Medicare typically covers hospice care under Medicare Part A, but patients may be responsible for any Medicare-approved copayments or coinsurance associated with hospice. This is where Medicare Supplement insurance comes in. Medicare Supplement insurance plans are offered by private insurance companies and may help cover out-of-pocket costs not paid under Original Medicare Part A (hospital insurance) and Part B (medical insurance). These plans fill the gaps in Original Medicare coverage, such as deductibles, co-insurance, and copayments.

| Characteristics | Values |

|---|---|

| Qualifying conditions for hospice care | You must have Medicare Part A (Hospital Insurance) and be certified as terminally ill by your hospice doctor and regular doctor, with a life expectancy of 6 months or less. You must accept palliative care instead of treatment to cure your illness and sign a statement choosing hospice care. |

| Hospice care coverage | Medicare Part A typically covers hospice care. Medicare Advantage plans can also expand coverage beyond Original Medicare. Hospice care includes inpatient and outpatient care, medication, and respite care for caregivers. |

| Out-of-pocket expenses | Medicare Supplement insurance (Medigap) can help cover out-of-pocket expenses not covered by Original Medicare, such as deductibles, copayments, and coinsurance. The 10 standardized Medicare Supplement plans offer varying levels of coverage for these expenses. |

| Opting out of hospice care | You have the right to stop receiving hospice care at any time and can return to the Medicare coverage you had before, such as a Medicare Supplement insurance plan and Original Medicare Part A and Part B. |

Explore related products

What You'll Learn

- Medicare Part A covers hospice care

- Medicare Supplement Insurance plans cover copayments and coinsurance

- Hospice care is for terminally ill patients with a prognosis of 6 months or less

- Hospice care can be provided at home or in a facility

- Medicare Advantage plans offer additional benefits beyond Original Medicare

![]()

Medicare Part A covers hospice care

Medicare-approved hospice care can be provided in your home or another facility, such as a nursing home, and you pay nothing for this care. However, you may have to pay for room and board if you choose to receive hospice care in a facility. Medicare Part A covers the cost of prescription drugs for pain relief and symptom management, with a copayment of up to $5 per prescription. If you require inpatient respite care, you may pay up to 5% of the Medicare-approved amount, but your copay cannot exceed the inpatient hospital deductible for the year.

While Medicare Part A covers most hospice care costs, there may be some gaps in coverage. For example, you may be responsible for Medicare-approved copayments or coinsurance associated with hospice care. This is where Medicare Supplement Insurance, also known as Medigap, comes in. Medicare Supplement plans are offered by private insurance companies and help cover out-of-pocket costs not paid under Original Medicare Part A and Part B. These plans fill the "gaps" in Original Medicare coverage, such as deductibles, coinsurance, and copayments.

It is important to note that if you decide to leave hospice care, your original Medicare coverage or Medicare Supplement plan will typically resume. Additionally, if your health improves or your illness goes into remission, you may be discharged from hospice care and return to your previous Medicare coverage.

Pet Owner's Guide to Medical Insurance Expenses

You may want to see also

Explore related products

![]()

