Insurance companies often raise premiums due to a combination of factors, including increased claims payouts, rising healthcare or repair costs, and higher operational expenses. Additionally, changes in regulatory requirements, inflation, and unpredictable events like natural disasters can drive up the overall risk for insurers, prompting them to adjust rates to maintain profitability and ensure sufficient funds to cover future claims. Policyholders may also see increases if their individual risk profile changes, such as a history of accidents or filing multiple claims. These adjustments are typically based on actuarial data and industry trends, aiming to balance the insurer’s financial stability with the need to provide adequate coverage to customers.

| Characteristics | Values |

|---|---|

| Increased Claims Costs | Rising medical, repair, or liability costs lead to higher payouts, prompting rate hikes. |

| Inflation | General inflation increases operational costs for insurers, reflected in premiums. |

| Natural Disasters | Frequent catastrophic events (e.g., hurricanes, wildfires) drive up claims expenses. |

| Regulatory Changes | New laws or mandates (e.g., minimum coverage requirements) increase insurer costs. |

| Policyholder Risk Profile | Changes in driving record, health status, or location can elevate risk and premiums. |

| Economic Conditions | Economic downturns may lead to more claims (e.g., theft, unemployment-related incidents). |

| Investment Performance | Poor returns on insurer investments can offset losses, leading to higher premiums. |

| Fraudulent Claims | Increased fraud drives up costs, impacting overall premium rates. |

| Technological Advancements | Adoption of new technologies (e.g., telematics) may initially raise costs for insurers. |

| Market Competition | Reduced competition or market consolidation can allow insurers to raise rates. |

| Policy Add-ons or Upgrades | Adding coverage options or increasing policy limits directly raises premiums. |

| Reinsurance Costs | Higher reinsurance premiums (insurers' insurance) are passed on to policyholders. |

| Demographic Shifts | Aging populations or urban migration can increase risk pools and premiums. |

| Legal Settlements | Large legal payouts in lawsuits against insurers can impact overall rates. |

| Underwriting Practices | Stricter risk assessment or policy exclusions may result in higher premiums for some. |

Explore related products

What You'll Learn

- Inflation Impact: Rising costs of claims and services force insurers to increase premiums to maintain profitability

- Increased Risk: Higher claim frequencies or severity due to accidents, disasters, or health issues drive up payments

- Regulatory Changes: New laws or compliance requirements can add operational costs, leading to premium hikes

- Economic Factors: Poor investment returns or market volatility may prompt insurers to raise rates

- Policyholder Behavior: Changes in customer demographics, coverage needs, or claims history influence payment adjustments

![]()

Inflation Impact: Rising costs of claims and services force insurers to increase premiums to maintain profitability

