Insurance companies often inquire about your monthly food budget as part of their broader assessment of your financial habits and lifestyle. This information helps them gauge your overall financial stability, spending patterns, and potential risks. For instance, a high food budget might indicate frequent dining out, which could correlate with health risks like obesity or cardiovascular issues, potentially affecting life or health insurance premiums. Conversely, a low budget might suggest cost-cutting measures that could impact overall well-being. By understanding your food spending, insurers can more accurately underwrite policies, tailor coverage, and assess long-term risks, ensuring fair pricing while managing their own exposure to claims.

| Characteristics | Values |

|---|---|

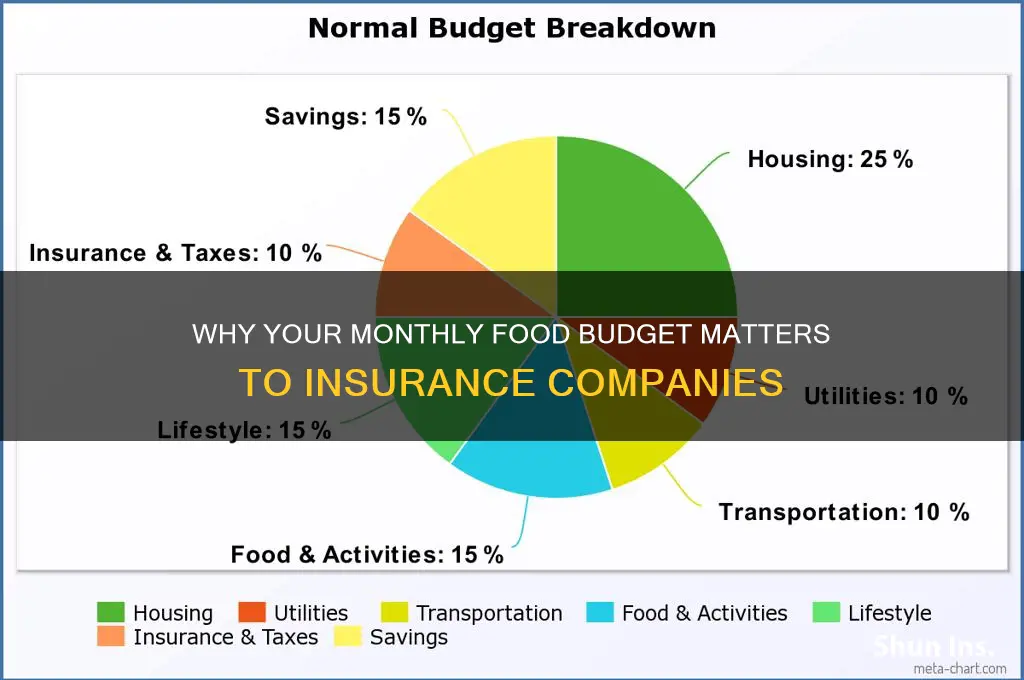

| Risk Assessment | Insurance companies use your monthly food budget as a proxy for your overall lifestyle and financial habits. A higher food budget might indicate a more affluent lifestyle, potentially correlating with higher-risk behaviors or more valuable assets to insure. |

| Health Indicators | Food choices reflect dietary habits, which can impact health. Unhealthy eating patterns may lead to higher health risks, influencing life and health insurance premiums. |

| Financial Stability | A consistent and reasonable food budget suggests financial discipline and stability, which insurers view favorably as it indicates lower likelihood of missed payments. |

| Inflation and Cost of Living | Food costs are a significant part of household expenses. Insurers may use this data to adjust premiums based on regional cost of living and inflation trends. |

| Lifestyle Insights | Food spending can reveal lifestyle choices (e.g., dining out vs. cooking at home), which insurers use to assess risk profiles for various insurance products. |

| Fraud Detection | Inconsistencies between reported income, food budget, and other financial data may raise red flags for potential fraud or misrepresentation. |

| Personalized Pricing | Some insurers use detailed financial data, including food budgets, to offer personalized premiums based on individual risk and lifestyle factors. |

| Behavioral Analytics | Advanced insurers use food budget data in behavioral analytics models to predict claims likelihood and customer behavior. |

| Regulatory Compliance | In some regions, insurers must justify premium calculations, and including food budget data helps demonstrate a comprehensive risk assessment process. |

| Customer Segmentation | Food budget data helps insurers segment customers into groups with similar risk profiles for targeted marketing and product offerings. |

