Homeowners insurance rates are rising across the US, with some states experiencing spikes of more than 20%. There are several reasons why insurance rates are increasing. Firstly, climate change is causing more frequent and severe weather events, leading to higher damage claims and payouts from insurance companies. Secondly, construction and labor costs have increased due to supply chain issues, rising rent and housing costs, and higher laborer demand in disaster-stricken areas. Thirdly, inflation has led to higher replacement costs for homes and belongings. Additionally, insurance companies may raise rates due to increased claims from other clients, and properties may increase in value due to additions or improvements. These factors collectively contribute to the annual increase in homeowners insurance rates.

| Characteristics | Values |

|---|---|

| Inflation | As inflation increases, insurance companies respond by raising rates |

| Natural disasters | Natural disasters linked to climate change are increasing and causing higher payouts by insurance companies |

| Inflation of building material costs | The rising cost of building materials, supply chain issues, and unfilled jobs are driving up the costs of home repairs |

| Increased value of property | Adding new rooms to your home can boost its value and insurance rates |

| Filing a claim | On average, home insurance premiums increase by roughly 7% to 10% after a claim |

| Fewer insurers | When there are fewer insurers in a particular state or region, the remaining ones may increase costs |

Explore related products

What You'll Learn

![]()

Inflation and increased construction costs

Inflation also contributes to higher construction costs, which directly impact insurance rates. The rising cost of building materials, including a 14.3% increase in material goods for new residential construction between October 2021 and October 2022, drives up the costs of home repairs and replacements. Severe weather events, such as hurricanes, wildfires, and floods, further exacerbate the situation by causing widespread damage and increasing the demand for construction materials and labor in affected areas.

The construction industry is facing challenges due to limited supplies and inflated prices for building materials, as well as a skilled labor shortage. As a result, labor rates tend to escalate in the aftermath of severe weather events, contributing to higher insurance payouts and, consequently, higher premiums for homeowners. The increasing frequency and severity of natural disasters linked to climate change play a significant role in driving up insurance costs.

Additionally, the property insurance market has become destabilized due to more frequent and severe natural catastrophes. Insurers are responding to rising damage claims caused by extreme weather events, leading to higher insurance payouts and, ultimately, increased premiums for homeowners. The impact of climate change on insurance rates is particularly evident in states like California, where wildfires in 2017 and 2018 wiped out nearly 25 years' worth of profits for insurance companies, forcing them to raise rates to balance their risk.

Unveiling the Truth Behind Farmers Insurance Ads: Creative License or Real-Life Accidents?

You may want to see also

Explore related products

![]()

Frequent and severe weather events

Climate change is causing more frequent and severe weather events, leading to an increase in homeowners' insurance rates. The rise in global temperatures has resulted in more extreme weather conditions, such as hurricanes, floods, droughts, and wildfires, which have become more destructive and costly. As a result, insurance companies have had to make higher payouts, leading them to raise their prices to remain solvent. This dynamic is evident in Houston, where the risk assessors at First Street Foundation estimate that what used to be a 100-year disaster is now expected once every 23 years.

The impact of climate change on insurance rates is particularly notable in disaster-prone states like California, Florida, North Carolina, Oklahoma, and Texas. For example, California's wildfires in 2017 and 2018 wiped out nearly 25 years' worth of profits for insurance companies in the state. As a result, these companies have had to increase their rates to balance their risk and cover their costs.

The increase in weather-related claims has also contributed to the rise in homeowners' insurance rates. When a severe weather event occurs, many homes in the area can be impacted, leading to a spike in the demand for construction materials and labor, driving up the costs of home repairs. This dynamic is reflected in the data, which shows that the average number of billion-dollar disasters has increased from 3.3 per year in the 1980s to 18.3 per year in the decade leading up to 2024.

Insurers typically adjust rates based on actual and anticipated weather-related losses. As a result, homeowners in states with a higher risk of severe weather events may face higher insurance premiums. Additionally, as construction costs rise, the cost to repair or rebuild a home in the event of weather-related damage also increases, further driving up insurance rates.

The combination of more frequent and severe weather events, higher payouts from insurance companies, and increased costs for construction and labor has led to the steady increase in homeowners' insurance rates observed in recent years.

