverage unfairly. This standardization also streamlines compliance with federal regulations, as NFIP participation is mandatory for lenders in high-risk areas.

However, insurers must navigate limitations in FEMA’s data. For example, FIRMs may not account for localized factors like rapid urbanization or climate change-induced shifts in precipitation patterns. To mitigate this, insurers often supplement FEMA data with proprietary tools, such as satellite imagery or real-time weather analytics. This hybrid approach enhances accuracy but underscores the critical role FEMA plays as a baseline data provider. Without FEMA’s foundation, insurers would face greater uncertainty and higher operational costs in managing flood risk.

A practical takeaway for policyholders is to verify their property’s FIRM designation, as it directly impacts insurance costs and coverage eligibility. Homeowners in SFHAs are typically required to purchase flood insurance, while those in lower-risk zones may opt for it voluntarily. By understanding FEMA’s role in risk assessment and data sharing, consumers can make informed decisions about their coverage needs and advocate for updates to flood maps if local conditions have changed. This transparency fosters trust between insurers, regulators, and policyholders, ensuring a more resilient approach to flood risk management.

SC Accident Protocol: Insurance Verification by Law Enforcement

You may want to see also

Explore related products

![]()

Claims Processing Support

Insurance companies often rely on FEMA for flood-related claims due to the complexity and scale of flood damage, which can overwhelm their internal resources. FEMA’s National Flood Insurance Program (NFIP) provides a standardized framework for assessing and processing flood claims, ensuring consistency across thousands of cases. This partnership allows insurers to leverage FEMA’s expertise in flood risk management, reducing administrative burdens and improving claim accuracy. Without FEMA’s involvement, insurers would face significant challenges in handling the volume and technicalities of flood claims, particularly in catastrophic events.

One critical aspect of claims processing support is FEMA’s role in providing standardized claim forms and guidelines. Insurers use FEMA’s NFIP-approved forms, such as the Proof of Loss and Sworn Statement in Proof of Loss, to streamline documentation. These forms are designed to capture essential details about the flood damage, ensuring that claims are processed efficiently and in compliance with federal regulations. By adhering to FEMA’s standards, insurers minimize errors and disputes, which can delay payouts and frustrate policyholders. This standardization is particularly vital during large-scale flooding events when speed and accuracy are paramount.

FEMA also offers technical support to insurers through its network of adjusters and engineers specializing in flood damage assessment. These professionals are trained to evaluate structural damage, differentiate between flood-related and non-flood-related losses, and determine appropriate compensation. Insurers can tap into this expertise to resolve complex claims that require detailed analysis, such as those involving foundation damage or electrical system failures. This technical support not only improves claim accuracy but also helps insurers avoid overpayment or underpayment, which can lead to legal disputes or dissatisfied customers.

Another key benefit of FEMA’s involvement is its role in managing policyholder expectations and communications. FEMA provides resources, such as claim-tracking tools and educational materials, that insurers can share with policyholders to keep them informed throughout the claims process. This transparency reduces confusion and anxiety, particularly for homeowners dealing with the aftermath of a flood. By aligning their communication strategies with FEMA’s guidelines, insurers can enhance customer satisfaction and build trust, even in challenging circumstances.

In conclusion, FEMA’s claims processing support is indispensable for insurance companies handling flood-related claims. From standardized forms and technical expertise to communication resources, FEMA’s involvement ensures that claims are processed efficiently, accurately, and fairly. Insurers that leverage FEMA’s framework can focus on their core responsibilities while relying on a proven system to manage the complexities of flood insurance. This partnership ultimately benefits policyholders, who receive timely and appropriate compensation for their losses, and insurers, who maintain operational efficiency and customer trust.

Top Travel Insurance Companies for Stress-Free Adventures Worldwide

You may want to see also

Explore related products

![]()

Disaster Response Coordination

Insurance companies often rely on FEMA for flood-related disasters because FEMA provides a centralized framework for disaster response coordination, which is critical for efficient claims processing and resource allocation. When a flood occurs, the scale of destruction can overwhelm local and state resources, making federal intervention essential. FEMA steps in to coordinate efforts across various agencies, ensuring that rescue, relief, and recovery operations are streamlined. This coordination reduces redundancy and ensures that affected areas receive timely assistance. For insurance companies, this means having a reliable partner to assess damage, verify claims, and expedite payouts, ultimately minimizing financial and operational risks.

Consider the logistical nightmare of managing thousands of flood claims simultaneously. Without FEMA’s involvement, insurance companies would face significant challenges in verifying the extent of damage, especially in areas where local infrastructure is compromised. FEMA’s Disaster Field Offices (DFOs) serve as hubs for on-the-ground coordination, providing real-time data and assessments that insurers can use to process claims more accurately. For instance, FEMA’s flood maps and damage assessments help insurers determine whether a property is within a high-risk flood zone, which is crucial for calculating payouts and future premiums. This collaboration ensures that policyholders receive fair compensation while insurers maintain financial stability.

A key aspect of FEMA’s role in disaster response coordination is its ability to mobilize resources quickly. After a flood, FEMA deploys teams to assess damage, distribute aid, and coordinate with local authorities. Insurance companies benefit from this rapid response because it provides them with immediate access to critical information. For example, FEMA’s Individual Assistance programs often include grants for temporary housing and home repairs, which can reduce the burden on insurers by addressing immediate needs of policyholders. By working alongside FEMA, insurers can focus on long-term claims processing while FEMA handles the initial crisis management.

However, relying on FEMA is not without challenges. Coordination between federal agencies and private insurers can sometimes lead to delays or miscommunication. To mitigate this, insurance companies should establish clear lines of communication with FEMA representatives and train their staff to navigate FEMA’s processes. For instance, insurers can designate FEMA liaison officers who specialize in understanding the agency’s protocols and can expedite information exchange. Additionally, insurers should encourage policyholders to register with FEMA promptly after a flood, as this speeds up the verification process and ensures faster claim settlements.

In conclusion, FEMA’s role in disaster response coordination is indispensable for insurance companies dealing with flood claims. By leveraging FEMA’s resources, insurers can streamline their operations, reduce risks, and provide better service to policyholders. While challenges exist, proactive measures such as establishing dedicated liaisons and educating staff on FEMA procedures can enhance collaboration. Ultimately, this partnership ensures that communities recover more efficiently from floods, benefiting both insurers and the individuals they serve.

Adding a Dependent to Your Medical Mutual Insurance Plan

You may want to see also

Frequently asked questions

Insurance companies use FEMA's National Flood Insurance Program (NFIP) because flood risk is often too high and unpredictable for private insurers to manage profitably. FEMA provides a standardized, government-backed flood insurance option that private companies can offer to their customers.

FEMA’s involvement allows insurance companies to provide flood insurance without taking on the full financial risk of catastrophic flood events. The NFIP ensures claims are paid through government funds, reducing the burden on private insurers.

Yes, some private insurers offer flood insurance outside of FEMA’s NFIP, but these policies often have higher premiums or limited coverage. FEMA’s program remains the primary option for most homeowners due to its affordability and widespread availability.

Flood damage is typically excluded from standard homeowners’ policies because it is considered a high-risk, catastrophic event. Insurance companies rely on FEMA’s NFIP to provide this coverage separately, ensuring they can manage their risk effectively.