Explore related products

What You'll Learn

- Assessing Lifestyle Risks: Links food spending to health habits, predicting potential medical claims

- Income Verification: Confirms financial stability and ability to pay premiums consistently

- Behavioral Insights: Analyzes spending patterns to gauge responsibility and risk-taking tendencies

- Health Underwriting: High food costs may indicate poor diet, increasing health-related claim risks

- Fraud Detection: Unusual food budgets can flag discrepancies in reported income or lifestyle

![]()

Assessing Lifestyle Risks: Links food spending to health habits, predicting potential medical claims

Insurance companies often inquire about your monthly food budget because it serves as a proxy for understanding your dietary habits, which are closely tied to overall health. For instance, a high budget might indicate frequent dining out, potentially linked to higher consumption of processed foods and lower intake of nutrients. Conversely, a modest budget could suggest home cooking, often associated with healthier eating patterns. This data point allows insurers to assess lifestyle risks and predict future medical claims by identifying patterns that correlate with chronic conditions like diabetes, heart disease, or obesity.

Consider the analytical perspective: Studies show that individuals spending over 50% of their food budget on eating out are 30% more likely to develop metabolic syndrome compared to those who cook at home. Insurers use this correlation to stratify risk, adjusting premiums accordingly. For example, a 40-year-old with a $600 monthly food budget, primarily spent on fast food, may face higher premiums than a peer with a $400 budget focused on groceries for meal prep. This isn’t about judgment—it’s about actuarial science leveraging behavioral data to forecast healthcare costs.

From an instructive standpoint, understanding this link empowers individuals to make informed choices. Reducing restaurant spending by 20% and redirecting funds to whole foods can lower the risk of hypertension by up to 15%, according to a Harvard study. Practical tips include meal planning, bulk buying, and prioritizing nutrient-dense foods like leafy greens, lean proteins, and whole grains. Insurers may even offer wellness programs incentivizing such habits, proving that small dietary shifts can yield significant health and financial dividends.

Comparatively, this approach mirrors how auto insurers use mileage data to assess driving risk. Just as more miles on the road increase accident likelihood, a diet heavy in processed foods elevates health risks. However, unlike driving, dietary habits are more malleable. Insurers increasingly offer tools like nutrition tracking apps or discounts on gym memberships, turning policyholders from passive risk subjects into active health managers. This shift not only reduces claims but also fosters a preventive care mindset.

Finally, the descriptive lens reveals a broader trend: insurance is evolving from reactive to predictive. By linking food spending to health outcomes, companies move beyond traditional metrics like age or family history. For instance, a 35-year-old with a $300 grocery-focused budget might be rated lower risk than a 30-year-old spending $800 on takeout, despite the age difference. This granular approach reflects a healthcare system prioritizing prevention, where lifestyle data isn’t just a number—it’s a roadmap to better health and lower costs.

Canceling SSI Medical Insurance Cover: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Income Verification: Confirms financial stability and ability to pay premiums consistently

Insurance companies often request details about your monthly food budget as part of a broader income verification process. This seemingly unrelated question serves a critical purpose: it provides a snapshot of your discretionary spending habits, which are directly tied to your overall financial stability. By understanding how much you allocate to essentials like food, insurers can gauge your ability to manage expenses and, by extension, your likelihood of consistently paying premiums. For instance, a high food budget relative to income might indicate financial strain, while a balanced allocation suggests disciplined budgeting.

Analyzing your food budget allows insurers to assess your financial health in a practical, everyday context. It’s not just about the number itself but how it fits into your broader financial picture. For example, if your food budget consumes a significant portion of your income, it may signal limited flexibility to cover unexpected costs, including insurance premiums. Conversely, a modest food budget paired with stable income indicates a higher capacity to meet financial obligations. This analysis helps insurers categorize risk and tailor policies accordingly, ensuring premiums are affordable for both parties.

To illustrate, consider a 35-year-old earning $50,000 annually. If their monthly food budget is $800, it represents 16% of their post-tax income—a reasonable figure. However, if their food budget is $1,500, it raises red flags, as it suggests disproportionate spending on non-essential items or financial mismanagement. Insurers use such data to predict payment reliability, often adjusting premiums or requiring additional verification for higher-risk profiles. Practical tip: Review your budget before applying for insurance to ensure discretionary spending aligns with industry benchmarks.

