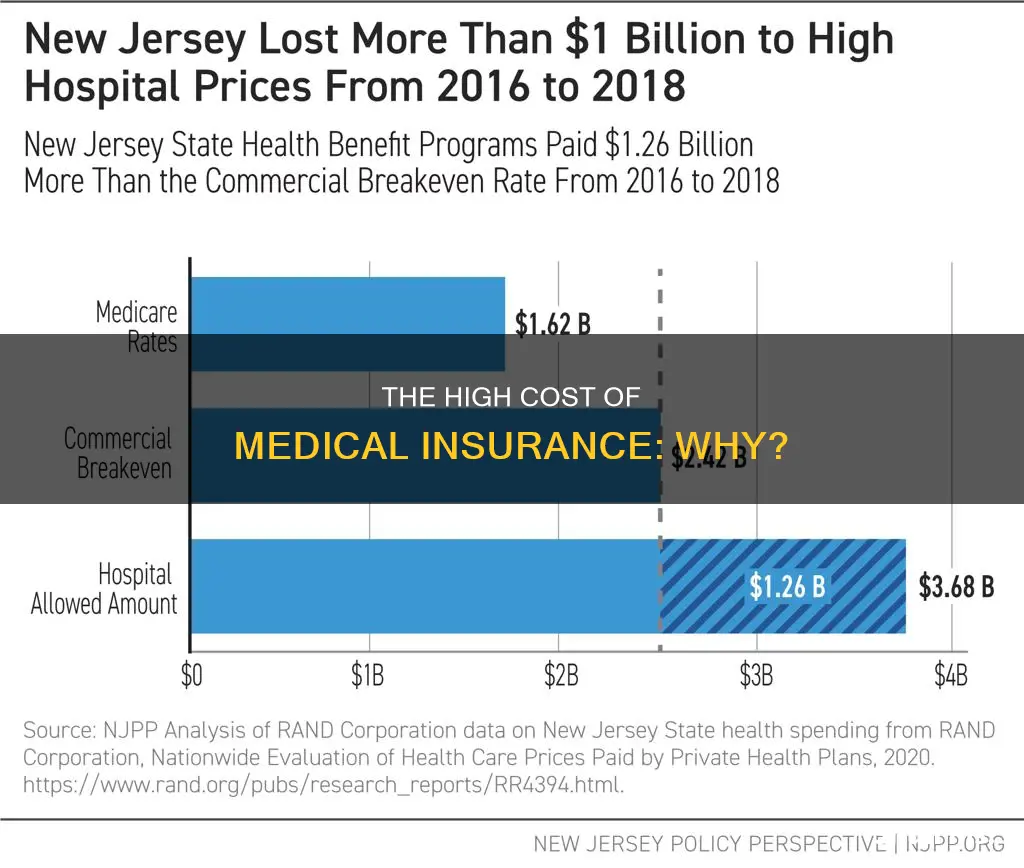

The cost of medical insurance is a complex issue influenced by a multitude of factors. In the United States, healthcare costs have been steadily increasing, with spending reaching $4.5 trillion in 2022, translating to an average of $13,493 per person. This is significantly higher compared to other wealthy nations, where the average cost per person is less than half. The reasons behind these soaring costs are varied and multifaceted, ranging from market concentration among insurance providers to the high price of pharmaceutical drugs and medical procedures.

| Characteristics | Values |

|---|---|

| Lack of government intervention | The US government does not control healthcare costs, unlike most developed countries. |

| High administrative costs | The US healthcare system's complexity leads to administrative waste and higher costs. |

| Aging population | An aging population increases healthcare utilization and prices. |

| High drug costs | Americans pay twice as much for prescription drugs compared to other developed countries. |

| Provider pricing | Hospitals, doctors, and nurses in the US charge more than in other countries. |

| Market concentration | Fewer insurance companies in the market lead to higher premiums and decreased access to affordable insurance. |

| High-tech procedures | Insurers adjust premiums to cover the costs of advanced treatments. |

| Patient behavior | Patients may insist on expensive and unnecessary procedures, contributing to wasteful spending. |

| Lack of transparency | Lack of transparency in medical service costs makes it challenging for patients to choose lower-cost options. |

Explore related products

What You'll Learn

![]()

Rising drug costs

The cost of prescription drugs is a significant concern for many Americans, with more than one in four adults reporting difficulty affording their medication. This issue has become a top health policy issue for consumers and policymakers alike. The high cost of prescription drugs can be attributed to various factors, and it is a complex issue with no single solution for reducing costs.

