Life insurance is a popular financial tool for wealthy individuals to provide for their loved ones after their death, shield their wealth from taxes, and build generational wealth. It offers a way to maximize their after-tax estate and pass on more money to their heirs. Life insurance also provides liquidity, allowing policyholders to borrow against their policy or use it as collateral for a loan. Additionally, it offers safety from market volatility and predictable rates of return, making it an attractive investment option for the wealthy.

Explore related products

What You'll Learn

![]()

Life insurance offers a tax-free way to pass on wealth to heirs

Life insurance is a popular way for wealthy individuals to pass on their wealth to their heirs. It offers a tax-free way to transfer wealth from one generation to the next, ensuring that the beneficiaries receive the maximum amount of money possible.

Life insurance death benefits are typically income-tax-free for the beneficiary. This is particularly appealing to those with a higher net worth who want to provide an inheritance that does not create an additional tax burden for their heirs. For example, if money is left in a retirement plan, like a 401(k) or Traditional Individual Retirement Account (IRA), heirs would have to pay income tax when withdrawing the money. With a life insurance policy, the death benefit is a tax-free asset, and the beneficiary can choose to receive the payout as a lump sum or in installments.

In addition, a life insurance policy is typically considered separate from an individual's estate and is not subject to inheritance tax. Inheritance tax is only present in a handful of states and forces the beneficiary to pay taxes on inherited assets. However, life insurance proceeds are generally exempt from this tax, allowing heirs to keep more of the money they inherit.

Life insurance can also provide financial protection for a family in the event of the unexpected death of a primary breadwinner. It can ensure that the family's standard of living is maintained and that their financial needs are taken care of in the future. Furthermore, many life insurance policies allow policyholders to lock in low premiums at an early age, resulting in significant savings over the life of the policy. This is especially beneficial for wealthy individuals who want to secure coverage for their children and future generations at a lower cost.

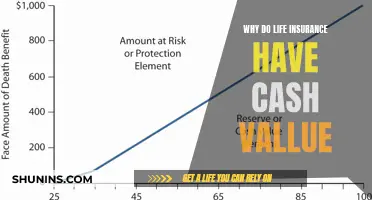

Wealthy individuals often choose permanent life insurance policies, such as whole life or universal life insurance, for wealth transfer and preservation. These policies offer the opportunity for cash value accumulation, which can provide a source of savings for future expenses. Additionally, the death benefit amount is generally guaranteed, providing financial protection for beneficiaries. Term life insurance is another option for those who want to ensure their beneficiaries receive a significant financial benefit without the need for cash value accumulation.

Overall, life insurance offers a tax-free way to pass on wealth to heirs, making it an attractive option for wealthy individuals looking to transfer and preserve their assets for future generations.

Instant Life Insurance: Get Covered Immediately

You may want to see also

Explore related products

![]()

It can be used as an investment tool with tax benefits

Life insurance can be used as an investment tool with tax benefits. Life insurance policies can be used as a financial asset during one's life, similar to an IRA or mutual fund. Permanent life insurance policies that come with cash value accounts can protect your money from stock market fluctuations. While a traditional investment account usually offers higher returns, some cash value returns, though typically lower, are more predictable.

Universal life insurance functions similarly to whole life insurance, allowing policyholders to grow an asset by accruing interest over time that can be borrowed against. With universal life policies, the premiums are not set and are subject to change, and there are no guarantees on the rate your money will earn over time. Under the universal life umbrella is "variable universal life insurance", which enables policy owners to invest their earnings into the accounts of their choosing, including mutual funds, thus increasing potential earnings over time. As you contribute to your policy over the years, you earn the ability to borrow against what you've saved, and all your earnings grow on a tax-deferred basis.

Indexed universal life insurance, or what some call LASER Funds, are also used by millionaires to keep their serious cash and continue to build wealth. LASER stands for Liquid Assets Safety Earning Returns, meaning the financial vehicle offers sufficient liquidity, safety, and predictable rates of return, with tax advantages. LASER Funds allow policyholders to borrow money income-tax-free for retirement income, business ventures, and real estate purchases. They can also be used as collateral for a loan, which can make it easier to get approved or get a better rate on the loan.

Life insurance death benefits are also income-tax-free to the beneficiary. This is appealing to individuals with a higher net worth who want to provide an inheritance that doesn't create an extra tax burden. If you leave money in a retirement plan, like a 401(k) or Traditional Individual Retirement Account (IRA), your heirs would owe income tax for taking the money out. A life insurance policy with an investment component and cash value is a good way to build more tax-free savings, and you could also sell your policy for a lump sum through a life settlement.

Life Insurance PFICs: French Predica's Status Explored

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

It can be used as collateral for a loan

Life insurance can be used as collateral for a loan, which can make it easier to get approved or secure a better rate on the loan. This is because lenders view collateral-backed loans as less risky since they can recoup their losses if the borrower defaults. This type of arrangement is called a collateral assignment, which is a lien against the proceeds of an insurance policy.