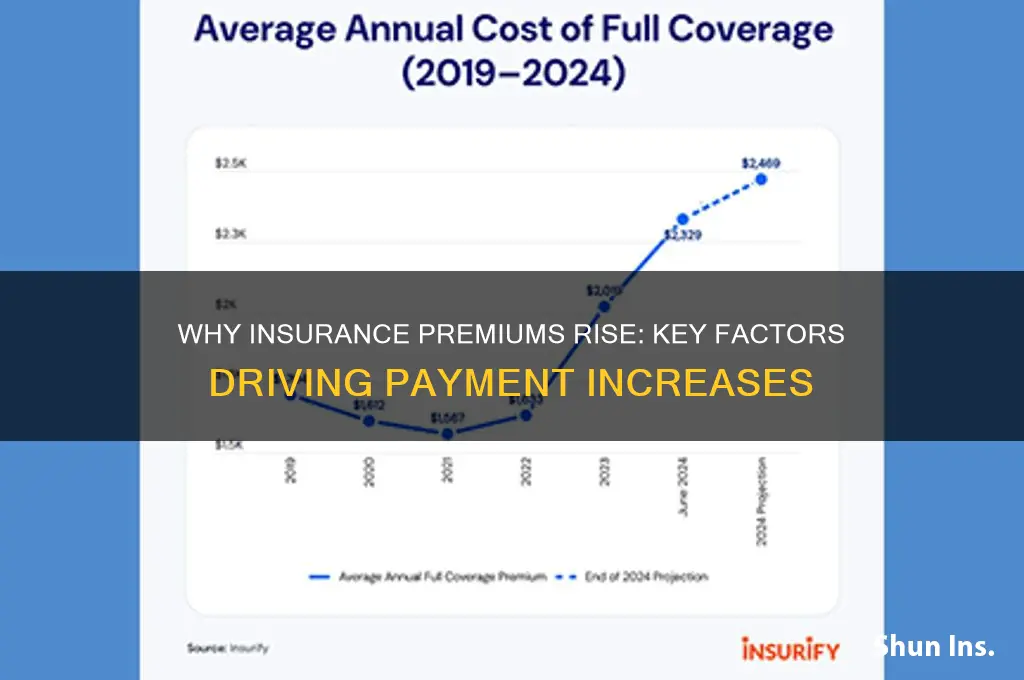

Insurance companies are not immune to the economic forces that shape the broader market. One of the most significant factors influencing premium increases is inflation, which drives up the cost of claims and services. When the price of medical care, auto repairs, and construction materials rises, insurers must pay more to settle claims. To maintain profitability and ensure they can meet their financial obligations, insurers often have no choice but to pass these increased costs on to policyholders in the form of higher premiums.

Consider the healthcare sector, where inflation has been particularly pronounced. Between 2010 and 2020, U.S. healthcare costs increased by an average of 4.9% annually, outpacing general inflation. For health insurers, this means higher payouts for medical treatments, hospital stays, and prescription drugs. To offset these expenses, premiums for individual and group health plans have risen steadily. For example, the average annual premium for employer-sponsored family coverage reached $22,221 in 2022, with employees contributing $6,106 of that amount. This trend underscores the direct link between inflationary pressures in healthcare and the rising cost of insurance.

The impact of inflation is equally evident in the auto insurance industry. The cost of vehicle repairs has surged due to higher prices for parts and labor. For instance, the price of auto body work increased by 5.5% in 2021 alone, driven by supply chain disruptions and rising material costs. Additionally, the growing prevalence of advanced driver-assistance systems (ADAS) in modern vehicles has made repairs more expensive. Insurers must account for these higher claims costs, leading to premium increases. A 2022 study found that auto insurance rates rose by an average of 4.9% nationally, with some states experiencing double-digit hikes.

To mitigate the effects of inflation, policyholders can take proactive steps. For health insurance, consider high-deductible plans paired with health savings accounts (HSAs), which offer tax advantages and encourage cost-conscious healthcare decisions. In auto insurance, raising deductibles or bundling policies can reduce premiums. Additionally, maintaining a good credit score and safe driving record can qualify individuals for discounts. While these strategies may not eliminate premium increases entirely, they can help manage costs in an inflationary environment.

Ultimately, the relationship between inflation and insurance premiums is a delicate balance. Insurers must navigate rising claims costs while remaining competitive in the market. For consumers, understanding this dynamic is crucial for making informed decisions about coverage. By staying informed and exploring cost-saving options, policyholders can better adapt to the financial pressures created by inflation.

Discovering the Top Insurance Company: A Comprehensive Industry Leader Analysis

You may want to see also

Explore related products

![]()

Increased Risk: Higher claim frequencies or severity due to accidents, disasters, or health issues drive up payments

Insurance companies are not arbitrary in their decision to raise premiums; they are, in fact, responding to a delicate balance between risk and reward. At the heart of this issue lies the concept of increased risk, a multifaceted beast that rears its head in various forms: accidents, natural disasters, and escalating health issues. Each of these factors contributes to a surge in claim frequencies and severity, leaving insurers with no choice but to recalibrate their payment structures.

Consider the aftermath of a catastrophic hurricane, where entire neighborhoods are reduced to rubble. The sheer volume of claims filed in the wake of such an event can be staggering, with policyholders seeking compensation for damaged property, lost possessions, and temporary living expenses. As insurers shell out millions, even billions, of dollars to cover these claims, they are forced to reassess their risk models and adjust premiums accordingly. For instance, residents in coastal areas prone to hurricanes may see their premiums increase by 10-20% or more, reflecting the heightened risk of future storms. Similarly, drivers in regions with high accident rates, such as densely populated urban centers, may face premium hikes of 5-15%, as insurers factor in the increased likelihood of collisions and subsequent claims.

To mitigate the impact of increased risk, insurers often employ sophisticated data analytics and modeling techniques. By analyzing historical claim data, demographic trends, and environmental factors, they can identify patterns and predict future risks with greater accuracy. For example, health insurers may use predictive modeling to identify high-risk populations, such as individuals over 50 with pre-existing conditions like diabetes or heart disease. These policyholders may be subject to higher premiums, as they are statistically more likely to file claims for costly medical treatments, such as insulin therapy (which can cost $100-$500 per month) or cardiac procedures (which can exceed $50,000). By targeting these high-risk groups, insurers can adjust their premiums to reflect the anticipated claim costs, ensuring they remain financially viable.