From a persuasive standpoint, transparency in income verification benefits both you and the insurer. By accurately reporting your food budget, you demonstrate financial responsibility, potentially qualifying for lower premiums or better coverage terms. Insurers rely on this data to mitigate risk, ensuring they can fulfill claims without overcharging responsible policyholders. For example, a family of four with a $600 monthly food budget on a $70,000 income is likely to be viewed as low-risk, whereas a single individual with the same budget on a $30,000 income may face scrutiny. Honesty in reporting fosters trust and aligns incentives.

In conclusion, your monthly food budget is more than a trivial detail—it’s a window into your financial discipline and stability. Insurers use this information to verify income, assess risk, and ensure premiums are paid consistently. By understanding this process, you can proactively manage your budget, provide accurate information, and secure favorable insurance terms. Remember, it’s not about restricting your spending but demonstrating a balanced approach to financial management.

Top Insurance Companies Offering the Best Value for Your Money

You may want to see also

Explore related products

![]()

Behavioral Insights: Analyzes spending patterns to gauge responsibility and risk-taking tendencies

Insurance companies often inquire about your monthly food budget, not merely to satisfy curiosity, but to glean valuable behavioral insights. This seemingly mundane detail serves as a microcosm of your broader financial habits, offering a window into your spending patterns, self-discipline, and propensity for risk. By analyzing how you allocate funds for essentials like food, insurers can infer your overall financial responsibility and, consequently, your potential risk as a policyholder.

Consider the analytical perspective: a person who consistently allocates a reasonable, stable amount for groceries each month demonstrates predictability and planning. This suggests a lower likelihood of impulsive decisions, which could translate to safer driving habits or more prudent health choices. Conversely, erratic or excessively high food expenditures might indicate a lack of financial control, potentially correlating with higher-risk behaviors. For instance, someone who frequently dines out on expensive meals may also be more inclined to take risks in other areas of life, such as speeding or neglecting preventive healthcare.

From an instructive standpoint, understanding this connection empowers individuals to view their spending habits as more than just personal choices. A practical tip: track your monthly food expenses for three months, categorizing them into essentials (groceries), discretionary (dining out), and indulgences (premium brands or exotic items). This exercise not only helps you identify areas for financial optimization but also prepares you to present a more favorable profile to insurers. For example, reducing dining out from 50% to 30% of your food budget could signal improved financial discipline, potentially leading to better insurance rates.

Persuasively, insurers argue that such data-driven assessments ensure fairer pricing and more accurate risk evaluations. By integrating behavioral insights, they can reward responsible individuals with lower premiums while charging higher rates to those exhibiting riskier spending patterns. This approach aligns with the broader trend of personalized insurance, where factors beyond traditional demographics play a pivotal role. For instance, a 35-year-old with a modest food budget and consistent savings might qualify for lower life insurance premiums compared to a peer with similar health metrics but erratic spending habits.

Finally, a comparative analysis reveals that this practice is not unique to insurance. Financial institutions, such as banks and credit card companies, also scrutinize spending patterns to assess creditworthiness. However, insurers take it a step further by linking these patterns to lifestyle risks. For example, a high allocation for fast food or alcohol might raise red flags for health insurers, who could infer increased risks of obesity or accidents. Thus, your food budget becomes a proxy for broader lifestyle choices, influencing not just your premiums but also the terms of your coverage.

In conclusion, the seemingly innocuous question about your monthly food budget is a strategic tool for insurers to decode your behavioral tendencies. By analyzing this data, they can make informed predictions about your responsibility and risk-taking, tailoring policies to match. For consumers, this underscores the importance of mindful spending—not just for financial health, but also for securing favorable insurance terms.

Who Insures Trucking Companies? A Guide to Commercial Coverage

You may want to see also

Explore related products

![]()

Health Underwriting: High food costs may indicate poor diet, increasing health-related claim risks

Insurance companies often inquire about your monthly food budget as part of their health underwriting process, and it’s not just about curiosity. High food costs can serve as a proxy for dietary habits, which in turn influence health risks. For instance, a household spending significantly more on processed foods, takeout, or sugary beverages may be at a higher risk for obesity, diabetes, or cardiovascular diseases. These conditions not only impact an individual’s quality of life but also increase the likelihood of filing health-related claims, which insurers must account for in their risk assessments.