Firstly, drug manufacturers incur substantial research, development, marketing, and production costs in creating new medications, especially for complex health conditions. These costs are often passed on to consumers, driving up the price of prescription drugs. Additionally, pharmaceutical companies seek to maximize profits, which can result in high drug prices. While drug companies argue that developing new drugs is expensive, a study by JAMA Network Open found no correlation between research and development spending and drug prices. Furthermore, the same drugs produced by these companies often cost significantly less in Europe, where prices are negotiated.

Secondly, the lack of government intervention in the U.S. healthcare system contributes to rising drug costs. Unlike other developed countries, the U.S. government does not regulate drug prices, allowing prices to be determined by market forces. This lack of price negotiation power results in higher prices for drugs, medical equipment, and hospital care. However, there have been recent efforts to address this issue, such as the Inflation Reduction Act passed in 2022, which includes provisions to cap insulin cost-sharing for patients with Medicare.

Thirdly, the behaviour of both patients and providers can contribute to wasteful spending and higher drug costs. Patients may insist on brand-name medications or expensive procedures, believing that more expensive care is better care. Providers, on the other hand, may order unnecessary tests or procedures, further driving up costs. Additionally, insurance carriers and providers must balance the cost of new medications with their benefits to patients, which can result in difficult decisions about coverage and patient access.

Finally, the structure of the U.S. healthcare system itself contributes to rising drug costs. The majority of Americans rely on private health insurance, which can result in higher prices due to market forces. Additionally, insurance companies have shifted costs to patients through higher copays, deductibles, and premiums, further increasing out-of-pocket expenses. However, generic drugs, which are more affordable, account for approximately 90% of all prescriptions in the U.S., offering potential cost savings for patients.

Podiatry and Medical Insurance: What's Covered?

You may want to see also

Explore related products

![]()

High administrative costs

The complexity of the US healthcare system contributes to high administrative costs, which in turn drive up pricing. The US healthcare system is a mixed system, and unlike many other developed nations, it does not provide universal healthcare. The lack of political support for a universal healthcare system means the government is unable to negotiate lower costs for drugs, medical equipment, and hospital care, as is the case in other countries.

The US healthcare system's complexity also means that insurance claims are complicated, requiring many people to process them. Medical billing professionals must understand deductibles, coverage, and copays for numerous insurance companies. The training and compensation for these professionals translate into higher premiums and healthcare costs.

The US healthcare system also has separate funding sources, rules, out-of-pocket costs, and enrollment dates for various private and public insurance providers, which adds to the complexity and administrative costs. The Affordable Care Act, for example, has introduced new rules that have contributed to rising administrative costs.

The high administrative costs of the US healthcare system are a significant factor in the high cost of healthcare in the country. The system's complexity and lack of standardization lead to higher premiums and healthcare costs for consumers.

Cashing Medical Insurance Checks: What You Need to Know

You may want to see also

Explore related products

![]()

Lack of government intervention

The cost of medical insurance is high due to a variety of factors, and one of the significant reasons is the lack of government intervention in the healthcare market in the United States. Here are some key points explaining how the absence of government intervention contributes to high medical insurance costs:

Market Concentration and Competition: The US healthcare market has witnessed a trend of increasing concentration, with a decreasing number of private health insurance companies operating in each state. This concentration is often the result of mergers and acquisitions among existing insurance companies, making it challenging for new issuers to enter the market. As a result, the market becomes less competitive, leading to higher premiums and reduced access to affordable health insurance options for consumers.

Drug Pricing and Profit-Driven Healthcare: In the US, drug prices are not regulated by the government, as seen in many other countries. Pharmaceutical companies often charge significantly higher prices for drugs compared to production costs due to the expenses involved in testing and approval. Americans pay almost four times more for prescription drugs than citizens of other developed nations. The lack of government intervention in drug pricing allows companies to set high prices, impacting insurance costs. Additionally, healthcare providers in the US are often profit-driven, with hospitals, doctors, and nurses charging higher fees compared to their international counterparts.

Administrative Costs and Complexity: The complexity of the US healthcare system contributes to high administrative costs, which are ultimately passed on to consumers through insurance premiums. The system involves multiple funding sources, rules, out-of-pocket costs, and enrollment dates for various private and public insurance providers. This complexity requires a large number of medical billing professionals to process, verify, and pay out insurance claims, adding to the overall cost of healthcare and insurance.

Lack of Price Transparency: While there have been efforts to increase price transparency in the healthcare industry, the lack of transparency in medical service costs makes it challenging for companies and consumers to make informed decisions and control spending. Insurance companies and medical providers often lack transparency about the costs of services, making it difficult for consumers to choose lower-cost options or compare prices between providers.

Impact of High Healthcare Spending: The United States has one of the highest healthcare expenditures in the world, with spending reaching $4.5 trillion in 2022, averaging $13,493 per person. High healthcare spending contributes to the country's unsustainable national debt and hinders its ability to respond effectively to public health crises, such as the COVID-19 pandemic. The lack of government intervention to control healthcare costs drives up prices and has significant economic implications for the country.

