Medicare covers a large share of healthcare costs, but it does not cover everything. You may still be responsible for deductibles, co-payments, and coinsurance costs, which can be significant. This is where extra insurance can help. Medicare Supplement Insurance, also known as Medigap, is extra insurance you can buy from a private company to help pay your share of out-of-pocket costs in Original Medicare. Medigap policies fill in the gaps in Medicare coverage, and some even offer coverage when travelling outside the US. However, they generally do not cover long-term care, vision, dental, hearing aids, private nursing, or prescription drugs. Therefore, it is important to consider your specific needs when deciding whether to purchase supplemental insurance to go along with Medicare.

| Characteristics | Values |

|---|---|

| What is it? | Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps pay your share of out-of-pocket costs in Original Medicare. |

| Who is it for? | Anyone who has Medicare Part A and Part B is eligible to apply for a Medicare supplement plan. |

| What does it cover? | Medigap covers deductibles, coinsurance, and other out-of-pocket costs from Medicare. Some policies also offer coverage for travel outside the US, dental, vision, and hearing services. |

| What doesn't it cover? | Medigap policies generally do not cover long-term care, prescription drugs, or hearing aids. |

| How does it work with other insurance? | If you have Medicare and other health insurance, one will be the "primary payer" and the other the "secondary payer". The primary payer pays up to its limit, then sends the remaining balance to the secondary payer. |

| How much does it cost? | Typically, you pay a monthly premium to the insurance company for a Medigap policy. |

Explore related products

What You'll Learn

![]()

Medicare doesn't cover all costs

Original Medicare (Parts A and B) doesn't cover all healthcare costs. It also doesn't cover prescription drugs. For this reason, many people opt for Medicare Supplement Insurance (Medigap) or Medicare Advantage to fill the gaps. Medigap is extra insurance you can buy from a private company that helps pay your share of costs in Original Medicare. Generally, you need Part A and Part B to buy a Medigap policy. Some Medigap policies offer coverage when you travel outside the US. However, Medigap policies don't cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

If you're a hospital inpatient, Medicare Part A generally covers your care for a limited time. A deductible or copay generally applies. For instance, you pay $0 per day for days 1-20 (but the Part A deductible applies), $204 per day for days 21-100, and you pay all costs from day 101 onwards.

Medicare Part B generally covers most outpatient care. Most Part D prescription drug plans might have an annual deductible, and you pay a copayment or coinsurance amount each time you fill a prescription. These costs vary from one plan to another.

If you receive Medicare by way of disability, it is recommended that you speak with an independent advisor who can help compare your options to cover what Medicare doesn’t cover. For instance, if you are not yet 65, you might benefit from choosing Medicare Advantage because Medigap can be much more expensive.

Understanding Master Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Supplemental insurance helps cover out-of-pocket expenses

Medicare is a federal program that provides health insurance coverage for people aged 65 and over, as well as some younger people with disabilities or end-stage renal disease. While Medicare can be a valuable source of health coverage, it doesn't cover all medical expenses. This is where supplemental insurance comes in.

Supplemental insurance, also known as Medicare Supplement Insurance or Medigap, is additional insurance that you can purchase to help cover the gaps left by Medicare. It is designed to help pay for expenses that your original Medicare plan may not cover, such as deductibles, copayments, and coinsurance. These out-of-pocket costs can add up quickly, especially if you require frequent medical care or face unexpected health challenges.

Medigap policies are sold by private insurance companies and are standardized, meaning that the benefits offered are the same across different insurers. However, it's important to note that Medigap doesn't cover costs for services that Original Medicare doesn't cover, such as long-term care or dental services. Additionally, Medigap policies generally don't cover prescription drugs, vision, or hearing aids.

Supplemental insurance can provide peace of mind and financial protection by helping to cover these out-of-pocket expenses. It ensures that individuals are not burdened with unexpected or excessive medical costs. When considering supplemental insurance, it's important to carefully review the limitations and benefits of different policies, as they may vary. Additionally, understanding the coordination of benefits between Medicare and any other insurance coverage you have is crucial to ensure proper coverage and payment.

