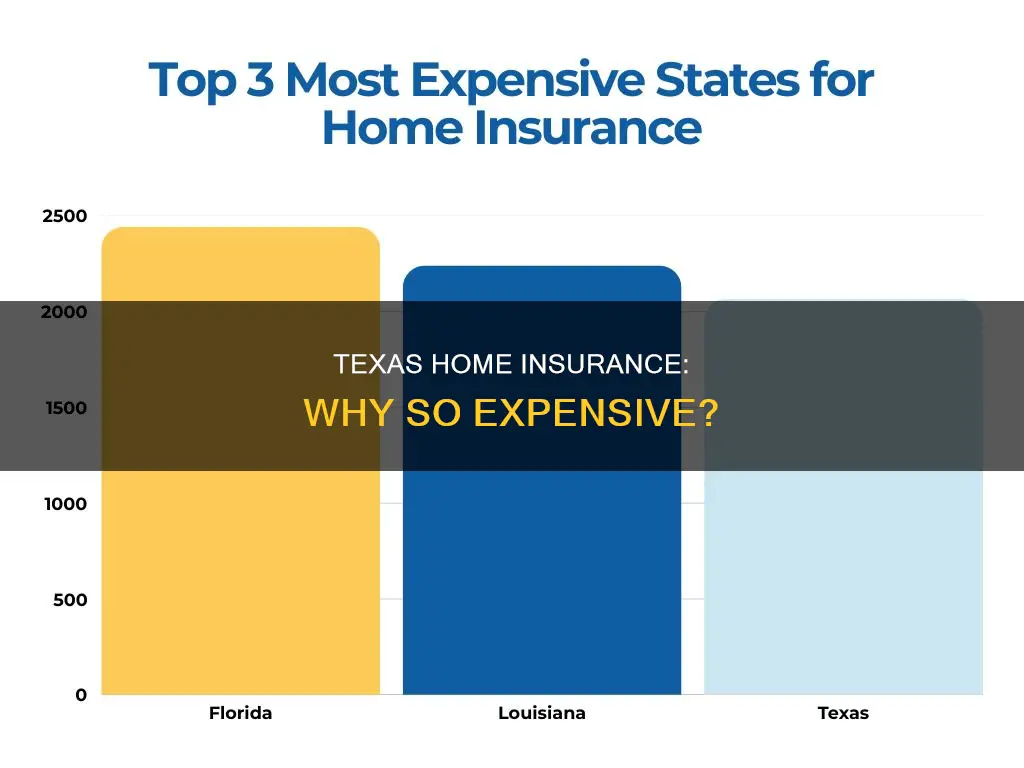

Home insurance in Texas is among the most expensive in the country, with the average annual cost of home insurance in the state being $3,875, which is 113% more than the national average. There are several factors contributing to the high cost of homeowners insurance in Texas, including the increasing number and severity of storms and other weather events, rising costs of materials and labor, and increasing home values. Texas is prone to hurricanes, wildfires, and tornadoes, which can cause extensive damage to homes and result in costly insurance claims. Climate change and inflation are also contributing to the rising cost of home insurance in the state.

| Characteristics | Values |

|---|---|

| Average annual cost of home insurance in Texas | $3,875 |

| Average annual national cost of home insurance | $1,820 |

| Percentage increase in Texas insurance rates since 2018 | 50.9% |

| Average increase in Texas insurance rates in 2023 | 21% |

| Number of damaging weather events in 2023 | 28 |

| Average cost of home insurance in Houston, Texas | $6,008 |

| Average cost of home insurance in El Paso, Texas | $2,144 |

| Average cost of home insurance in Texas | $3,851 |

| Average national cost of home insurance | $2,466 |

| Primary reason for inflating insurance prices | Increasing number of claims |

| Reason for increasing number of claims | Climate change, severe weather events, and inflation |

Explore related products

What You'll Learn

![]()

Climate change and inflation

Texas is prone to hurricanes, flooding, and wildfires, which are becoming more severe due to climate change. As a result, insurance companies are becoming increasingly concerned about the impact of powerful thunderstorms, which are wrecking homes with flooding, hail, and strong winds. The frequency and size of these weather events have led to an increase in insurance claims and payouts, with 28 weather events recorded in 2023, each causing at least $1 billion in damages. This has caused insurance companies to increase their rates to offset the costs.

