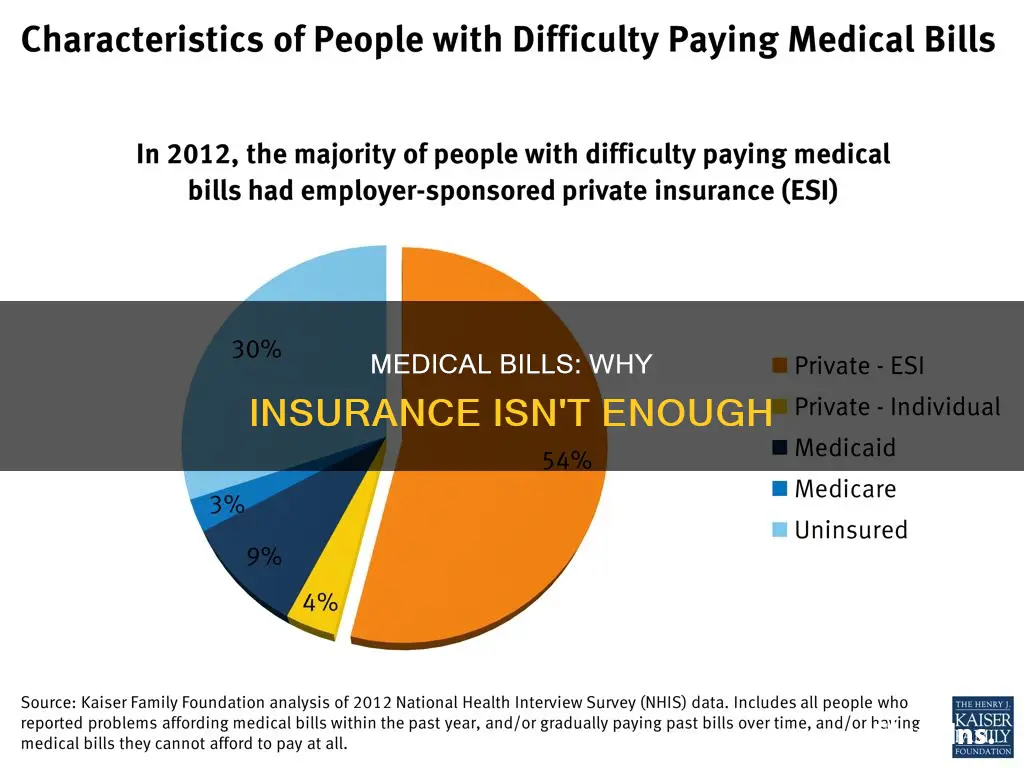

Despite over 90% of the United States population having some form of health insurance, medical debt is a persistent issue, with 55% of Americans reporting that they have medical debt. There are several reasons why people may have medical bills even with insurance. Firstly, most traditional insurance plans have high deductibles, which is the amount the policyholder must pay out-of-pocket before the insurance company covers the remaining expenses. Additionally, insurance companies often only pay a percentage of the cash price for a procedure, resulting in high copayments for the patient. Furthermore, people with complex health needs requiring ongoing care may see medical bills accumulate over time, and those with disabilities or worse health may experience unemployment or income losses, making it difficult to afford medical bills.

| Characteristics | Values |

|---|---|

| People with disabilities or in worse health | More likely to have medical debt |

| Lower-income people | More likely to have medical debt |

| Uninsured people | More likely to have medical debt |

| People with complex health needs that require ongoing care | More likely to have medical debt |

| People with unaffordable medical bills | Likely to delay or skip needed care to avoid incurring more medical debt |

| People with unaffordable medical bills | Likely to cut back on other basic household expenses |

| People with unaffordable medical bills | Likely to take money out of retirement or college savings |

| People with unaffordable medical bills | Likely to increase credit card debt |

| People with high-deductible plans | Less likely to seek out primary or preventative care due to high upfront costs |

| People without health coverage | Exposed to high medical costs |

| People without health coverage | At risk of deep debt or bankruptcy |

| People without insurance | Expected to pay the full charge |

| People without insurance | At risk of paying out-of-network charges for emergency services |

| People without insurance | At risk of paying the difference between the out-of-network billed cost and the amount paid by health insurance |

Explore related products

What You'll Learn

![]()

High deductibles

High-deductible plans are often chosen because they tend to have lower monthly premiums, which can cost hundreds of dollars. However, this means that policyholders are less likely to seek primary or preventative care due to high upfront costs. Since many medical problems are unexpected, policyholders can quickly find themselves in debt, especially when they have to pay the full, yearly deductible amount.