If the borrower dies before the loan is paid off, the lender gets first dibs on the death benefit to pay off the outstanding loan balance, and any remaining death benefit goes to the policy's other beneficiaries. This is a common requirement for small-business lending, as many entrepreneurs sink most, if not all, of their savings into their ventures, and a failed business might not leave enough tangible assets of value for the lender to recoup their losses.

Collateral assignment may also be a good option if you want to access funds without placing any of your assets, such as a car or house, at risk. It can also be a credible choice if your credit rating is not high, which can make it difficult to find attractive loan terms.

However, if you don't pay back the cash value taken from the policy, it can reduce the death benefit and could mean higher premiums if you were using the invested returns of the policy's cash value to offset your premium costs.

Choosing the Right Insurance: Life or Mortgage Term?

You may want to see also

Explore related products

![]()

It can help build generational wealth

Life insurance can be a useful tool for wealthy individuals to build generational wealth. Here are several ways in which life insurance can help achieve this:

Liquidity

Life insurance provides liquidity, allowing individuals to access their money whenever needed. This flexibility enables them to seize investment opportunities, such as purchasing real estate or starting a business, without liquidating their assets.

Safety

Life insurance offers a safe haven for wealth accumulation. Insurance companies have a proven track record of financial stability, even during economic downturns. This safety net ensures that principal amounts are protected, providing peace of mind, especially during volatile market conditions.

Predictable Rates of Return

Life insurance policies, particularly LASER (Liquid Assets Safety Earning Returns) Funds, offer predictable rates of return. Historically, these funds have generated returns ranging from 5% to 10%, with a guaranteed 0% floor, shielding investors from significant losses during market downturns.

Tax Advantages

Life insurance provides numerous tax advantages. Firstly, the cash value accumulated within a life insurance policy grows tax-free. Secondly, beneficiaries receive death benefits free from income tax, avoiding the tax burden often associated with inheritances. This tax-free transfer ensures that heirs receive the full intended amount, preserving generational wealth.

Estate Planning

Life insurance can help in estate planning by providing a tax-free source of funds to cover estate taxes. Without life insurance, heirs may be forced to sell off assets, such as real estate or businesses, to pay these taxes. Life insurance ensures that heirs can retain these valuable assets while also receiving the full inheritance amount.

In summary, life insurance is a valuable tool for wealthy individuals to build and protect their generational wealth. It offers liquidity, safety, predictable returns, and tax advantages, all of which contribute to the preservation and growth of wealth across generations.

Finding Life Insurance: Locating Your Provider and Coverage

You may want to see also

Explore related products

![]()

It can be used to create an investment portfolio

Life insurance can be used as an investment tool with tax benefits while the policyholder is still alive. Permanent life insurance policies that come with cash value accounts can protect the policyholder's money from stock market fluctuations. These policies are more expensive and are therefore more suitable for wealthy individuals who have covered their other financial needs and have extra money to spend on investing and creating an inheritance.

Universal life insurance functions similarly to whole life insurance, allowing policyholders to grow an asset by accruing interest over time that can be borrowed against. With universal life policies, the premiums are not set and there are no guarantees on the rate the money will earn over time. However, under the universal life umbrella is variable universal life insurance, which enables policyholders to invest their earnings into the accounts of their choosing, including mutual funds, thereby increasing their potential earnings over time.

Life insurance can be used to create an investment portfolio in several ways. Firstly, it can be used as collateral for a loan, which can increase the chances of approval or result in a better loan rate. Secondly, policyholders can simply withdraw funds from their policy, although they may have to pay taxes if their withdrawal dips into their investment gains. Thirdly, life insurance can be used as an alternative source of liquidity, helping investors avoid having to liquidate securities and potentially triggering capital gains.

Millionaires use properly structured, maximum-funded indexed universal life insurance policies, or LASER Funds, to build wealth. These funds allow them to borrow money from their policies for various purposes, such as real estate, business ventures, or education. They can pay interest to the insurance company while their money continues to earn interest. By using their LASER Funds as collateral for loans, they can avoid withdrawing their principal and giving up earning tax-free interest on their money. LASER Funds offer liquidity, safety, predictable rates of return, and tax advantages.

Life Insurance Trust: Protecting Your Family's Future

You may want to see also

Frequently asked questions

Life insurance can be used as an investment tool with tax benefits. It can also be used to provide for their loved ones in the event of their death, build cash value, or as protection against estate taxes.

Life insurance policies can accrue interest over time that can be borrowed against. This allows the wealthy to borrow from their policies whenever they need to, without having to pay income tax or an early withdrawal penalty.

Life insurance death benefits are income-tax-free for the beneficiary. This means that the wealthy can use life insurance to provide an inheritance that doesn't create an extra tax burden for their heirs.

![The Story of Life Insurance. [1907]](https://m.media-amazon.com/images/I/51kQvAmzUEL._AC_UL320_.jpg)