A comparative analysis of different insurance sectors reveals distinct strategies for managing increased risk. While auto insurers may focus on driver behavior and vehicle safety features, health insurers prioritize preventive care and wellness programs. For instance, some health insurers offer discounted premiums to policyholders who participate in regular exercise programs or undergo annual health screenings. By encouraging healthy behaviors, these insurers aim to reduce the frequency and severity of claims, ultimately lowering costs for both themselves and their policyholders. In contrast, property insurers may invest in community-based initiatives, such as flood mitigation projects or wildfire prevention programs, to reduce the risk of catastrophic events and minimize claim payouts.

As a practical guide for policyholders, it is essential to understand the factors that contribute to increased risk and take proactive steps to mitigate them. For example, drivers can reduce their risk of accidents by practicing safe driving habits, such as avoiding distractions and maintaining a safe following distance. Homeowners in disaster-prone areas can invest in resilient construction materials, such as impact-resistant windows or reinforced roofing, to minimize damage from storms or wildfires. By taking these precautions, policyholders can not only reduce their risk of filing claims but also potentially qualify for lower premiums or discounts from their insurers. Ultimately, by working together to manage increased risk, insurers and policyholders can create a more stable and sustainable insurance ecosystem, one that balances risk and reward in a fair and equitable manner.

Canceling Medical Insurance: When and How to Do It

You may want to see also

Explore related products

![]()

Regulatory Changes: New laws or compliance requirements can add operational costs, leading to premium hikes

Insurance companies often face the challenge of balancing profitability with regulatory compliance, and this delicate equilibrium can directly impact policyholders' premiums. When new laws or regulations are introduced, insurers must adapt their operations, and these adjustments frequently come with a price tag. For instance, consider the implementation of stricter data privacy regulations, such as the General Data Protection Regulation (GDPR) in Europe or the California Consumer Privacy Act (CCPA) in the United States. These laws mandate enhanced data security measures, consumer rights, and transparency in data handling practices. To comply, insurance companies invest in advanced cybersecurity systems, hire specialized personnel, and update their data management processes, all of which contribute to increased operational expenses.

The financial burden of regulatory compliance is not limited to technology and personnel. Insurance providers must also allocate resources for legal consultations, staff training, and ongoing monitoring to ensure adherence to new rules. For example, the Affordable Care Act (ACA) in the U.S. introduced numerous provisions, including essential health benefits and pre-existing condition coverage, which required insurers to redesign their health insurance plans. This process involved complex legal and actuarial work, resulting in significant costs that were partially offset by adjusting premiums. As a result, policyholders experienced rate increases, not solely due to rising healthcare costs but also as a direct consequence of regulatory changes.

A comparative analysis of the insurance market before and after the introduction of new regulations often reveals a clear pattern of premium hikes. Take the case of the European Union's Solvency II directive, which aimed to strengthen the capital adequacy and risk management of insurance companies. While this regulation enhanced the industry's stability, it also led to a substantial rise in compliance costs. Insurers had to invest in sophisticated risk modeling tools, employ additional risk management experts, and maintain higher levels of capital reserves. These measures, essential for compliance, ultimately contributed to higher premiums across various insurance products, from life and health to property and casualty.

To navigate the impact of regulatory changes, insurance companies employ various strategies. One approach is to streamline operations and improve efficiency to absorb some of the additional costs without passing them entirely to customers. However, when the financial burden is substantial, premium adjustments become inevitable. Policyholders can take proactive steps to mitigate the effects of these increases. Regularly reviewing and comparing insurance policies can help identify more cost-effective options. Additionally, understanding the specific regulatory changes affecting the insurance industry can provide insights into the timing and reasons for premium hikes, enabling consumers to make informed decisions and plan their finances accordingly.

In summary, regulatory changes are a significant driver of insurance premium increases, as they impose new operational requirements and costs on insurers. From data privacy laws to industry-specific regulations, these changes demand substantial investments in technology, personnel, and compliance processes. While insurance companies strive to manage these expenses, the financial impact often translates into higher premiums. By recognizing the connection between regulatory compliance and insurance costs, consumers can better understand the factors influencing their payments and make more informed choices in a dynamic insurance market.

Medical Insurers: Doctor Visits Covered in the USA?

You may want to see also

Explore related products

![]()

Economic Factors: Poor investment returns or market volatility may prompt insurers to raise rates

Insurance companies often rely on investment income to supplement premiums and maintain profitability. When financial markets underperform, these returns shrink, creating a shortfall that must be addressed. For instance, during the 2008 financial crisis, many insurers saw their investment portfolios plummet, forcing them to raise premiums to offset losses. This dynamic illustrates how external economic conditions directly impact policyholder costs.