Consider the analytical perspective: a family of four spending $1,200 monthly on food, with a large portion allocated to fast food and convenience items, is statistically more likely to face diet-related health issues. Studies show that diets high in saturated fats, sodium, and added sugars—common in processed foods—correlate with chronic illnesses. Insurers use this data to predict potential claims, adjusting premiums accordingly. Conversely, a similar budget spent on whole foods, fresh produce, and lean proteins suggests a lower health risk, potentially leading to more favorable underwriting terms.

From an instructive standpoint, understanding this connection empowers individuals to make informed choices. For example, a 30-year-old with a $500 monthly food budget could reduce health risks by allocating 70% to groceries like vegetables, whole grains, and lean meats, and limiting 30% to occasional dining out. This balance not only supports better health but may also signal to insurers a lower risk profile. Practical tips include meal planning, cooking at home, and prioritizing nutrient-dense foods, which can lower both food costs and health risks over time.

A comparative analysis reveals that insurers in countries with higher healthcare costs, such as the U.S., are more likely to scrutinize dietary indicators like food spending. In contrast, regions with universal healthcare may focus less on individual behaviors. However, even in these systems, private insurers often use similar metrics to assess supplemental policy risks. This highlights the global relevance of dietary habits in health underwriting, regardless of the healthcare model.

Finally, the takeaway is clear: your food budget isn’t just a financial metric—it’s a health indicator. Insurers use it to gauge potential risks, but individuals can leverage this knowledge to their advantage. By aligning spending with a healthy diet, you not only improve your well-being but may also secure more affordable insurance premiums. It’s a win-win: better health and better financial terms.

Medical Insurance Administrator: Outsourcing Claims and Benefits Management

You may want to see also

Explore related products

![]()

Fraud Detection: Unusual food budgets can flag discrepancies in reported income or lifestyle

Insurance companies often scrutinize monthly food budgets as a subtle yet effective tool for fraud detection. A food budget that deviates significantly from expected norms can signal inconsistencies in an individual’s reported income or lifestyle. For instance, a low-income claimant reporting a gourmet food budget or a high-income individual claiming subsistence-level spending raises red flags. These discrepancies prompt further investigation into the accuracy of financial disclosures, helping insurers identify potential fraud in claims related to income replacement or lifestyle assessments.

Analyzing food budgets requires context-specific benchmarks. A single adult’s monthly food expenditure typically ranges between $200 and $400 in the U.S., depending on location and dietary habits. Families of four average $800 to $1,200. When an applicant’s reported budget falls outside these ranges without justification—such as dietary restrictions or geographic cost differences—it becomes a data point for deeper scrutiny. For example, a claimant reporting a $50 monthly food budget while claiming a six-figure income loss may be inflating their financial need, warranting closer examination of their entire claim.

Instructively, insurers use food budgets as part of a broader fraud detection strategy. By cross-referencing this data with other financial indicators—such as housing costs, transportation expenses, and reported income—they can identify patterns of inconsistency. For instance, a claimant with a modest food budget but extravagant housing expenses may be understating their overall lifestyle to maximize a disability or income replacement claim. This layered approach ensures that no single data point is decisive but contributes to a comprehensive risk assessment.

Persuasively, the inclusion of food budgets in fraud detection is not about policing personal spending habits but ensuring fairness and accuracy in claims processing. Fraudulent claims drive up premiums for honest policyholders, making rigorous verification essential. By flagging unusual food budgets, insurers protect the integrity of their systems while discouraging opportunistic fraud. This practice also encourages claimants to provide accurate, transparent financial information, fostering trust in the insurance process.

Comparatively, food budgets serve as a more nuanced fraud detection tool than traditional income verification methods. While pay stubs and tax returns provide direct income data, they don’t always reflect lifestyle choices or spending habits. A food budget, however, offers insight into daily living standards, acting as a proxy for overall financial behavior. For example, a claimant reporting a luxury lifestyle on social media but a minimal food budget presents a clear contradiction, highlighting the value of this seemingly minor data point in uncovering fraud.

The Ultimate Guide to Traders Insurance Application

You may want to see also

Frequently asked questions

Insurance companies may ask for your monthly food budget to assess your overall financial health and lifestyle, which can help them evaluate risk and tailor policies to your needs.

Your food budget itself typically doesn’t directly impact premiums, but it may be part of a broader financial profile used to determine your ability to manage expenses and potential risks associated with your lifestyle.

While it may seem unrelated, sharing your food budget can provide insurers with insights into your spending habits and financial stability, which could indirectly influence policy recommendations or coverage options.