The rise in high-deductible plans can be attributed to employers shifting the burden of higher healthcare expenses to their employees. This has resulted in a cost shift that disproportionately affects lower-income workers and those with serious medical conditions, who are more likely to report problems paying medical bills and cut back on essential spending.

High-deductible plans can work well for people who rarely visit the doctor and anticipate very few medical expenses. On the other hand, low-deductible plans are more suitable for individuals with chronic conditions or families who expect to make several trips to the doctor annually, as it keeps their upfront costs lower and allows them to better manage their expenses.

The problem of high deductibles leading to medical debt can potentially be addressed by ensuring that all individuals are enrolled in comprehensive healthcare coverage, ending deceptive marketing of health plans, and making cost-sharing more affordable.

Medical Insurance Tax Deductibility in the UK: What's the Verdict?

You may want to see also

Explore related products

$15.97 $15.97

![]()

Unexpected costs

Additionally, insurance companies often only pay a percentage of the billed amount for a procedure, leaving the patient with unexpected out-of-pocket costs. This can be due to contracts and fee schedules that establish reimbursement amounts, or because the insurance company only covers a percentage of the cash price. In some cases, patients may be billed for out-of-network charges or surprise billing, where the insurance does not cover the full cost of the treatment.

Furthermore, even with insurance, unexpected costs can occur from medical bills due to the complexity of the medical billing system. Medical bills are often hard to understand, and it can be challenging to determine whether one owes the bill and how much they owe. There may also be errors in the billing, so it is essential to verify the accuracy of the bill before paying.

The financial implications of unexpected medical costs can be significant, with nearly half of those with medical debt reporting that it has prevented them from buying a house or saving for retirement. Many Americans, even those with insurance, do not have enough liquid assets to meet deductibles or out-of-pocket maximums, and unexpected medical bills can lead to debt or even bankruptcy.

To mitigate unexpected costs, it is recommended to assess one's health needs and compare them to the benefits offered by different insurance policies. Shopping around on the ACA marketplace may help reduce costs, especially for those with incomes above the federal poverty level, as government subsidies are available. Additionally, in cases of financial hardship, it is possible to negotiate with medical providers to reduce debts to a more manageable level.

Choosing a Medical Insurance Carrier: Name Considerations

You may want to see also

Explore related products

![]()

Lack of preventive care

Despite over 90% of the United States population having some form of health insurance, medical debt remains a persistent problem. This is partly due to the lack of preventive care, which can lead to unexpected medical expenses.

High-deductible health plans often have lower monthly premiums, making them attractive to consumers. However, these plans may deter policyholders from seeking primary or preventive care due to high upfront costs. As a result, many medical problems are left untreated and can quickly become more severe and expensive to treat. This can lead to significant medical debt, especially for those who have to pay the full deductible amount.

The high cost of healthcare in the United States can also deter people from seeking preventive care. Even with insurance, medical bills can be extremely high, and many people do not have enough liquid assets to meet deductibles or out-of-pocket maximums. For example, a surgery that is billed for $20,000 may be adjusted down to $7,000 by insurance, but the policyholder may still have to pay a few hundred to a few thousand dollars in copays. These high out-of-pocket costs can deter people from seeking medical care, even when it is necessary.

Additionally, insurance companies often only cover a percentage of the cash price for a procedure, which can result in unexpected out-of-pocket costs for the patient. This is because the initial charged amount is often much higher than what the insurance company will reimburse, and the patient is responsible for the remaining balance. This can be extremely burdensome for those with complex health needs that require ongoing care, as medical bills can quickly pile up.

The lack of preventive care can also be attributed to the structure of the insurance system itself. Many insurance plans have high deductibles, whether they are purchased through the marketplace or an employer. This means that policyholders must pay a significant amount of money out-of-pocket before their insurance coverage kicks in. As a result, many people delay or skip needed care to avoid incurring more medical debt, which can lead to a worsening of their health condition and more expensive treatments in the future.

In conclusion, the lack of preventive care is a significant contributor to medical debt, even for those with health insurance. High-deductible plans, the high cost of healthcare, and the structure of the insurance system can all deter people from seeking preventive care, leading to unexpected and expensive medical treatments down the line.

Primary Medical Insurance: A Guide for Receptionists

You may want to see also

Explore related products

![]()

Insurance markdowns

In the context of medical billing, a markdown refers to the difference between the original retail price and the lower price that a dealer charges a customer. In other words, it is the amount by which a medical bill is reduced or discounted.