In summary, supplemental insurance plays a crucial role in helping individuals with Medicare cover their out-of-pocket expenses. By purchasing a Medigap policy, individuals can have added protection against the financial burden of unexpected or high medical costs, ensuring that they can focus on their health and well-being without worrying about excessive out-of-pocket expenses.

Ophthalmology Insurance: What You Need to Know

You may want to see also

Explore related products

$8

![]()

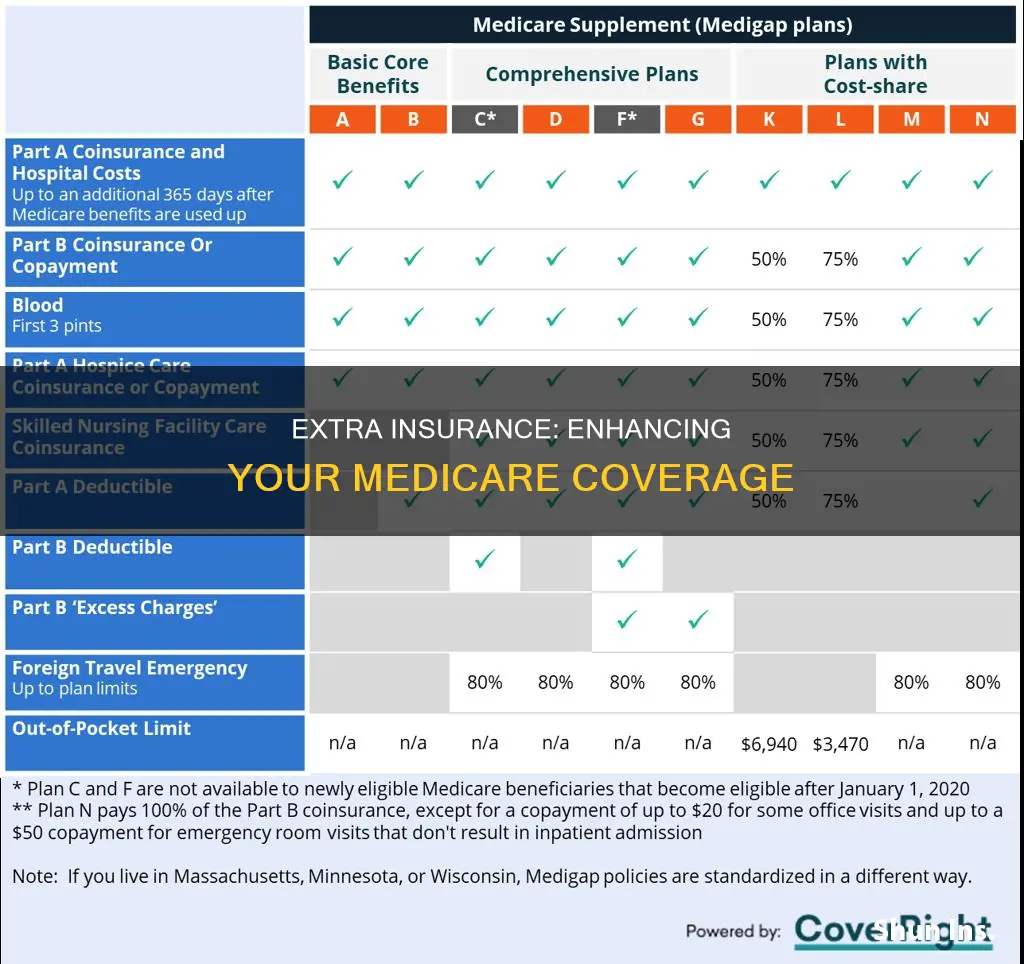

Medigap policies fill Medicare coverage gaps

Medicare is the federal health insurance program for people aged 65 and over, but it doesn't cover all health-related costs. This is where extra insurance, or Medigap, comes in. Medigap policies, or Medicare Supplement Insurance, are sold by private companies and help pay for some of the costs that aren't covered by Original Medicare (Part A and Part B). This includes costs like copayments, coinsurance, and deductibles. Generally, you need to have Original Medicare (both Part A and Part B) before you can buy a Medigap policy.