Finding Doctors Who Accept Your Medico Insurance Coverage

You may want to see also

Explore related products

![]()

Fewer insurance companies

The cost of medical insurance is influenced by a multitude of factors, and one significant contributor is the decreasing number of insurance providers in the market. Over the last decade, there has been a notable decline in the number of private health insurance companies operating in each state. This trend towards market concentration results in higher premiums and reduced access to affordable health insurance options for consumers.

Market concentration occurs when three or fewer insurance companies hold at least 80% of the market share of enrollment in a given state. This phenomenon is often a result of consolidation through mergers and acquisitions among existing insurance providers. Additionally, market concentration can intensify if existing health insurance companies exit the market, further diminishing the number of available options for consumers.

The consequences of market concentration in the insurance industry are significant. As fewer insurance companies compete for consumers, the level of competition decreases. This reduced competition can lead to higher premiums and a decrease in the availability of affordable health insurance plans. Ultimately, consumers may face limited choices and higher costs for their medical insurance coverage.

The impact of market concentration is not limited to consumers alone. Healthcare providers, including doctors, hospitals, and specialized clinics, also feel the effects. Insurance companies negotiate and determine the rates they are willing to pay for different medical services. These rates may not always align with the billed amounts, leading to potential confusion for both patients and healthcare providers.

To maintain profitability, healthcare providers may need to adapt their practices. For instance, a family doctor with a high patient volume may be more amenable to lower reimbursement rates compared to a specialized surgeon who treats fewer patients with higher bills. Insurance companies also have specific criteria for covering treatments, reimbursing only those deemed "medically necessary." This dynamic can create a complex landscape for providers, who must navigate insurance requirements while ensuring they receive fair compensation for their services.

In conclusion, the decreasing number of insurance companies in the market contributes to rising medical insurance costs. This trend towards market concentration results in higher premiums, reduced access to affordable plans, and limited options for consumers. Additionally, it influences the dynamics between insurance companies and healthcare providers, potentially impacting the range of treatments and services available to patients. Addressing the issue of market concentration in the insurance industry is crucial to curbing the escalating costs of medical insurance.

Removing Adult Children from Your Medical Insurance

You may want to see also

Explore related products

![]()

High-cost procedures

The cost of medical insurance is influenced by a range of factors, including the high price of medical procedures. Technological advancements in medicine have led to the development of innovative and expensive treatments. These high-tech medical procedures contribute to increased insurance premiums as insurers adjust their rates to cover the costs associated with these cutting-edge treatments.

The use of advanced medical technology, such as MRI scans, can be significantly more expensive than simpler alternatives like X-ray imaging. Patients often believe that more expensive care equates to better care, leading to increased demand for these costly procedures. Additionally, pharmaceutical drugs play a significant role in driving up insurance costs. Americans pay almost four times more for prescription drugs compared to citizens of other developed nations. The high cost of drug development, research, marketing, and production is reflected in the price of these medications.

Furthermore, the complexity of the US healthcare system contributes to administrative waste, impacting insurance costs. The system's intricacies require a multitude of medical billing professionals, resulting in higher training and compensation costs that are ultimately passed on to consumers through increased premiums and healthcare expenses. The lack of government intervention in the US healthcare market also contributes to higher prices, as seen with the high costs of drugs due to the absence of price regulation.

The high cost of medical procedures and treatments significantly influences the overall expense of medical insurance. The intricate nature of the healthcare system, combined with the high prices of advanced technology and medications, results in increased insurance premiums for consumers. These factors collectively contribute to the rising cost of medical insurance, making it challenging for individuals to afford quality healthcare.

Invisalign Treatment: Is It Covered by Medical Insurance?

You may want to see also

Frequently asked questions

There are many factors that contribute to the high cost of medical insurance, including:

- The high cost of drugs: Americans pay almost four times as much for pharmaceutical drugs as citizens of other developed countries.

- Complexity of the system: The U.S. healthcare system is complex, and the lack of set prices for medical services means providers can charge what the market will bear.

- Market concentration: With fewer insurance companies in each state, markets become less competitive, leading to higher premiums and decreased access to affordable health insurance.

The rate companies pay for insurance is based on an employee's medical spending. Employers seek to reduce costs by excluding pricier hospitals or providers from their insurance plans' networks. Since 2000, employer premium costs have increased by about 200%, while individuals are paying 272% more for single coverage.

Individuals can take steps to manage the cost of medical insurance, such as:

- Choosing less expensive in-network healthcare providers whenever possible.

- Considering generic medication brands, which often have the same active ingredients without the high price tag.

- Shopping around for affordable health insurance plans.

- Taking a higher deductible to lower monthly premiums.