Farmers Insurance Umbrella: Comprehensive Protection for Your Assets

You may want to see also

Explore related products

![]()

Filing a claim

It is worth noting that the frequency and severity of natural disasters, such as hurricanes, wildfires, and floods, have increased due to climate change. These events have resulted in higher damage claims and payouts for insurance companies, leading them to raise their prices to remain solvent. As a result, homeowners face rising insurance costs. Additionally, the cost of repairing or rebuilding a home after a disaster has increased due to higher labour and construction expenses, further contributing to the overall rise in insurance rates.

To mitigate the impact of filing a claim on your homeowner's insurance rates, consider the following:

- Contact your insurance agent or specialist: Before filing a claim, discuss the specifics of your situation with your agent or an insurance specialist. They can help you assess whether filing a claim is the best course of action and provide guidance on alternative options.

- Compare rates and shop around: Re-evaluate your home insurance annually to ensure you are getting the best coverage and rates. Compare prices and policies from multiple insurance companies to find the most suitable option for your needs.

- Choose a high-deductible policy: If your home is not prone to many hazards and you have a good history with your insurer, consider opting for a high-deductible policy. A higher deductible can lower your premium, but ensure you have sufficient savings to cover the deductible in case of a loss.

- Explore customer retention programs: Some insurance companies offer loyalty programs that provide premium discounts or credits to long-term customers. These programs can help offset any increases in your insurance rates due to filed claims.

- Bundle your policies: You may be able to save money by bundling your homeowner's insurance with other policies, such as car, boat, or speciality coverages. Insurance providers often offer discounts when you purchase multiple policies with them.

Trampoline Hazards: Insurers Need to Know

You may want to see also

Explore related products

![]()

Property value increases

One of the main reasons why homeowners' insurance increases every year is due to property value increases. The value of a property is determined by its location, square footage, and any additions or improvements made. If a homeowner adds a new room, deck, or makes significant investments in home improvement, such as updating the kitchen, the property's value increases. This, in turn, leads to higher insurance premiums.

Inflation also plays a role in property value increases. As inflation rises, so do the costs of construction materials and labour. This is especially true after severe weather events, such as hurricanes, wildfires, or tornadoes, which can cause spikes in construction costs due to increased demand and limited supply. As a result, insurance companies raise rates to keep up with the increased cost of rebuilding homes.

Additionally, the age and condition of a home can impact its value. Older homes may require updates to meet modern building codes, and homes with older roofs may be subject to higher premiums as the roof is crucial in keeping the house intact.

It is important to note that the replacement cost of a home, which includes the cost of rebuilding it from the ground up, differs from the market value, which includes the land's value. Home insurance rates are most directly affected by the replacement cost, as it is often the largest coverage limit on the policy.

Furthermore, the location of a property can influence its value and, consequently, the insurance rates. Properties in high-risk areas, such as those prone to natural disasters or with higher crime rates, may face higher insurance premiums.

Overall, property value increases are a significant factor in the annual rise of homeowners' insurance premiums, and it is essential for homeowners to keep their property details updated with their insurance company to ensure adequate coverage.

Escrow Advantage: Taxes, Insurance, and Mortgage

You may want to see also

Explore related products

![]()

Lack of insurers in certain states

Homeowners' insurance rates are increasing across the United States, with significant variation by region and ZIP codes. One of the contributing factors to this trend is the lack of insurers in certain states, which leads to higher premiums for homeowners.

In states like California, Louisiana, and Florida, private insurers have faced challenges such as unprofitability, insolvencies, and market exits. For example, in California, insurers have incurred substantial underwriting losses on their homeowner policies due to wildfires, which have resulted in increased costs for rebuilding and repairing homes. As a result, some insurers have stopped writing new policies or capped the number of new policies, reducing the options available to homeowners.