Medigap policies can also cover services that Original Medicare doesn't, like emergency medical care when travelling outside the US. Some policies might even offer coverage for prescription drugs, but this is becoming less common. Medigap plans sold after 2005 don't include prescription drug coverage, so you would need to join a separate Medicare drug plan (Part D) for this.

It's important to note that Medigap policies are different from Medicare Advantage Plans (Part C). While Medigap supplements Original Medicare, a Medicare Advantage Plan is an alternative way to receive Medicare coverage. You can't have both at the same time. If you want to switch between them, you usually have a 12-month trial period to make the change without losing your coverage.

Medigap policies only cover one person, so spouses would each need their own policy. Additionally, Medigap doesn't cover everything. For example, it generally doesn't cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Despite these exclusions, Medigap policies can provide valuable peace of mind by filling in some of the gaps in Original Medicare coverage.

Using Medical Insurance for Dental Work: What You Need to Know

You may want to see also

Explore related products

![]()

Medicare Advantage offers more flexibility

Medicare Advantage, also known as MA, is a popular alternative to Original Medicare. It offers flexibility in terms of cost and coverage, often including prescription drugs and vision, hearing, or dental care.

Original Medicare beneficiaries often purchase a Medicare Supplement Insurance plan, or Medigap, to help pay for expenses such as the 20% coinsurance not covered by Medicare. Medigap also provides foreign emergency coverage. However, Medigap does not include dental, vision, or hearing coverage. Medicare Advantage, on the other hand, typically covers these services for a lower premium.

Medigap plans offer more flexible coverage than Medicare Advantage, but they charge higher premiums. Additionally, Medigap policies generally do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Medicare Advantage plans are designed to cover everything that Original Medicare does, and more.

Medicare Advantage may be a more affordable option, with built-in price breaks on annual costs. However, it may involve more hassles with preauthorization and provider network requirements. Medicare Advantage plans can change benefits annually or drop providers mid-year, and there may be geographical restrictions on accessing care outside of your state.

In conclusion, Medicare Advantage offers more flexibility in terms of cost and coverage for services such as dental, vision, and hearing. However, it is important to consider the potential downsides, including limited provider choices, unexpected plan changes, and restrictions on care access.

Understanding PPO Insurance and Medical Expense Deductions

You may want to see also

Explore related products

![]()

Supplemental insurance aids in retirement healthcare costs

While Medicare covers a large share of healthcare costs, it does not cover everything. There are out-of-pocket expenses that individuals must pay, such as deductibles, co-payments, and coinsurance costs. This is where supplemental insurance can help.

Supplemental insurance, also known as Medigap insurance, is extra insurance that can be purchased from private companies to help cover these out-of-pocket costs. It is important to note that Medigap policies do not cover long-term care, prescription drugs, vision, dental, or hearing aids. However, some Medigap policies offer coverage for healthcare expenses incurred while travelling outside the US.

To be eligible for a Medigap policy, individuals must have Original Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). During the Medigap open enrollment period, which lasts six months from the time an individual turns 65 and signs up for Medicare Part B, insurance companies must accept the applicant regardless of any pre-existing health conditions. After this period, insurance companies may ask about health conditions and could increase premiums or deny coverage.

Medicare Advantage is another option that bundles Part A, Part B, and sometimes Part D (drug coverage) into one plan. These plans offer more flexibility than Medigap and may include benefits such as dental, vision, and prescription drugs. However, the benefits and costs of Medicare Advantage plans can change annually during the enrollment period, and the co-payments and deductibles may be higher compared to Medigap.

When considering supplemental insurance, it is advisable to speak with a financial representative to determine the best options for managing healthcare costs during retirement.

Battling Insurance: Strategies to Secure Your Medication Coverage

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help cover out-of-pocket costs in Original Medicare.

While Medicare covers a large share of healthcare costs, it does not cover everything. Extra insurance helps cover out-of-pocket expenses such as deductibles, co-payments, and coinsurance costs.

Medigap policies fill in the gaps in Medicare coverage. They typically cover deductibles, coinsurance, and other out-of-pocket costs according to the policy terms. Some Medigap policies also offer coverage for foreign travel emergencies.