Additionally, inflation has contributed to the rising cost of homeowners insurance in Texas. Inflation has pushed up construction costs, increasing the cost of building materials and construction labor. It has also led to higher reinsurance expenses, as insurance companies buy reinsurance to spread their risk and remain financially stable in the event of a major disaster. The combination of climate change and inflation has resulted in a skyrocketing increase in homeowners insurance rates in Texas, with some residents opting to go without insurance due to the high costs.

The impact of climate change on insurance rates is further exacerbated by the development of high-risk areas. As more people move to these areas, the potential for insured losses and insurance claims increases. This has led to a rise in reinsurance rates, which in turn affects the premiums charged by insurance companies. According to the Insurance Information Institute, the cumulative replacement costs for home repair increased by 55% between 2020 and 2022, outpacing the general rate of inflation.

To address the challenges posed by climate change and inflation, insurance companies are adopting more sophisticated risk modeling tools. These models help insurers better assess and price natural disaster risks, leading to more customized pricing for individual homeowners based on their risk exposure. However, this also means that high-risk homeowners may face significantly higher insurance rates.

Overall, the combination of climate change and inflation has had a significant impact on the cost of homeowners insurance in Texas, leading to rising insurance rates and challenging the affordability of homeownership in the state.

Mortgage Insurance: When Does It End?

You may want to see also

Explore related products

![]()

Severe weather events

Texas has always had high insurance rates, but the average annual cost of home insurance in 2023 was $3,875, a staggering 113% more than the national average. This surge in insurance rates can be attributed to the increasing number of claims due to severe weather events, including hurricanes, tropical storms, and hailstorms.

Texas is prone to hurricanes, which pose a consistent threat to homeowners. In addition to hurricanes, Texas has also experienced tropical storms and hailstorms, with 28 weather events recorded in 2023, each causing at least $1 billion in damages. The vulnerability to these severe weather events has made Texas one of the states with the fastest-rising home insurance rates.

The impact of severe weather events on insurance rates is evident in the Houston metropolitan area, where communities closest to the coast pay nearly three times the national average for home insurance. Houston is, in fact, the most expensive city in Texas for home insurance, with an average annual cost of $6,008. The proximity to the coast and the vulnerability to hurricanes are significant factors in the high insurance rates in this region.

In addition to coastal areas, severe weather events have also affected other parts of Texas. For example, homeowners in Amarillo and Lubbock have witnessed surging premiums due to wind storms and wildfires in the panhandle and West Texas. Central and North Texas have not been spared either, with hailstorms and tornadoes causing extensive damage and driving up insurance costs.

The frequency and intensity of storms, coupled with the rising costs of materials and labor, have put a strain on insurance providers, leading to increased premiums for homeowners. The cost of reinsurance, which insurance companies purchase to protect their losses, has also increased due to the rising number of claims. As a result, Texas homeowners are struggling to keep their homes insured, and some are even opting out of coverage altogether.

Housing Insurance: Government Control?

You may want to see also

Explore related products

![]()

Hailstorms and hurricanes

Hurricanes are another significant factor contributing to the high insurance rates in Texas. The state's proximity to the coast makes it vulnerable to hurricanes and tropical storms, which can cause widespread destruction. Houston, for example, has the highest insurance rates in Texas due to its location near the coast and its susceptibility to hurricanes. The consistent threat of hurricanes has led some insurance companies to pull out of coastal states or increase their rates.

The impact of hurricanes on insurance rates is further exacerbated by the increased frequency and intensity of these storms, which have been linked to climate change. As climate change continues to influence weather patterns, the severity and frequency of hurricanes and tropical storms are expected to increase, resulting in more costly and frequent claims. This has led to a cycle of rising insurance payouts and, subsequently, higher insurance rates for homeowners.

To mitigate the risks associated with hurricanes and hailstorms, some states have implemented incentives for homeowners to upgrade their homes to fortified standards, making them more resilient to wind and hail damage. However, the cost of repairing and rebuilding homes after these weather events remains high, contributing to the overall increase in insurance rates.