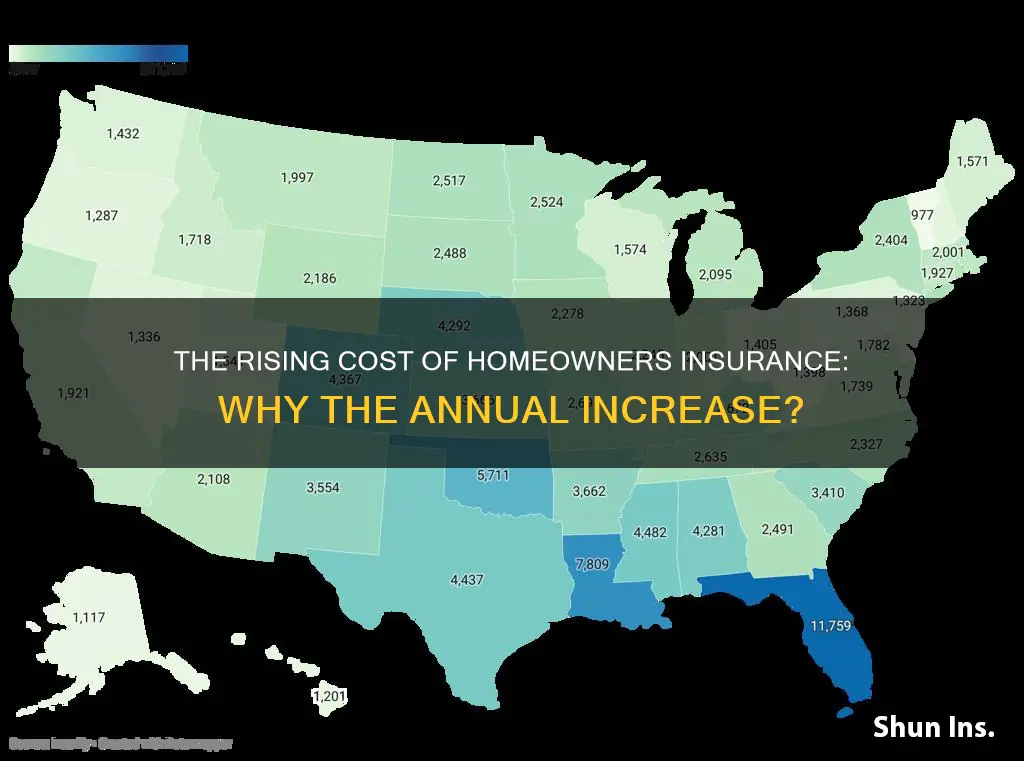

A similar situation is observed in Florida, where the high risk of catastrophes, including hurricanes and floods, has made it challenging for insurers to operate. The average premium on a Florida homeowners' policy is around $6,000 per year, almost four times the US average of $1,700. The high cost of insurance in Florida is further exacerbated by the need for additional flood insurance, which is typically required for those with a Citizens' policy.

The lack of insurers in these states is not just a result of market conditions but is also influenced by regulatory requirements. For instance, in California, Proposition 103 includes provisions that can delay premium rate adjustments and require a minimum of 20 years of past claims history for premium loadings, regardless of recent growth in wildfire losses. These factors contribute to the financial challenges faced by insurers in the state.

The trend of decreasing insurer options is concerning as it leads to higher premiums for homeowners. With fewer insurers in a particular state or region, the remaining insurers can implement stricter underwriting criteria and increase costs to reflect higher demand and exposure. This dynamic further exacerbates the financial burden on homeowners, especially in high-risk states.

Addressing the lack of insurers in certain states requires a comprehensive approach that considers market conditions, regulatory requirements, and the impact of climate change. By working together, policymakers, insurers, and consumers can develop solutions that improve the availability and affordability of homeowners' insurance, even in areas with higher catastrophe risks.

Reporting Insurance Fraud in Indiana: What You Need to Know

You may want to see also

Frequently asked questions

There are several reasons why homeowners insurance rates may increase annually. Firstly, insurance companies adjust their rates in response to inflation, as the cost of replacing your home and belongings will increase with inflation. Secondly, severe weather events and natural disasters have become more frequent and destructive due to climate change, leading to higher damage claims and payouts by insurance companies, who then raise their prices to cover these costs. Finally, the cost of building materials and labour has been increasing, which also contributes to higher insurance rates.

As inflation increases, the cost of replacing or repairing your home and belongings also increases. Insurance companies reference the Consumer Price Index to measure inflation and adjust their rates accordingly. This means that even if nothing has changed with your property, you may still experience higher insurance rates due to inflation.

Climate change has led to more frequent and severe weather events, such as hurricanes, wildfires, storms, and flooding. These events cause widespread damage, resulting in increased insurance claims and payouts. Insurance companies factor in the risk associated with climate change and adjust their rates to remain financially stable. As a result, homeowners may experience higher insurance rates or reduced coverage to mitigate the increased risk.