Markdowns in medical billing can occur for various reasons. One common reason is when insurance companies negotiate discounted rates with healthcare providers on behalf of their insured members. These negotiated rates often result in significant markdowns from the original billed amount, sometimes as high as 70-90%. For example, a hospital may charge $1000 for a particular procedure, but the insurance company has negotiated a rate of $500. In this case, the insurance company pays $500, and the patient may be responsible for a copayment or coinsurance amount, resulting in a further markdown of the original bill.

Another reason for markdowns is when patients do not have insurance coverage or are considered out-of-network. In these cases, hospitals may offer self-pay discounts or financial hardship adjustments to reduce the patient's out-of-pocket costs. Hospitals would rather receive something than nothing, so they may be willing to negotiate lower prices to collect some payment. Additionally, federal laws such as the No Surprises Act protect patients from unexpected out-of-network medical bills and give them the right to dispute bills that exceed good faith estimates.

Markdowns can also occur due to errors or overbuying by retailers. These are referred to as permanent markdowns, as the value of the merchandise is reduced permanently, and the goal is to turn it into cash and remove it from the store as quickly as possible. Temporary markdowns, on the other hand, are used to stimulate sales and are usually taken at the point of sale for specific events or promotions.

While markdowns can provide financial relief for patients, medical debt remains a significant issue in the United States. Despite most Americans having health insurance, many do not have enough liquid assets to meet deductibles or out-of-pocket maximums. As a result, even relatively small medical bills can present significant financial challenges for many people.

Medical Mutual of Ohio: A Good Insurance Option?

You may want to see also

Explore related products

![]()

Complex billing

Medical billing is a complex process that involves multiple institutions with opposing interests, including insurance companies, healthcare providers, and patients. The billed amount for a medical service is often significantly higher than the amount reimbursed by the insurance company, which can result in high out-of-pocket costs for patients. This complexity can make it challenging for individuals to understand their medical bills and identify errors or discrepancies.

One factor contributing to complex billing is the variation in reimbursement rates among different insurance companies and plans. Insurance companies negotiate contracts and fee schedules with healthcare providers, determining the rates at which they will reimburse medical services. These negotiated rates can vary widely, resulting in inconsistent pricing for the same service across different insurance plans. As a result, patients with different insurance coverage may face varying levels of financial responsibility for the same treatment.

Additionally, insurance plans often have high deductibles, which is the amount a patient must pay out of pocket before their insurance coverage begins to pay for services. High-deductible plans tend to have lower monthly premiums, making them attractive to consumers. However, policyholders may be less likely to seek primary or preventive care due to the high upfront costs associated with meeting their deductibles. This can lead to unexpected medical debt, especially when individuals are faced with medical emergencies or unexpected health issues.

The complexity of medical billing can also be attributed to the involvement of multiple healthcare providers and facilities. When a patient receives treatment, they may receive separate bills from the hospital, physicians, laboratories, and other specialists involved in their care. Each of these bills may contain charges for specific services or procedures, making it challenging for patients to understand and reconcile their total medical expenses.

Furthermore, medical billing often includes various codes and technical terms that can be difficult for non-experts to decipher. Understanding the billing codes, procedure names, and insurance adjustments requires a level of familiarity with medical terminology and billing practices. This complexity can make it challenging for individuals to identify errors or discrepancies in their medical bills and assert their rights as consumers.

To navigate complex billing, individuals should carefully review their medical bills and ensure they understand the charges and adjustments. It is important to verify that the services and procedures listed on the bill match the care received and that there are no duplicate or erroneous charges. Individuals can also seek assistance from consumer advocacy groups, state agencies, or legal professionals to help interpret their medical bills and dispute any inaccuracies or unexpected charges.

Long-Term Medical Insurance: Your Future Health Care

You may want to see also

Frequently asked questions

Medical bills are complicated and often hard to understand. People with insurance may have medical bills due to high deductibles, out-of-pocket maximums, and unexpected out-of-network charges.

Deductibles are the amount you pay for covered health care services before your insurance plan starts to pay. For example, with a $2,000 deductible, you pay the first $2,000 of covered services yourself. High-deductible plans tend to have lower monthly premiums, which can cost hundreds of dollars, so people choose these plans to save money. However, this means that insured people may still have to pay thousands of dollars out-of-pocket before insurance coverage kicks in.

An out-of-pocket maximum is the total amount you'll have to pay no matter how much covered care you get in a plan year. For example, if your plan has a $3,000 out-of-pocket maximum, once you pay $3,000 in deductibles, coinsurance, and copayments, the plan pays for any covered care for the rest of the year. People with insurance may still have medical bills if they have not yet met their out-of-pocket maximum.

Unexpected out-of-network charges occur when you receive care at an out-of-network facility or from an out-of-network provider, and your insurance does not cover the full out-of-network cost. In these situations, insured people may be surprised by large medical bills.