In summary, hailstorms and hurricanes have significantly contributed to the high cost of homeowners insurance in Texas. The frequency and severity of these weather events, coupled with the increasing costs of repairs and rebuilding, have led to rising insurance claims and, subsequently, higher premiums for Texas residents. As the state continues to face the challenges posed by severe weather, it is crucial for homeowners to carefully consider their insurance options and take steps to protect their properties.

Crafting a Value Report for Insurance Claims

You may want to see also

Explore related products

![]()

Increasing home values

Texas homeowners are facing a challenging situation with skyrocketing insurance costs. One of the key factors contributing to this is the increasing home values in the state. As the Texas housing market gains popularity, with four of its metro areas featured in the US News & World Report's top 10, the demand for homes has intensified. This surge in demand has led to a corresponding increase in home prices, which directly impacts the cost of insurance.

The rising home values in Texas have significant implications for insurance costs. As home prices climb, the cost of repairing or replacing a home in the event of damage also increases. This is because the cost of construction materials and labour is higher, and insurance companies need to ensure they have sufficient reserves to cover potential claims. Consequently, insurance providers are compelled to charge higher premiums to homeowners to offset these escalating expenses.

In addition to the direct impact of rising home values, the increased demand for housing in Texas has led to a higher concentration of homes in certain areas, particularly those that are vulnerable to severe weather events. This concentration of insured properties in high-risk areas further exacerbates the financial burden on insurance companies, prompting them to raise rates for homeowners in these regions.

The state's vulnerability to severe weather events, including hurricanes, tropical storms, hailstorms, and wildfires, has played a significant role in driving up insurance rates. These events have resulted in a growing number of claims, with 2023 being a record-breaking year for damaging weather-related disasters. The frequent occurrence of these events has led to substantial payouts from insurance companies, which they need to recoup through increased premiums.

To address the escalating insurance costs, some states have implemented initiatives to fortify homes against severe weather. For example, Alabama mandates that insurers offer discounts to homeowners who upgrade their homes to a fortified standard, making them more resilient to wind and hail damage. Similar discussions are taking place in Texas, with lawmakers considering ways to incentivize homeowners to reinforce their properties, thereby potentially reducing insurance rates.

While increasing home values have contributed to the surge in insurance costs, it is important to recognize that there are multiple factors at play, including the frequency and severity of weather events, inflation, and the rising cost of construction. As Texas continues to grapple with these challenges, it remains crucial for homeowners to make informed decisions regarding their insurance coverage and explore ways to mitigate the financial burden.

Strategies to Modify Your Mortgage Insurance Coverage

You may want to see also

Explore related products

$9.45 $15

![]()

Cost of reinsurance

Reinsurance is a contract between a reinsurer and an insurer, wherein the insurance company transfers some of its insured risk to the reinsurance company. Reinsurance is often referred to as "insurance for insurance companies". It allows insurers to remain solvent by recovering some or all amounts paid out to claimants.

In the context of Texas, reinsurance has been proposed as a solution to the state's high homeowners insurance costs. Texas has experienced a high number of damaging weather events, which have resulted in substantial losses for insurance companies. Reinsurance would provide these companies with substantial liquid assets to offset these losses.

A federal reinsurance program has been considered by Congress, with estimates suggesting that a national reinsurance program with an $80,000 reinsurance corridor and an 80% payment rate would cost $9.5 billion. However, it is unclear how much of this cost would be passed on to consumers in the form of higher insurance premiums.

While reinsurance can provide stability to the insurance market, it does not directly address the underlying causes of high insurance costs in Texas, such as the increasing frequency and severity of storms and the impact of inflation on construction costs. As a result, it is difficult to predict the overall effect of reinsurance on the cost of homeowners insurance in Texas.

Flood Insurance: What Mortgage Holders Need to Know

You may want to see also

Frequently asked questions

Home insurance in Texas is among the most expensive in the country due to the increasing number of claims related to severe weather events, from hurricanes and tropical storms to hailstorms and wildfires.

The average annual cost of home insurance in Texas in 2023 was $3,875, which is 113% more than the national average of $1,820.

In addition to the high number of weather-related claims, insurance rates in Texas are also impacted by rising construction and labor costs, increasing home values, and inflation.

There are a few ways to reduce the cost of homeowners insurance in Texas. One way is to make homes more disaster-resistant and upgrade them to be more resilient to severe weather. Additionally, bundling home and auto insurance can also help cut costs.