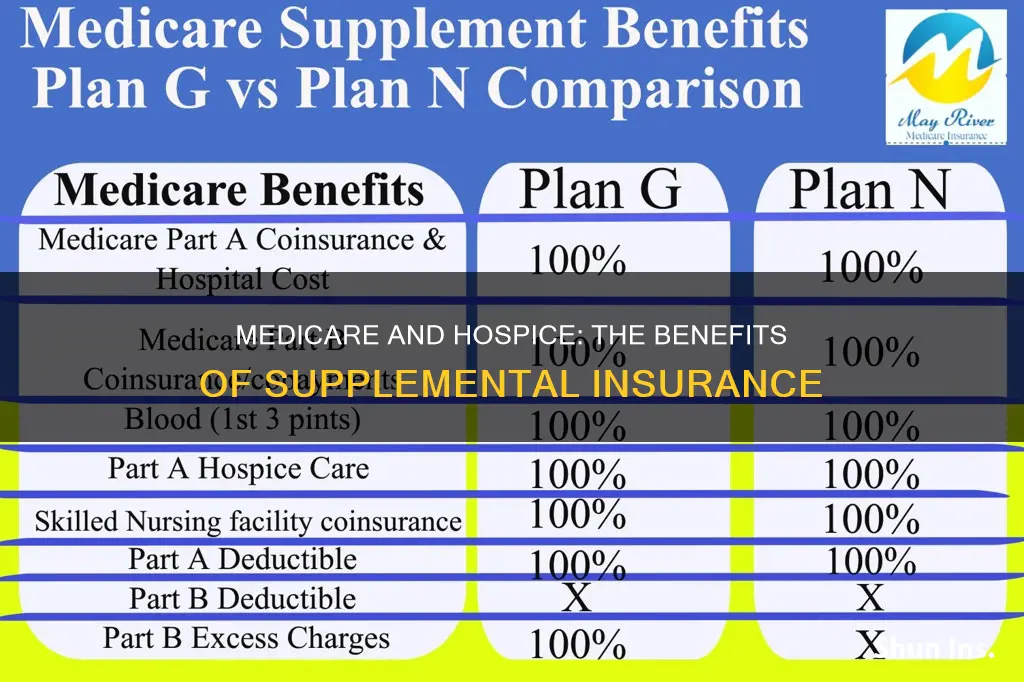

Medicare Supplement Insurance plans cover copayments and coinsurance

Medicare Supplement Insurance plans, also known as Medigap, help fill the "gaps" in Original Medicare. These “gaps” refer to expenses incurred under Original Medicare, such as deductibles, co-insurance, and copayments.

Medicare Supplement Insurance plans are offered by private insurance companies and help cover most out-of-pocket costs not paid under Original Medicare Part A (hospital insurance) and Part B (medical insurance). This includes copayments and coinsurance associated with hospice care, such as prescription drugs for pain relief and respite care for caregivers.

It's important to note that Medicare typically covers hospice care under Medicare Part A. However, individuals may still be responsible for any Medicare-approved copayments or coinsurance. Medicare Supplement Insurance plans can help cover these costs. For example, Plan K covers 50%, and Plan L covers 75% of the Medicare copayment or coinsurance amount.

Additionally, Medicare Supplement Insurance plans provide flexibility, allowing individuals to see any doctor or hospital in the US that accepts Medicare patients. These plans are standardized by the federal government, and each is named with a letter, like Plans A, F, G, and N. The best plan for an individual depends on their specific needs and budget. For instance, Plan F has the broadest coverage of Original Medicare out-of-pocket costs, including deductibles and some copayments and coinsurance. However, it is only available to those who were eligible for Medicare before January 1, 2020. On the other hand, Plan G is popular and offers broad coverage for most people, except for the Medicare Part B deductible. Plan N offers a lower premium with some copays and a small annual deductible.

In summary, Medicare Supplement Insurance plans help cover copayments and coinsurance associated with hospice care, providing financial peace of mind and flexibility in choosing healthcare providers.

Medical Insurance Coverage for Transfer Benches: What's Included?

You may want to see also

Explore related products

![]()

Hospice care is for terminally ill patients with a prognosis of 6 months or less

Hospice care is a type of end-of-life care for terminally ill patients with a prognosis of six months or less. It focuses on providing comfort, symptom management, and emotional support to patients and their families during their final months. To qualify for hospice care, a patient must meet specific eligibility requirements, including certification by their hospice doctor and regular doctor that their illness is incurable and their life expectancy is six months or fewer. This certification is typically based on a combination of factors, including the patient's functional status, nutritional status, and overall clinical deterioration.

Medicare typically covers hospice care under Medicare Part A. However, patients may still be responsible for certain out-of-pocket expenses, such as copayments for prescription drugs and respite care for caregivers. To help cover these additional costs, patients can consider purchasing Medicare Supplement Insurance (also known as Medigap), which is offered by private insurance companies. These supplemental plans fill the "gaps" in original Medicare coverage, including deductibles, coinsurance, and copayments.

It is important to note that hospice care is not just for patients with cancer or other specific illnesses. Patients with various conditions, such as heart failure, cardiopulmonary disease, liver disease, or neurological diseases, may also qualify for hospice care if they meet the eligibility criteria. The hospice team, in collaboration with the patient's attending physician, determines the primary diagnosis contributing to the patient's terminality.

Once a patient chooses hospice care, their hospice benefit should cover everything they need for their end-of-life care. Medicare-approved hospice providers ensure that patients pay nothing for hospice care. However, patients may still be responsible for room and board if they receive hospice care in their homes, nursing homes, or inpatient facilities. Additionally, patients have the right to change their hospice provider once during each benefit period, allowing them to find the care that best suits their needs.