Consider the mechanics: Insurers invest premiums in bonds, stocks, and real estate to generate returns. When interest rates fall or stock markets decline, these investments yield less. A 1% drop in investment returns on a $10 billion portfolio translates to a $100 million revenue loss. To compensate, insurers may increase premiums by 5-10% for policyholders, depending on the severity of the shortfall. This calculation highlights the delicate balance between investment strategy and premium pricing.

Market volatility compounds the challenge. Unpredictable economic conditions make it difficult for insurers to forecast returns accurately. For example, during periods of high inflation, bond values may decline, while equity markets become more volatile. This uncertainty forces insurers to adopt a conservative approach, often raising premiums preemptively to build reserves. Policyholders in volatile regions or industries may see steeper increases due to heightened risk exposure.

To mitigate these effects, insurers employ hedging strategies, such as diversifying investments or purchasing reinsurance. However, these measures have limits. When systemic economic issues persist, rate increases become inevitable. For policyholders, understanding this linkage is crucial. Reviewing annual reports or financial disclosures can provide insights into an insurer’s investment health and potential future rate adjustments.

Ultimately, economic factors like poor investment returns and market volatility are beyond individual control, but their impact on insurance premiums is tangible. Policyholders can proactively shop around, compare rates, and negotiate terms, especially during renewal periods. Staying informed about macroeconomic trends can also help anticipate changes, allowing for better financial planning in the face of rising insurance costs.

Florida Homeowners Insurance: Which Companies Cover Pet Liability?

You may want to see also

Explore related products

![]()

Policyholder Behavior: Changes in customer demographics, coverage needs, or claims history influence payment adjustments

Insurance premiums aren't set in stone. They're dynamic, responding to a complex dance of factors, and one of the most significant partners in this dance is you, the policyholder. Your behavior, from the day you sign on the dotted line to your claims history years down the line, directly impacts the cost of your coverage.

Think of it like a fitness tracker monitoring your health. Just as your activity level and diet influence your health metrics, your driving habits, lifestyle choices, and claims history paint a picture of your risk profile for insurers. This profile, in turn, determines the likelihood of you filing a claim and the potential cost of that claim.

Let's break it down. Imagine a young driver, fresh out of high school, purchasing their first car insurance policy. Their age, lack of driving experience, and statistically higher risk of accidents place them in a higher-risk category. This translates to higher premiums. However, as they gain experience, maintain a clean driving record, and perhaps even take defensive driving courses, their risk profile improves, potentially leading to lower premiums over time.

Conversely, a policyholder who files multiple claims within a short period, regardless of fault, signals a higher risk to the insurer. This could be due to frequent accidents, living in an area prone to natural disasters, or even a history of filing frivolous claims. As a result, the insurer may adjust premiums upwards to account for the increased likelihood of future payouts.

It's not just about accidents and claims. Changes in your lifestyle can also trigger premium adjustments. For instance, if you start using your vehicle for business purposes, your risk exposure increases, potentially leading to higher premiums. Similarly, moving to a neighborhood with higher crime rates or a region prone to severe weather events can also impact your rates.

Even seemingly minor changes can have an effect. Adding a teenage driver to your policy, for example, will likely result in a premium increase due to the higher risk associated with young, inexperienced drivers.

Understanding these dynamics empowers you to make informed decisions. Maintaining a clean driving record, bundling policies, and choosing a higher deductible can all help mitigate premium increases. Additionally, regularly reviewing your policy and shopping around for competitive rates ensures you're getting the best value for your coverage. Remember, you're not just a passive recipient of insurance rates; you're an active participant in the process. By being mindful of your behavior and its impact on your risk profile, you can take control of your insurance costs and ensure you're adequately protected without breaking the bank.

Top Companies Offering Exceptional Employee Health Insurance Plans in 2023

You may want to see also

Frequently asked questions

Insurance companies raise premiums to account for increased claims costs, rising healthcare or repair expenses, inflation, and higher operational costs.

Yes, filing a claim can lead to higher premiums, especially if the claim is large or if you have multiple claims in a short period, as it signals higher risk to the insurer.

Rates can increase due to broader factors like rising industry claims trends, natural disasters, regulatory changes, or increased costs in the area where you live.

Yes, in many regions, insurance companies use credit-based insurance scores to assess risk. A lower credit score may result in higher premiums.

Insurance companies typically review rates annually, but increases can occur more frequently. There is no universal limit, but state regulations may cap how much and how often premiums can rise.