In summary, hospice care is specifically designed for terminally ill patients with a prognosis of six months or less. It provides comprehensive support and comfort during the patient's end-of-life journey. Medicare typically covers hospice care, but supplemental insurance can help with any additional out-of-pocket expenses. By understanding the eligibility criteria and seeking the appropriate care team, patients and their families can make informed decisions about their end-of-life care options.

Medicaid and Copays: Does PA Cover Primary Insurance Copays?

You may want to see also

Explore related products

![]()

Hospice care can be provided at home or in a facility

Hospice care is a form of medical care for patients with terminal illnesses who are expected to live six months or less. It focuses on enhancing comfort and overall quality of life rather than increasing its quantity. Hospice care can be provided at home or in a facility, and patients can choose the option that best suits their needs and preferences.

Home hospice care allows patients to remain in their familiar surroundings, surrounded by loved ones. It offers personalized treatment plans, including visits from doctors, nurses, and hospice aides, medication management, and emotional support. However, it may require home modifications or additional support services, and family members may need to be involved in caregiving.

On the other hand, hospice facilities provide professional care and support in a structured setting. They offer a wide range of services, including access to advanced medical equipment and specialized therapies that may not be available at home. Families may find it more convenient as the facility staff handles most arrangements.

The decision between home hospice and hospice facility depends on various factors, including the patient's needs, preferences, health condition, and support network. Both options offer valuable support and aim to ensure comfort and dignity during end-of-life care.

Regarding supplemental insurance with Medicare and hospice, Medicare Part A typically covers hospice care. However, patients may be responsible for Medicare-approved copayments or coinsurance associated with hospice services, such as prescription drugs and respite care for caregivers. Medicare Supplement insurance plans, also known as Medigap plans, offered by private insurance companies, can help cover these out-of-pocket costs. These plans fill the "gaps" in Original Medicare coverage, including deductibles, coinsurance, and copayments.

How Medicare and Medicaid Changes Affect Private Insurance

You may want to see also

Explore related products

![]()

Medicare Advantage plans offer additional benefits beyond Original Medicare

Medicare Advantage plans, also known as Part C, are offered by Medicare-approved private companies. These plans provide an alternative way to receive Part A (Hospital Insurance) and Part B (Medical Insurance) benefits, as opposed to Original Medicare. They often include Part D (drug coverage) and offer additional benefits beyond Original Medicare.

Medicare Advantage plans typically include a range of plan types, such as Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and Special Needs Plans (SNPs). These plans offer flexibility and tailored options to suit individual needs.

One of the key advantages of Medicare Advantage plans is their ability to fill the "'gaps'" in Original Medicare coverage. Original Medicare may leave beneficiaries with out-of-pocket costs, such as deductibles, co-insurance, and copayments. Medicare Advantage plans can help cover these expenses, providing financial relief to individuals.

Additionally, Medicare Advantage plans offer a diverse range of benefits that cater to specific needs. For example, Medicare Advantage plans may provide access to Medicare Medical Savings Accounts (MSAs) or Private Fee-for-Service Plans (PFFS). These options allow beneficiaries to customize their coverage according to their unique healthcare requirements and preferences.

It is important to note that before enrolling in a Medicare Advantage plan, individuals should consult their employer, union, or benefits administrator to understand the implications for any existing coverage. Joining a Medicare Advantage Plan might result in the loss of employer or union coverage, affecting not just the individual but also their spouse and dependents.

Strategies to Negotiate Medical Bills Like Your Insurance Company

You may want to see also

Frequently asked questions

Hospice care is end-of-life care for terminally ill patients who have a life expectancy of six months or less. It provides comfort and support to patients and their families during this difficult time.

Medicare typically covers hospice care under Medicare Part A (Hospital Insurance). However, there may be some out-of-pocket expenses, such as copayments for prescription drugs and respite care for caregivers.

Supplemental insurance, also known as Medigap insurance, can help cover the out-of-pocket costs associated with hospice care that Original Medicare doesn't cover. These expenses may include deductibles, copayments, and coinsurance.

The 10 standardized Medicare Supplement plans available in most states offer coverage for respite care coinsurance and copayments for prescription drugs related to hospice care.